{kind=link}

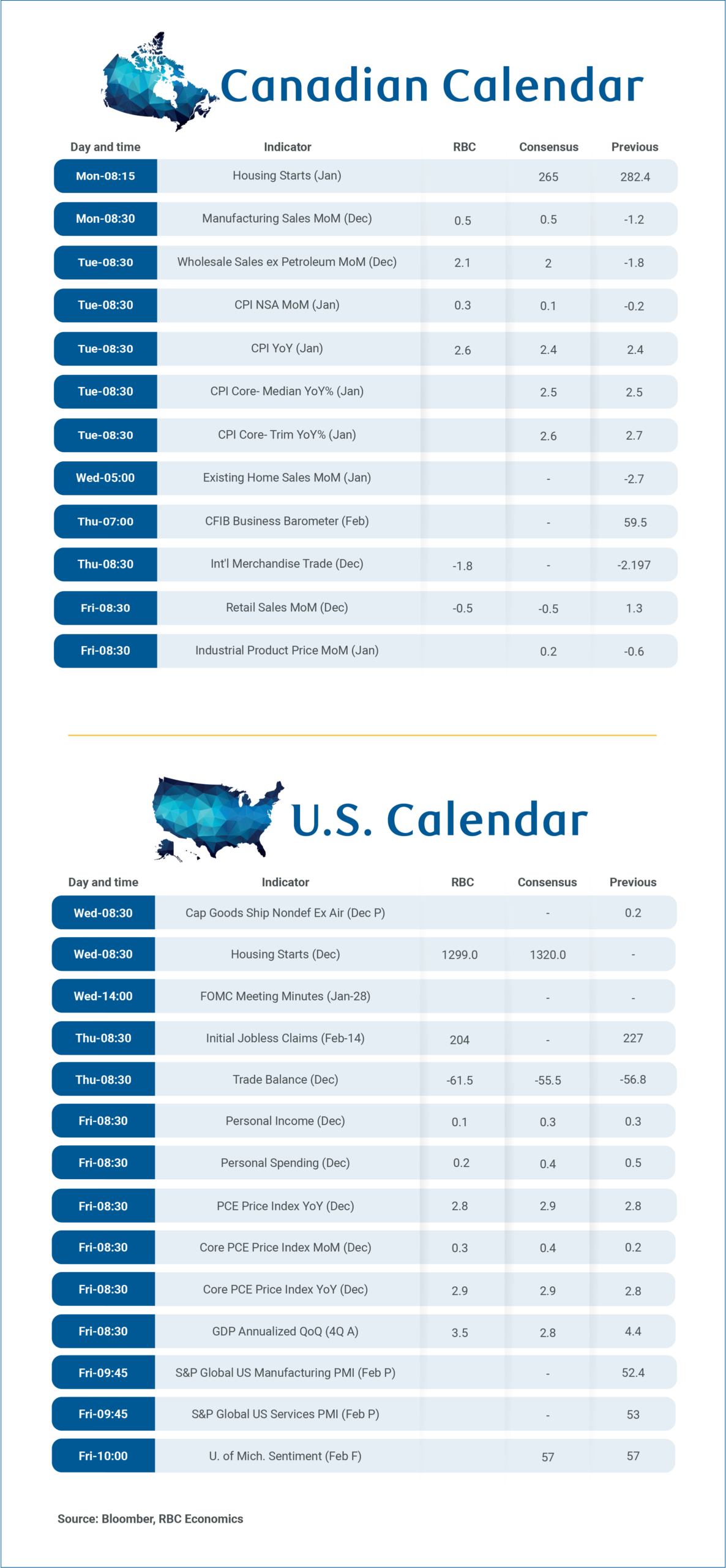

A packed Canadian economic release calendar in the coming week should reveal a partial recovery in auto production, a slightly narrower trade deficit in December, and further evidence that underlying inflation remains above the Bank of Canada’s 2% target despite edging lower.

International trade, manufacturing and wholesale sales reports should reinforce that some heavily trade exposed subsectors of the economy are still being significantly impacted by U.S. tariffs. But a sharp 20% drop in motor vehicle production in November—driven, at least, in part by semiconductor shortages—partially reversed seasonally adjusted in December. Advance estimates from Statistics Canada showed manufacturing sales up 0.5%, and wholesales 2.1% higher after falling in November.

Canadian exports tracking lower for 2025

The tick up in in motor vehicle production should also partially retrace November’s 11.6% drop in motor vehicle and parts exports. However, exports outside of autos likely remained depressed. Declining oil prices weighed on energy exports, and a surge in metal exports from November may also have partially reversed in December.

We look for the Canadian merchandise trade deficit on Thursday to narrow slightly to -$1.8 billion from -$2.2 billion in November.

Overall, 2025 proved exceptionally volatile for trade flows with U.S. inventory builds boosting exports earlier in the year before falling after tariffs took effect. For the full year, Canadian goods’ exports are tracking lower by approximately 2.5% from 2024.

Food prices and tax distortions to drive inflation higher

Tuesday’s Consumer Price Index report for January should show a tick higher in Canadian headline inflation to 2.6%, largely due to tax-related distortions — the prior year’s GST/HST holiday was not repeated this year – alongside still elevated grocery price growth.

Food price growth could spike above 7%, driven by rising restaurant costs compared to tax-exempt levels a year ago. But, grocery store price growth also likely remained high after hitting 5% in November. Energy prices, meanwhile, are tracking 11% below a year ago with gasoline down 17%—roughly half attributable to the removal of the carbon tax.

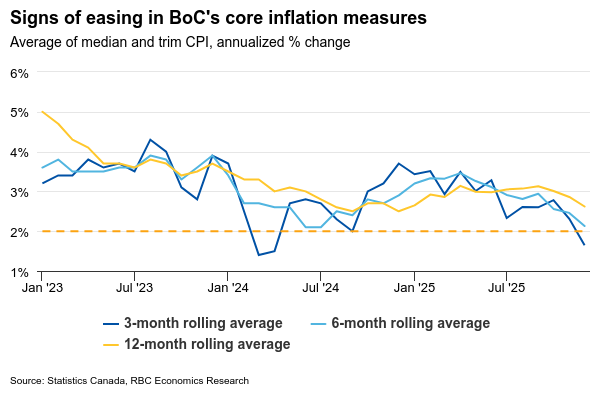

The BoC has limited control over global commodity trends affecting energy and food prices. The central bank will continue monitoring broader underlying price growth measures more closely. Median and trim CPI measures, which exclude indirect tax impacts, are expected to hold around 2.5% year-over-year—and have been gradually edging lower—but remain above the 2% target.