{kind=link}

A touch stronger than expected, with minimal risk to our March quarter estimates.

- Electricity and garments & footwear boosted the January CPI more than expected.

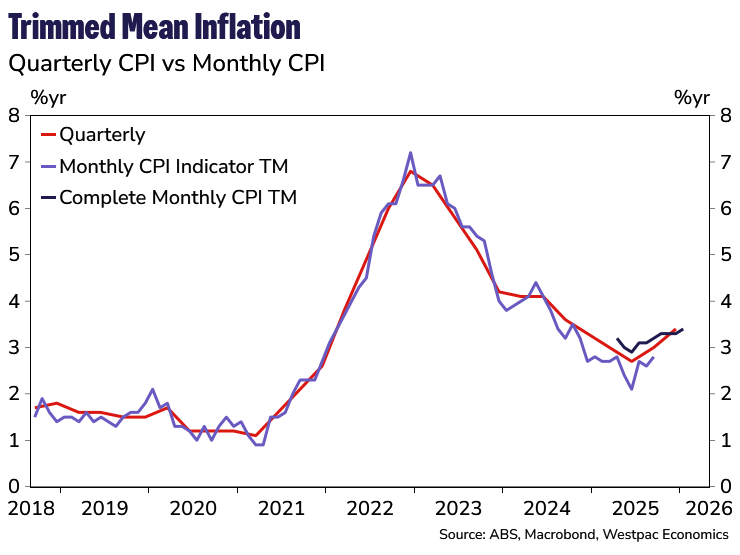

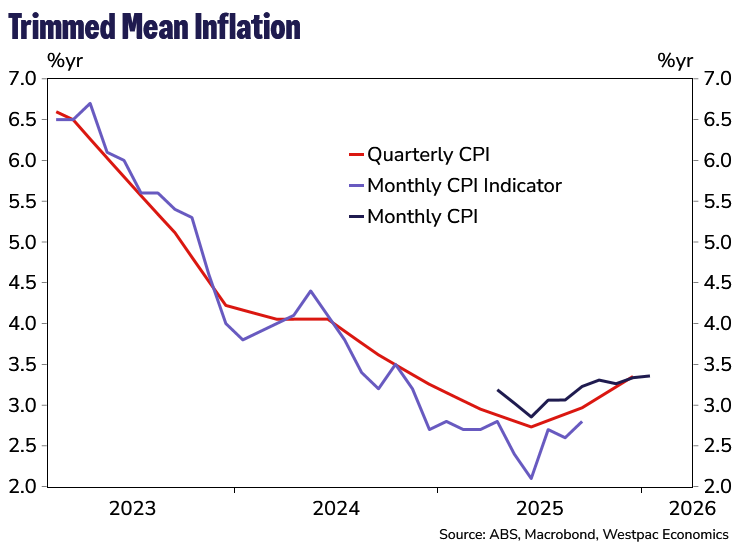

- In the month the Trimmed Mean was as expected with revision resulting in a modest uptick in the annual pace to 3.4%yr.

- Our preliminary review of the January Monthly CPI suggests little risk current inflation profile.

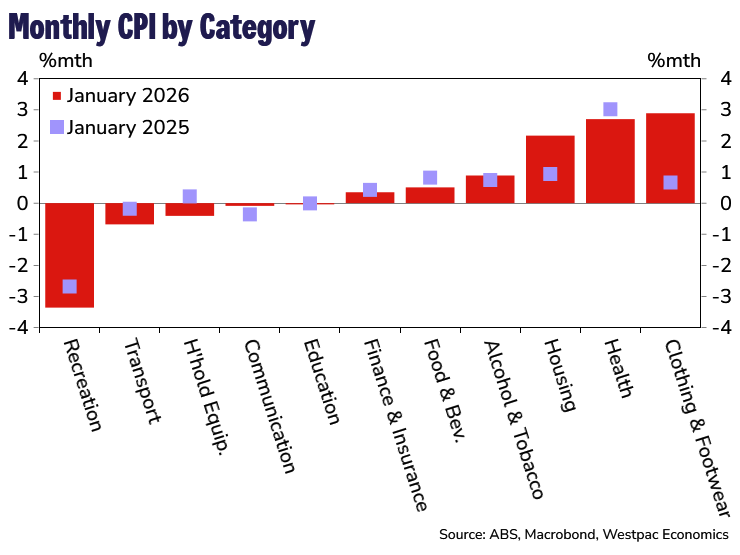

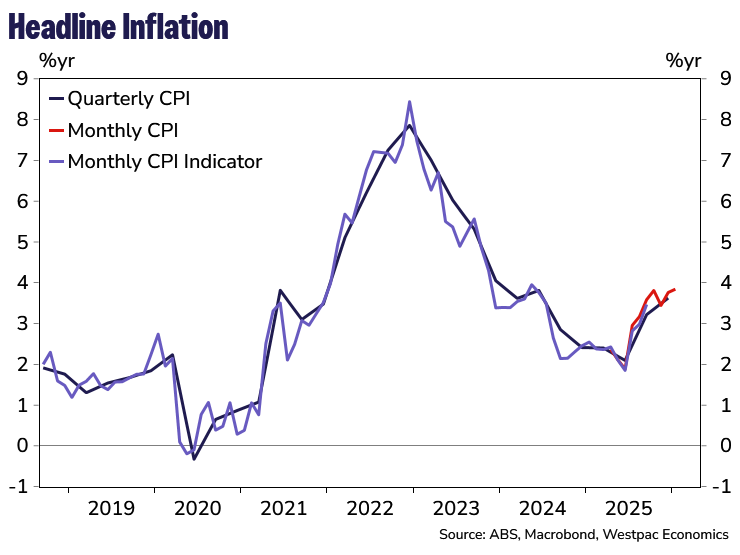

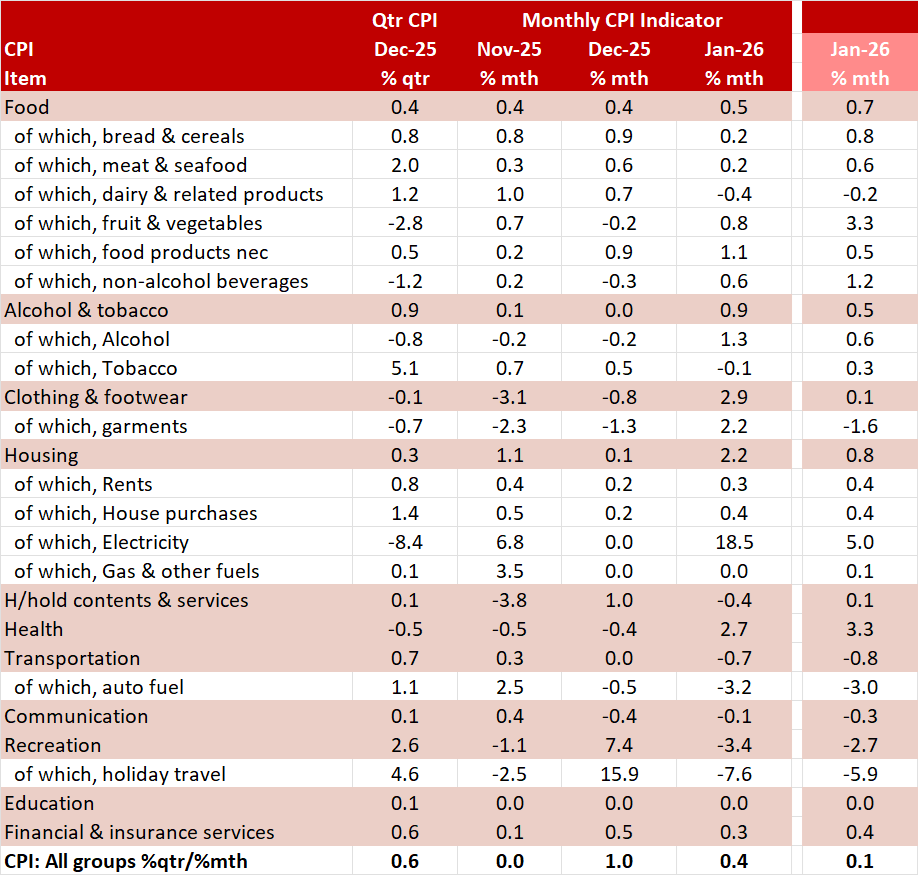

We start 2026 with a complete Monthly CPI. In January the CPI gained 3.8% in the year, a touch stronger than Westpac’s estimate of 3.6%yr and the market estimate of 3.7%yr. In the month, the CPI lifted 0.4%, stronger than Westpac’s published near-cast of 0.1% on the back of stronger than expect gains in electricity and garments & footwear offset somewhat by a larger than expected fall in holiday travel and a smaller than expected rise in health.

January is seasonally a soft month with the seasonally adjusted CPI lifting 0.5% in January. Due to the short history of the new monthly expenditure class series, we expect to see ongoing revisions to the CPI seasonal factors with the ABS fine tuning the process as they gather more data. In the December release the ABS estimated a seasonal impact of 0.3% in January, this was reported as 0.1% in the January release. Remembering that the Trimmed Mean is seasonally adjusted, this suggests we should expect to see revisions to the Trimmed Mean until the seasonal adjustment process is more mature.

The Monthly Trimmed Mean (TM) measure was up 3.4% in the year to January, Westpac and the market had estimated 3.3%yr, which is up a touch from 3.3%yr in December.

The TM lifted 0.3% in the month of January, on par with Westpac’s estimate of 0.3% with the higher than expected annual pace due to revisions. The monthly TM has printed 0.3%mth in five of the last six months. This month expenditure classes trimmed off the top included electricity, insurance, garments, child care, veterinary services and take away & fast foods. Trimmed off the lower bound in January included automotive fuel, vegetables and other non-durables.

As Michael Plumb, Head of Economic Analysis Department at the RBA noted in a speech this week, the RBA is using the expanded monthly data to evaluate and compare underlying inflation measures and is examining bias, seasonality, responsiveness and leading properties with a view of eventually moving to a monthly measure of core inflation. But it will take time to understand the properties and seasonal patterns of the data. As such the Bank will continue to focus on the quarterly CPI for forecasting and assessing underlying inflationary pressures.

Consistent with out preliminary review we see little risk to our current inflation profile. Our current estimate for the March quarter TM is 0.9%qtr, lifting the annual pace very slightly to 3.5%yr from 3.4%yr. Our March quarter CPI estimate is 1.1%qtr with the annual pace lifting from 3.6%yr to 3.8%yr as the energy rebates roll off boosting electricity prices in the CPI.

January Monthly CPI Indicator in more detail

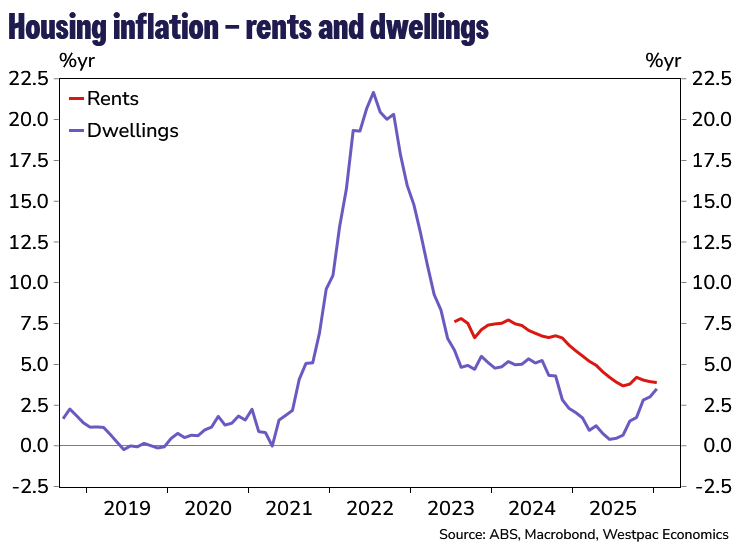

Rents were a touch softer than expected lifting 0.3% vs. Westpac’s 0.4% estimate. We are closely watching rents to see if this modest trend continues as expected. Dwellings gained 0.4% in the month, on par with our expectations as we note a strengthening trend which is likely to continue through the first quarter of 2026. The ABS notes that project home builders in some cities have raised base prices in response to increased demand and to pass through higher labour and material costs.

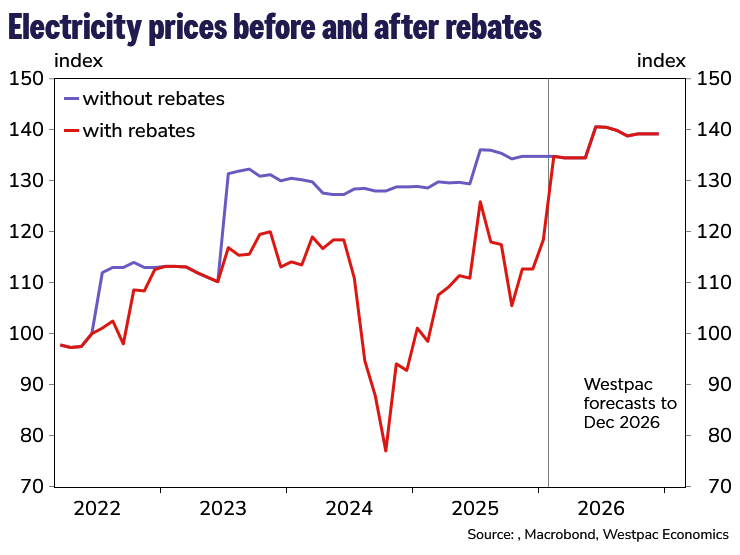

Electricity gained 18.5% in January compared to our forecast for 5.0% with the rise this month driven by households using up the extended EBRF rebates. This has seen the gap between electricity prices reported in the CPI, and the prices before rebates, almost close as it is now just 0.9%. We would expect this gap to close in February and without any new rebates, electricity prices will return to more normal pricing arrangements.

Holiday travel & accommodation fell –7.6% in January, a bit more than our estimate of –5.9% due to a –16.3% decline in international travel being only partially offset by a small 1.3% increase in domestic travel.

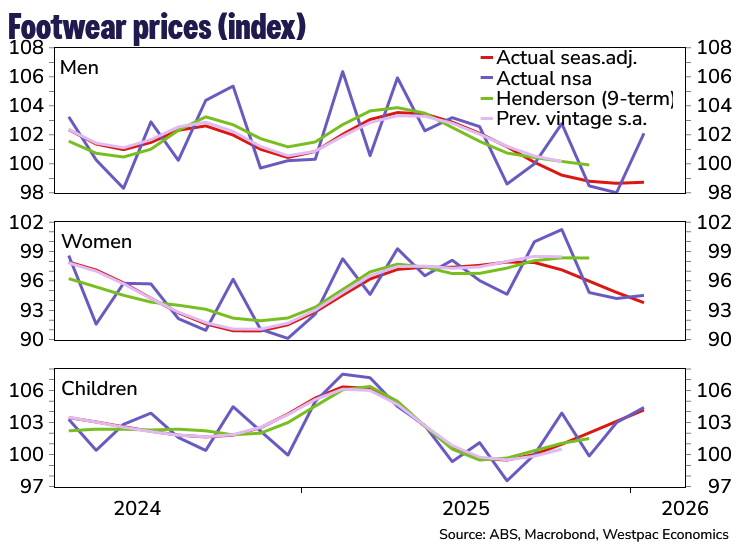

A key upside surprise was in clothing & footwear which gained 2.9% in the month compared to our estimate of 0.1%. Most of this discrepancy was due to garments which lifted 2.2% vs. Westpac’s expectation for a seasonal –1.6% decline. Also of note was a robust 4.2% increase in footwear for men and a 5.7% gain in accessories.