rose at its fastest monthly pace in nearly a year. The inflation report comes at a pivotal moment, as reports that the Trump administration may scale back its steel and aluminum tariffs suggest the administration is conscious of inflation risks.){kind=link}

Canadian Highlights

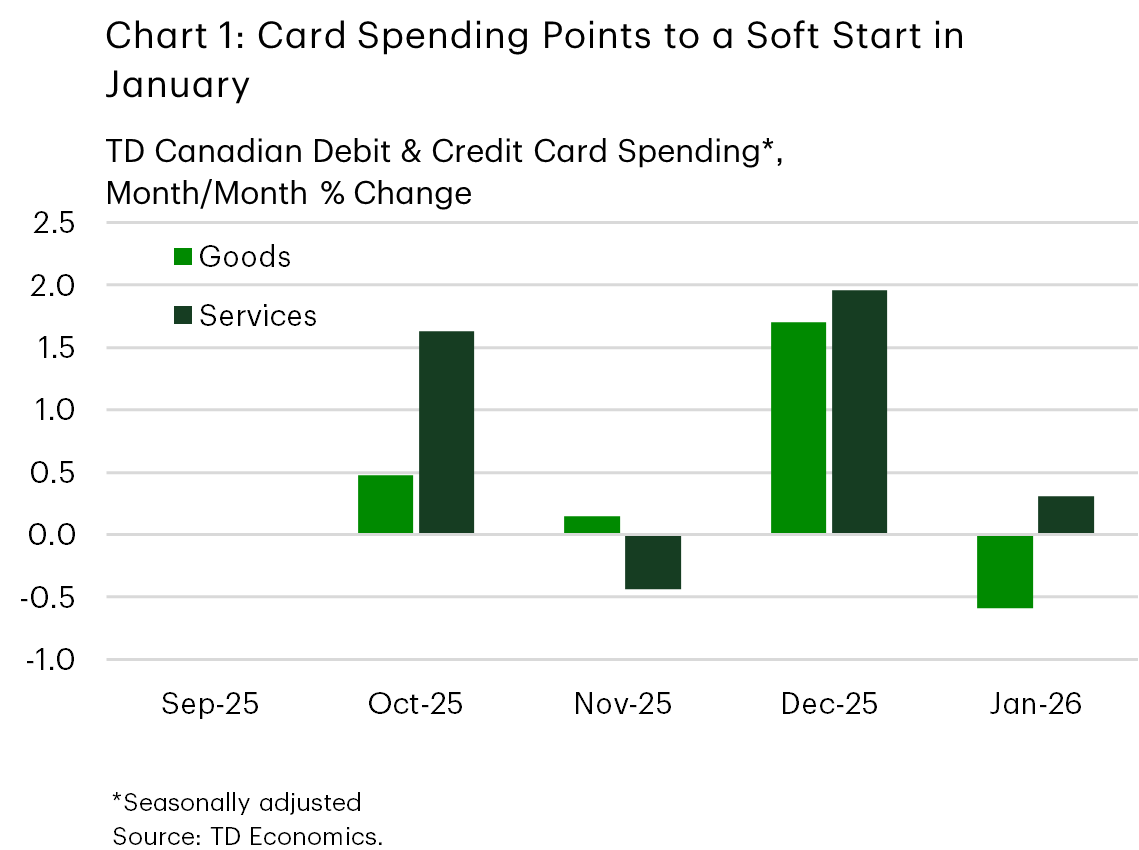

- The economic calendar was bare this week, but internal card spending data offered a glimpse into consumers early in 2026, suggesting a soft start to January.

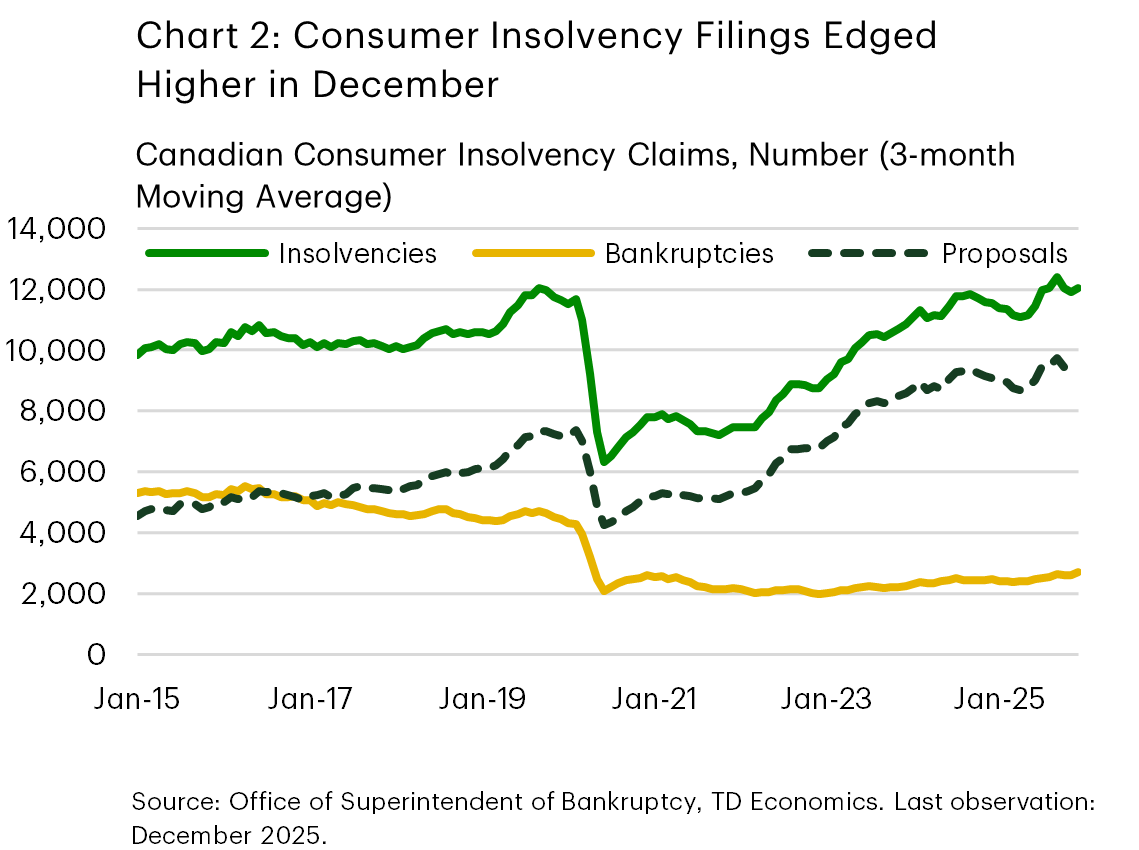

- December insolvency data showed that the three-month moving average trend in consumer filings started to rise again – worth watching, but not yet alarming.

- The next week promises to be far more eventful with a slew of data releases. With risks to inflation looking balanced ahead of January’s CPI update next week, we think the Bank of Canada has enough reason to stay on hold when it meets in March.

U.S. Highlights

- Financial markets sold off this week as developments in AI and tech raised doubts about future earnings.

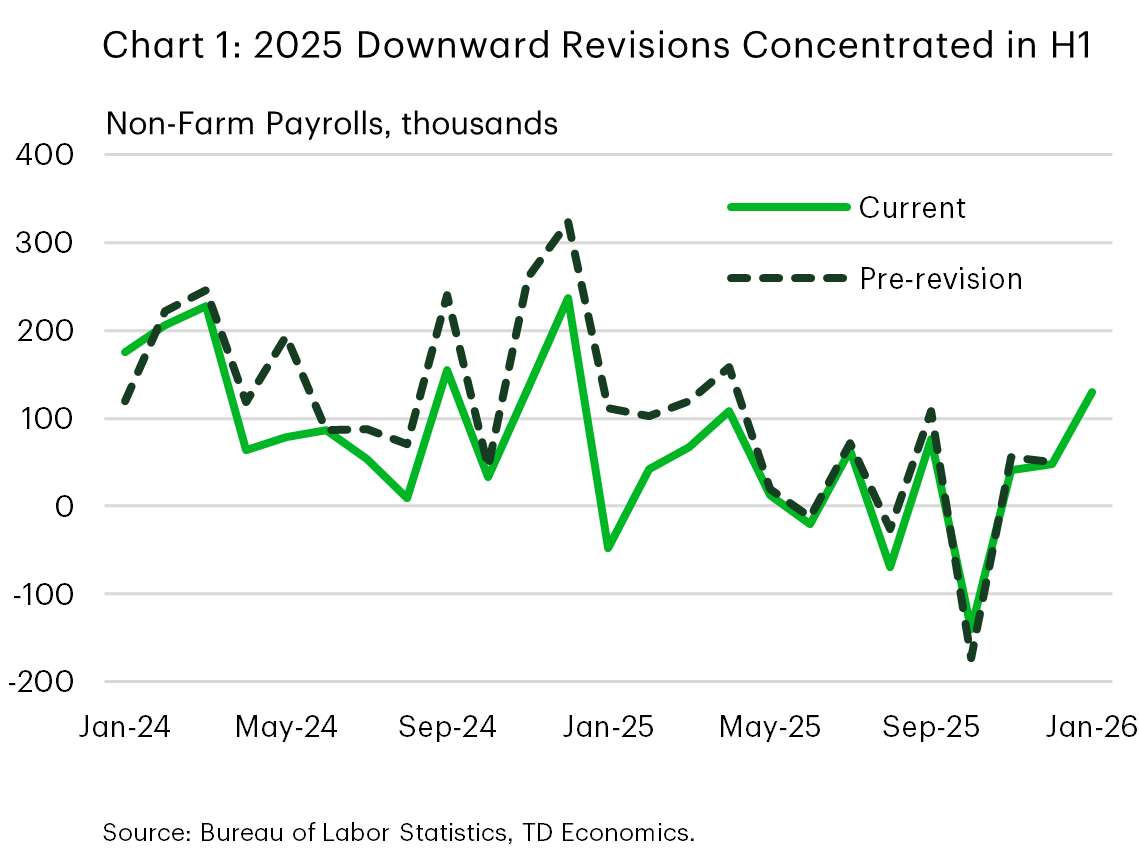

- January’s employment report delivered a clear upside surprise, easing concerns that the labor market was rolling over after last year’s slowdown.

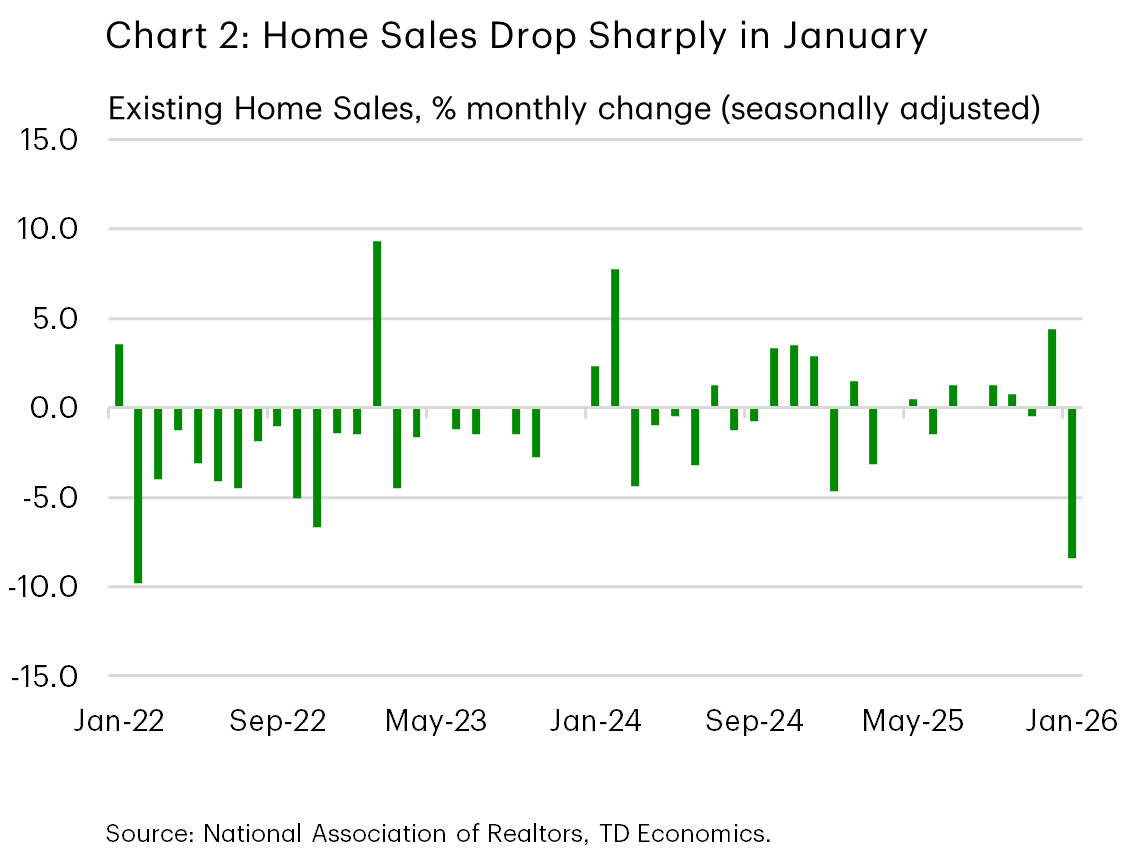

- In other important data releases, there were softer signals from consumer spending and housing. Inflation had a softer-than-expected headline number, but some cautionary signs of inflation pressures in the core.

Canada – A Week to Reflect

The shooting in Tumbler Ridge overshadowed all else this week, as Canadians mourned the victims of this tragedy. As a result, the Prime Minister postponed his planned defence-industrial strategy announcements, and with no economic data on the calendar, the week was somberly quiet.

Markets, though, kept moving. Canadian equities fluctuated over the week but are set to finish with more than 1% gain. The bond markets followed suit, with the 10-year Government of Canada yield falling roughly 15 basis points to 3.25% (yields move inversely to prices).

With the data calendar bare, it’s a good moment to step back and frame the bigger picture. We expect Canada’s economy to remain lukewarm in 2026, with a bit more heat by year-end. Our forecast sees the economy ending next year about 1.4% larger than in 2025, although with the coming CUSMA review likely to be bumpy, the risks to growth are tilted to the downside.

Business investment remains subdued amid lingering trade uncertainty and slower population growth is capping employment gains. But there are also reasons for optimism. Government spending is poised to provide support toward the end of 2026, and household spending remains one of the more stable pillars of the economy. TD card spending data point to a relatively solid December, with gains concentrated in services – particularly recreation and travel (Chart 1). Travel stayed strong in January too, as Canadians fled the winter storms for warmer destinations. Card spending on goods was firm in December, but softened in January, likely reflecting weather-related disruptions and reduced willingness to venture out. This sits somewhat at odds with the December retail sales flash estimate, which signaled a contraction. But auto sales, which were soft according to industry data, are included in retail sales and likely explain the gap. We also see a pullback in holiday-related categories such as clothing and electronics after strong December gains.

Above-trend growth in personal income and solid wealth gains helped support this spending. Still, not everyone is on solid ground. December insolvency data consumer filings rose 16% month-on-month. On a three-month moving average, filings rose 1.6%, reversing declines in the prior two months (Chart 2). The increase was driven by consumer proposals, though bankruptcies edged higher as well. While this bears watching, the trend is not yet alarming. Population-adjusted insolvency rates remain below pre-pandemic levels. Notably, bankruptcies are still historically low, with most of the rise coming from proposals – a mechanism that allows households to retain assets, maintain structured repayment plans, and face a comparatively milder hit to credit ratings.

Despite being short, next week promises to be far more eventful, with releases on inflation, merchandise trade, housing starts, home sales, and retail trade. Inflation bears close watching ahead of the Bank of Canada’s rate decision on March 18th. With inflation risks roughly balanced ahead of next week’s CPI, the central bank is right to share the Valentine’s Day spirit: committed but not quite ready to make a big move.

U.S. – Markets Blink, Jobs Hold Firm

Financial markets endured a rough patch this week, with a broad sell off across equities reflecting anxiety about the threat AI could pose to earnings and employment, the path of interest rates, and the durability of the ongoing expansion. That market reaction stood in contrast to the message from the January employment report. Payrolls growth came in well ahead of expectations, accompanied by a further dip in the unemployment rate. While revisions did reveal that job growth over much of 2025 was weaker than previously thought, the January rebound suggests that labor demand remains intact (Chart 1).

The rest of the data flow painted a more mixed picture of the economy. Headline CPI inflation came in softer than expected this morning, but core CPI picked up the most since August. Services inflation heated up while core goods inflation (excluding used vehicles) rose at its fastest monthly pace in nearly a year. The inflation report comes at a pivotal moment, as reports that the Trump administration may scale back its steel and aluminum tariffs suggest the administration is conscious of inflation risks.

Retail sales ended 2025 on a soft note. December sales were flat after a solid November, and downward revisions tempered the momentum implied by earlier releases. Housing data were also notably weak. Existing home sales posted their largest monthly decline in nearly four years in January, reflecting a combination of affordability constraints and bad weather (Chart 2).

Markets, meanwhile, struggled to reconcile the week’s macro data with a less accommodating policy backdrop. The equity sell off reflected concerns about growth-sensitive sectors and fear that advancements in AI may dislodge large incumbents across a wide swath of the economy, and a reassessment of the path for interest rates following a string of Fed communications. Market pricing for the Federal Reserve to reduce rates in its June meeting have fallen from 60% to around 50% over the course of this week. Speeches this week from Federal Reserve officials revealed a balance of opinion. More hawkish voices stressed that inflation remains above target and warned against premature easing, while others acknowledged that, even with a strong jobs report, there is still an argument for rate cuts later this year if disinflation continues. On balance, we read the prevailing sentiment from Fed officials as one of patience rather than urgency, but still hold on to our call for a rate cut in June. This morning’s softer CPI release may help move the Fed’s perceived balance of risks slightly towards easing, particularly if the disinflationary pressure were to persist over the coming months.

Looking ahead, our eyes will be on next week’s release of the FOMC meeting minutes, which should provide additional insight into how policymakers have been weighing inflation risks against signs of labor market stabilization. And next Friday’s PCE inflation and consumer spending data will be helpful in assessing the durability of consumer spending and the extent of momentum in recent inflation data.