{kind=link}

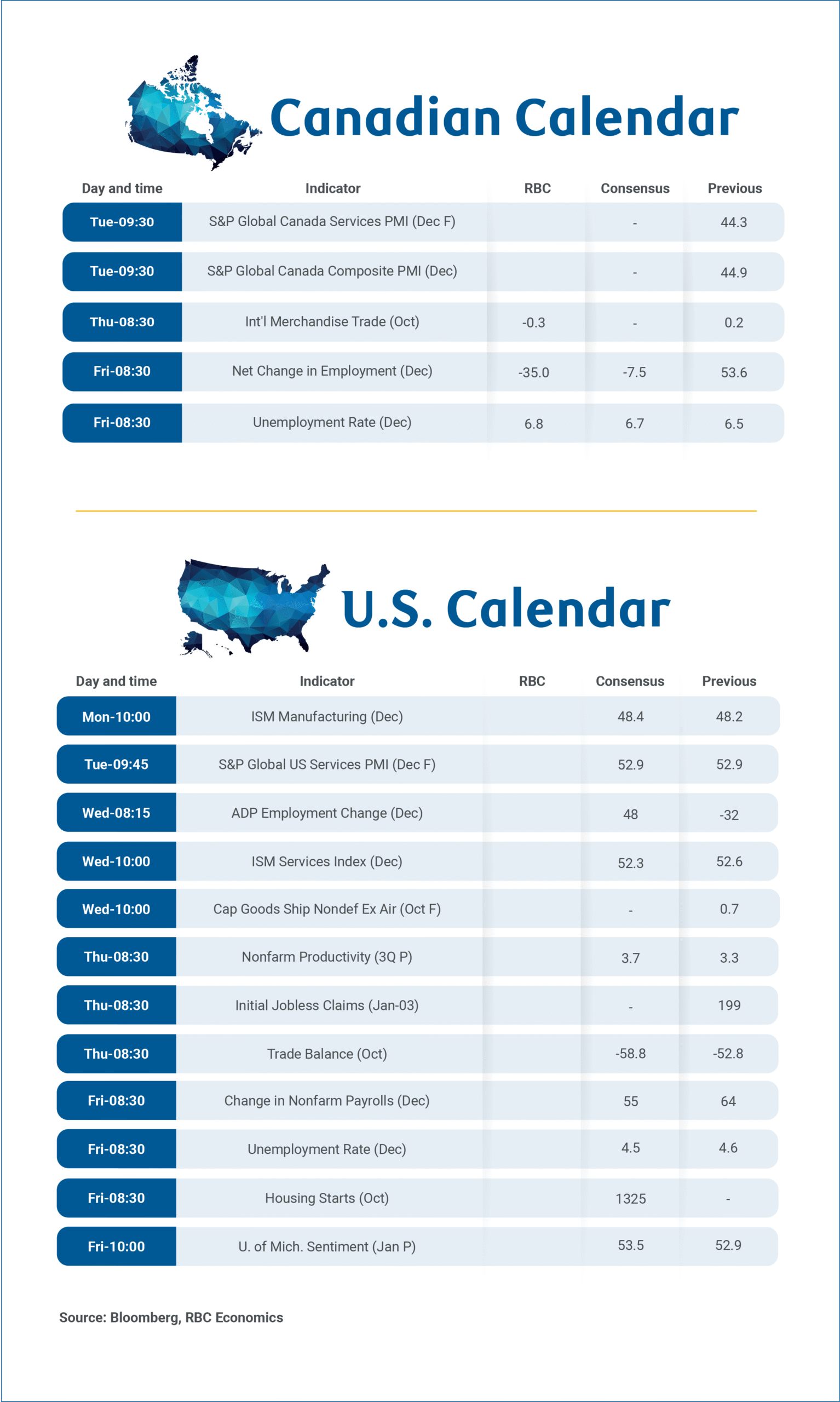

Labour market data will be back in focus next week with the dual release of Canadian and U.S. December employment reports on Friday, the first major Canadian data release of 2026 and an important input ahead of the Bank of Canada’s January policy decision.

After a series of firmer-than-expected labour market prints through the fall, we expect Canada’s December data to show a pullback after a surprisingly large drop in November unemployment, but still consistent with early signs of broader stabilization in Canadian labour markets into the end of the year.

Changes in the monthly employment count are notoriously volatile, but we look for employment to decline by 35,000 in December, reversing more than half of November’s large gain. We expect the unemployment rate to rise to 6.8% to reverse most of (but not all) of the unusually large 0.4 percentage point drop to 6.5% in November.

Although November’s sharp decline in the unemployment rate appears difficult to sustain, the December increase we expect should be viewed as a partial reversal of that move rather than a signal of renewed labour market deterioration.

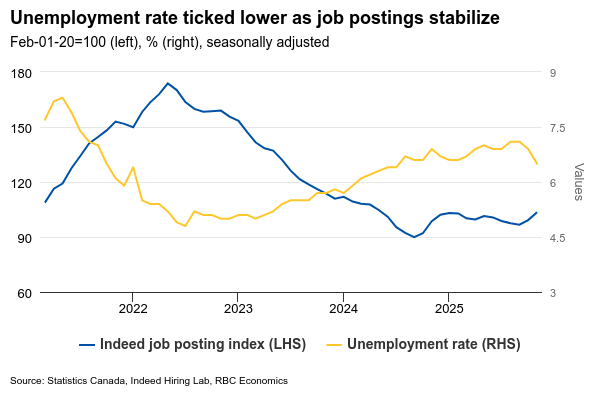

Details behind the upside surprise in the November employment data underscored the volatility in the monthly data, and may have reflected in part difficulties seasonally adjusting the data around the start of the holiday hiring period. Employment gains were again concentrated in part-time positions and among younger workers, while labour force participation declined. But the typically more stable core-age unemployment rate also declined and wage growth accelerated.

Heavily trade-exposed sectors continue to underperform broader employment trends. But there is little evidence that weakness has spread more broadly across the economy. And broader labour market conditions have shown further signs of stabilization.

Job postings data suggest hiring demand has stopped weakening and may be recovering modestly. And growth in the available labour force will continue to slow as federal government caps on temporary residence visas reduce population growth. The population aged 15+ already posted its smallest increase since May 2021 in November and highly likely slowed further in December given a reported pullback in total population in Q3.

From a policy perspective, December’s labour market report is unlikely to materially alter the Bank of Canada’s near-term outlook. We continue to expect the next change in interest rates from the BoC will be a hike, but not (as a base-case) until 2027.

Week ahead data watch:

Statistics Canada has flagged January 8th as the release date for October trade report, though timing remains preliminary given residual impacts from the earlier U.S. government shutdown. We expect October trade balance to move back to deficit, shifting from a $153 million surplus to roughly $283 million deficit, as export growth declines slightly while import growth edged higher. Lower oil prices, down 5.4% in October, likely pushed energy trade balance down. Motor vehicle shipments also reversed (-2%), following the jump in September.

In the U.S., employment growth is expected to remain slightly positive in December after a 64k gain in November. Employment growth has slowed to a crawl since tariffs escalated sharply with an average 17k per-month increase since April and the heavily exposed manufacturing sector posting job losses for 7 straight months. The unemployment rate jumped to 4.6% in November from 4.4% in September (the October unemployment rate could not be calculated due to the government shutdown that month.) That was the highest unemployment rate in more than 4 years, although current market consensus is looking for a tick lower to 4.5% in December.