{kind=link}

Week in review

The US stock markets started 2026 on a high note, with the S&P 500 and Nasdaq rallying on the first trading day thanks to renewed investor confidence.

Technology companies led the comeback, with giants like Nvidia and Broadcom posting strong gains after a few difficult days at the end of December. Although the market missed out on the traditional year-end “Santa Claus rally,” the longer-term picture remains very strong; all three major indexes finished 2025 with double-digit growth, marking their third straight year of profits.

The Dow Jones specifically closed out the year with an eight-month winning streak, fueled largely by the exploding demand for artificial intelligence technology.

On the FX front, the US dollar began 2026 with a slight recovery, rising 0.12% on Friday after a challenging performance last year.

In contrast, the Euro slipped by 0.11% to $1.1732, hurt by news that European factory activity has dropped to a nine-month low. Despite this slow start, both the Euro and the British Pound, which also dipped slightly today are coming off their strongest annual gains since 2017.

Overall trading activity remained quiet especially in the Asian session as markets in Japan and China were closed for the holiday.

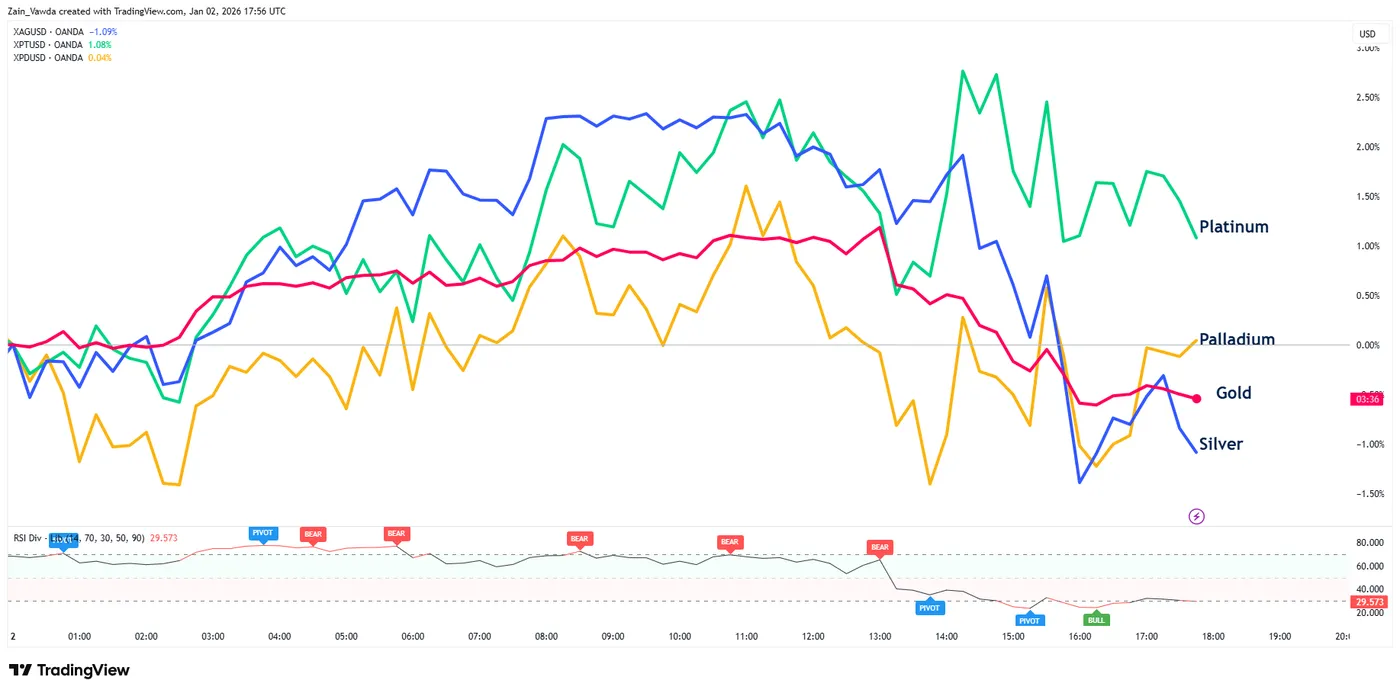

Commodities started the day eyeing a recovery following the recent selloff. Gold traded briefly above the $4400/oz before the precious metal wiped out the majority of its daily gains.

Silver is down around the 1% mark on the day while Platinum is up just over 1%.

Palladium has struggled but is eyeing a move into positive territory, finally.

Source:TradingView

The Week Ahead

The first full trading week of 2026 marks a sharp transition from the quiet holiday season to a busy schedule of critical economic reports. Market participants are moving on from a strong year where major US stock indexes rose between 16% and 20%, now facing an economy that feels unstable and uneven.

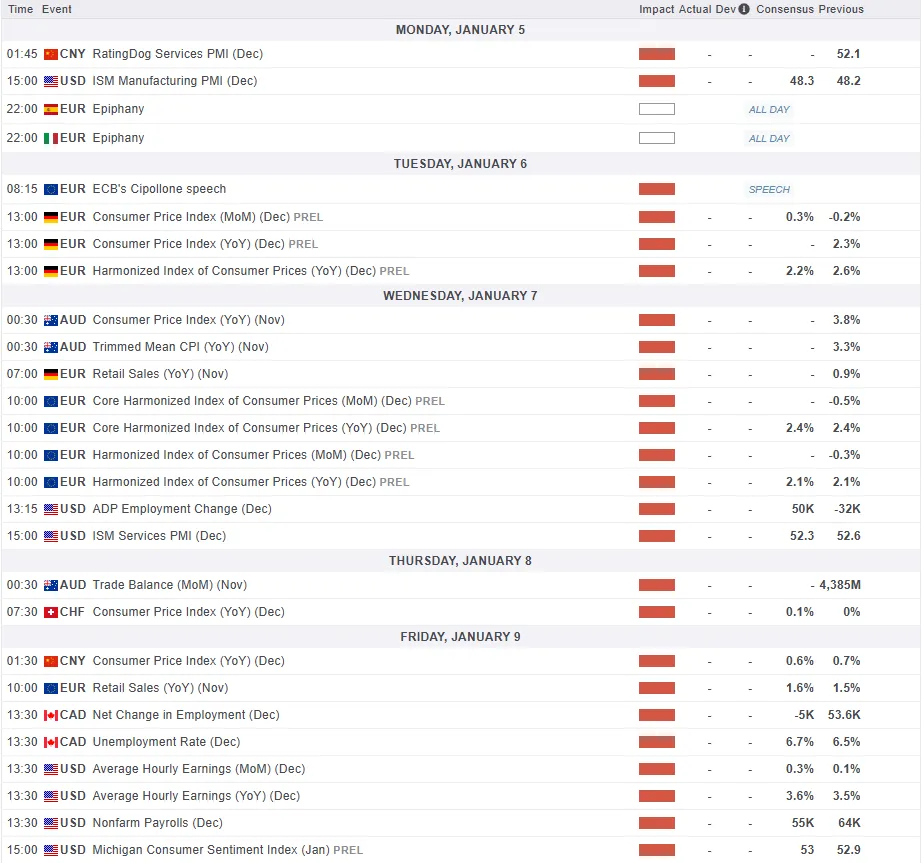

The coming week will be dominated by the December US jobs report, manufacturing data from both the U.S. and Europe, and updates on how UK retailers performed over Christmas. These events are happening against a backdrop of stubborn inflation near 3% and growing worries about labor shortages and new trade tariffs.

US Markets – Deciphering the “Low-Hire, Low-Fire” Paradigm

The main event for this week is the US employment report coming out on January 9, 2026.

This follows a year where hiring gradually slowed down, and experts predict the economy added about 55,000 jobs in December similar to November’s modest numbers.

However, the way analysts interpret this data is changing significantly. J.P. Morgan notes that because of stricter immigration rules and an aging population, the economy now needs far fewer new jobs to keep unemployment stable. The number of jobs needed to maintain the status quo has dropped from 50,000 a month to as low as 15,000.

Consequently, even a relatively low gain of 55,000 jobs would be strong enough to lower the unemployment rate, which is expected to dip from 4.6% to 4.5%

The current “stagnant” job market where companies are neither hiring aggressively nor firing workers is largely due to business uncertainty caused by changing trade rules and a recent government shutdown.

As a result, most new jobs in December are expected to come from stable industries like healthcare and shipping, while construction and manufacturing struggle under high costs. This cooling labor demand allowed the Federal Reserve to cut interest rates late last year, bringing them to a range of 3.5% to 3.75%.

While market participants do not expect another cut in January, there is currently a 50% chance of a cut in March.

However, if the upcoming jobs report is surprisingly weak, it could spark fears of a recession and lead investors to bet on faster interest rate cuts.

In the UK, in the United Kingdom, the first full week of January is synonymous with the “Golden Quarter” post-mortem. The retail sector, a cornerstone of the UK economy, faces a rigorous assessment through a series of trading updates from its most prominent entities: Next, Marks & Spencer, Tesco, and J Sainsbury.

These reports will offer the first definitive look at how consumers responded to the festive season amidst a backdrop of rising employment costs and a potential “price war” in the grocery sector.

This may have a bigger impact than usual on indices after the FTSE 100 passed the 10000 point mark for the first time this week.

Asia Pacific Markets

In the Asia-Pacific region, the week of January 4 is characterized by the return of full market participation following the extended New Year bank holidays in Japan.

Market participants are closely monitoring the Bank of Japan this week. While the bank is expected to proceed cautiously, new wage data arriving on January 7 could speed up interest rate hikes if earnings are higher than expected, which would strengthen the Japanese Yen.

Attention also turns to China, where inflation data released on January 9 is expected to highlight ongoing problems with falling factory prices. Before that, a key trade report on January 8 will show how well China is coping with global trade tensions; despite new export restrictions on steel and electric vehicles, experts still forecast a massive trade surplus of over $100 billion.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Chart of the Week – S&P 500

From a technical perspective, the S&P 500 has seen a decent pullback over the last 5 trading days.

This has brought the index close to a key confluence level where the 100-day MA and ascending trendline converge.

This is around the 6800 handle and could see the index print a higher low before moving higher once more.

If this level breaks, support may be found at 6675 and 6650 respectively.

On the upside, resistance rests at 6900 before the all-time highs at 6950 comes into focus.

S&P 500 Daily Chart, January 2, 2026

Source:TradingView.Com (click to enlarge)