{kind=link}

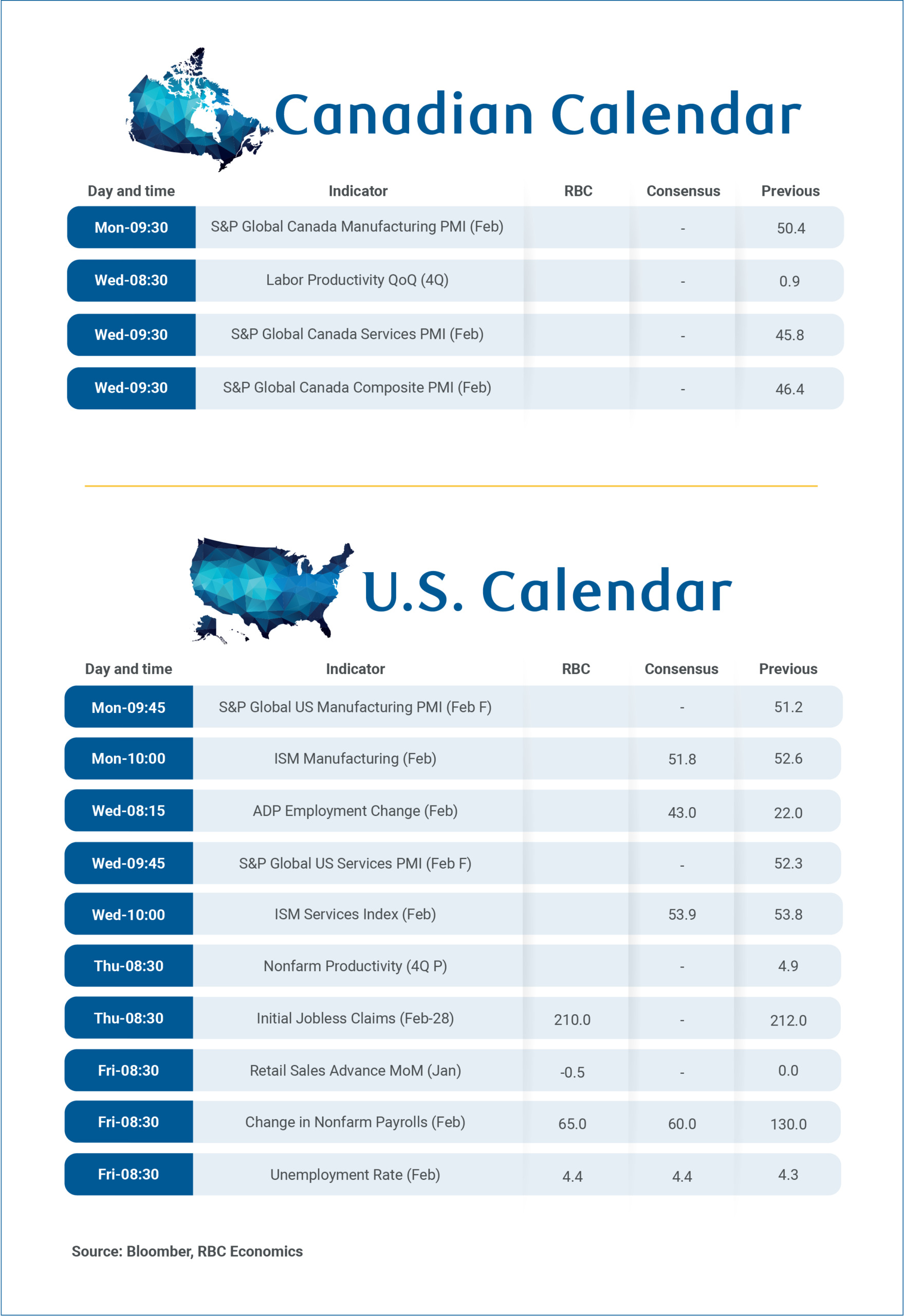

A quiet Canadian economic data calendar will leave focus on U.S. jobs next Friday—particularly on the disproportionately trade impacted industrial sector where cross-border economic ties with Canada are closest.

We look for the February report to be consistent with stabilizing broader U.S. labour market conditions. We expect the unemployment rate to tick up to 4.4% to reverse a decline to 4.3% in January, but hold below the recent 4.5% peak in November.

Job growth likely remained subdued (we expect a 65,000 increase), but slow underlying labour force growth due to an aging population and immigration curbs has lowered the breakeven rate of employment needed to keep the unemployment rate from rising more significantly.

Employment in the heavily tariff-exposed U.S. manufacturing sector has underperformed—mirroring conditions north of the border given tight Canada/U.S. industrial integration. But, it posted a small increase for the first time since November 2024 in January.

For Canada, we’re watching the February S&P manufacturing Purchasing Manager’s Index on Monday after it ticked above the neutral growth 50 level in January for the first time in a year.

U.S. tariff regime shifting with rates edging lower

U.S. trade policies are in flux again after the Supreme Court ruled against the use of IEEPA to impose broad-based tariffs last week. The U.S. administration announced a new 10% global tariff via Section 122 on the same day as the ruling, citing balance-of-payments deficit concerns.

The administration has already threatened to raise that to 15% (maximum allowable under that authority), but the list of exemptions from the measures is also long. Critically for Canada, trade compliant with CUSMA rules of origin is exempt as it was under IEEPA rules.

There is a list of more than 1,600 products where tariffs don’t apply “because of the needs of the United States economy.” By our count, products on that exemption list accounted for roughly half of U.S. global imports in 2025. For some trade partners, that share is substantially higher—for example, the exemption list covers more than 80% of U.S. imports from Taiwan in 2025.

Accounting for the exemptions, the new Section 122 tariffs likely represent a step lower in the average effective U.S. tariff rate overall. This aligns with our expectation that U.S. tariff collection may have already peaked given elevated affordability concerns.

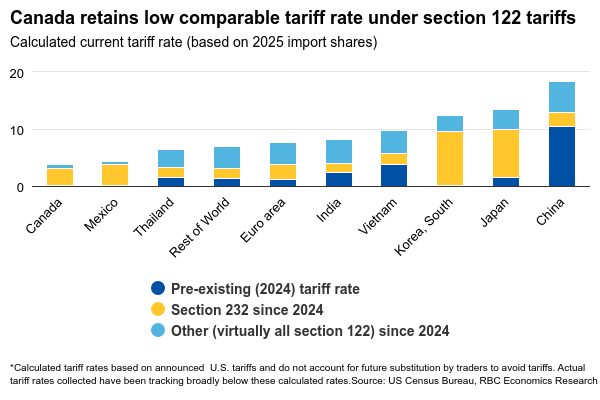

Canada’s tariff backdrop unchanged after court ruling

The new measures don’t significantly change the international trade backdrop for Canada.

CUSMA exemptions mean Canada should retain among the lowest average U.S. effective tariff, even as significant targeted tariffs remain in effect on products like steel, aluminum and the auto sector (measures not impacted by the U.S. Supreme Court ruling).

We’ve long highlighted the importance of preserving CUSMA and related exemptions to our Canadian outlook. But, the U.S. administration’s decision last week to uphold these exemptions underscores the agreement is mutually beneficial on both sides of the border—including lowering costs for the 22 U.S. states that counted Canada as their largest source of imports in 2025.