This is obviously a very fluid situation and as the facts on the ground evolve so too will the economic impact. As a framing, just bear in mind that, absent a prolonged war and major long-term disruptions to key shipping routes in the Strait of Hormuz, the impact on U.S. economic growth, inflation and monetary policy should remain modest. Of course, the opposite also could be true.

Our model simulations of 10% and 30% sustained increases in oil prices do not come close to generating a U.S. recession or markedly changing the trajectory for core inflation. Headline inflation does move higher via higher energy prices for the consumer, but the drag on real consumer spending and thus economic growth is muted in these scenarios (0.1-0.2 percentage points for the year).

Central banks typically look through oil-driven inflation shocks, and we expect this time to be similar. We expect the FOMC to take the long view, and the weekend’s events probably will not have a major impact on the Federal Reserve’s reaction function. Our forecast for 50 bps of rate cuts this year remains unchanged. Similarly, we are not making any changes to our G10 or EM central bank forecasts at this time. In the very near term, we expect central banks around the world to remain in wait-and-see mode as they await additional clarity on the geopolitical situation.

Below, the Team responds FAQ style to some of the most common questions we have received in the past 72 hours on this topic:

What happens to U.S. inflation in the wake of an oil-price shock?

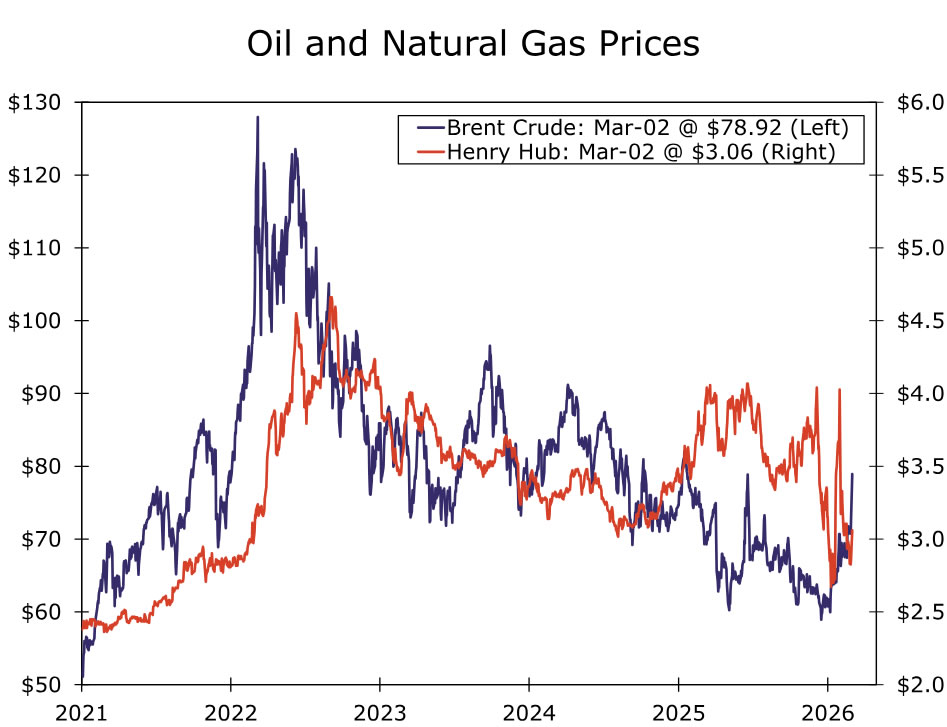

- Oil prices were already moving up over the past couple of weeks in anticipation of potential escalation, but the price of Brent crude has risen $7 since the U.S. strikes, or about 14% above its February average. Henry Hub natural gas prices are also up 6% in the wake of the strikes (Figure 1). Higher oil prices would need to persist to meaningfully impact the U.S. economy, as a sharp spike followed by a rapid normalization would not have much of an impact.

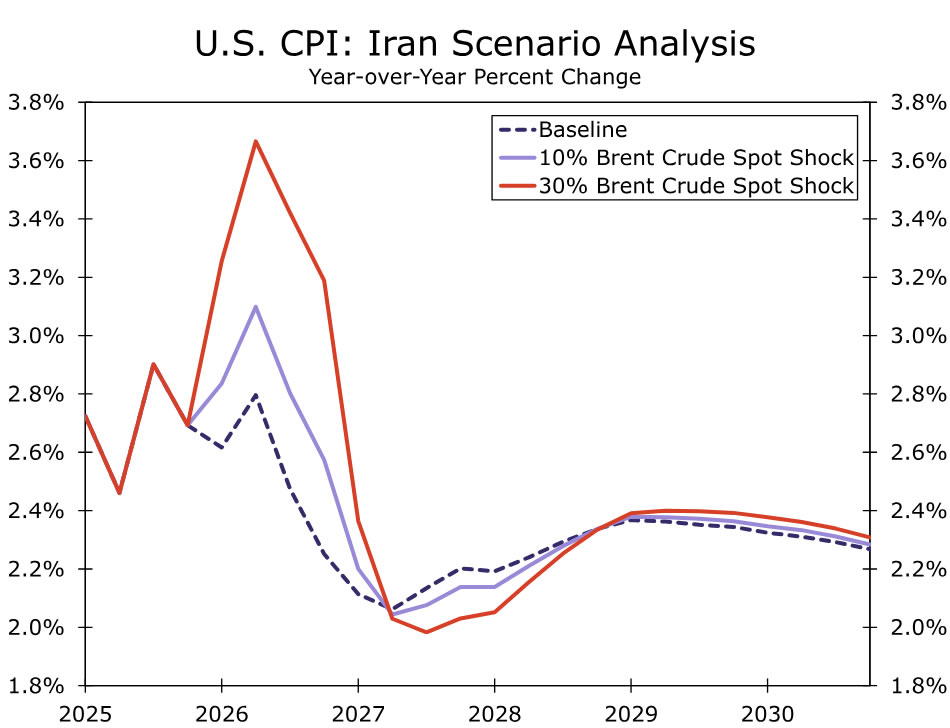

- To assess the potential U.S. macro impact from the military escalation, we run two scenarios: (1) a sustained 10% rise in Brent oil prices from a baseline expectation of around $65/barrel on average in Q1, and (2) a larger, sustained 30% rise in oil prices, which is closer to the spike that occurred immediately following Russia’s invasion of Ukraine in early 2022.

- A 10% sustained rise in oil prices would add roughly 0.3 percentage point to the year-over-year rate of headline consumer price inflation in the second and third quarter of this year, whereas a 30% rise would lift the one-year change closer to a full percentage point (Figure 2). The impact on core inflation would be much more modest (a few tenths with a 30% rise in oil prices) but not zero. This upward pressure on oil prices would reverse what has been one notable tailwind for disinflation and consumer spending over the past year; since last January, energy goods prices are down 7.3% compared to the 2.4% increase in headline CPI.

What does history say about consumer confidence sensitivity to energy spikes?

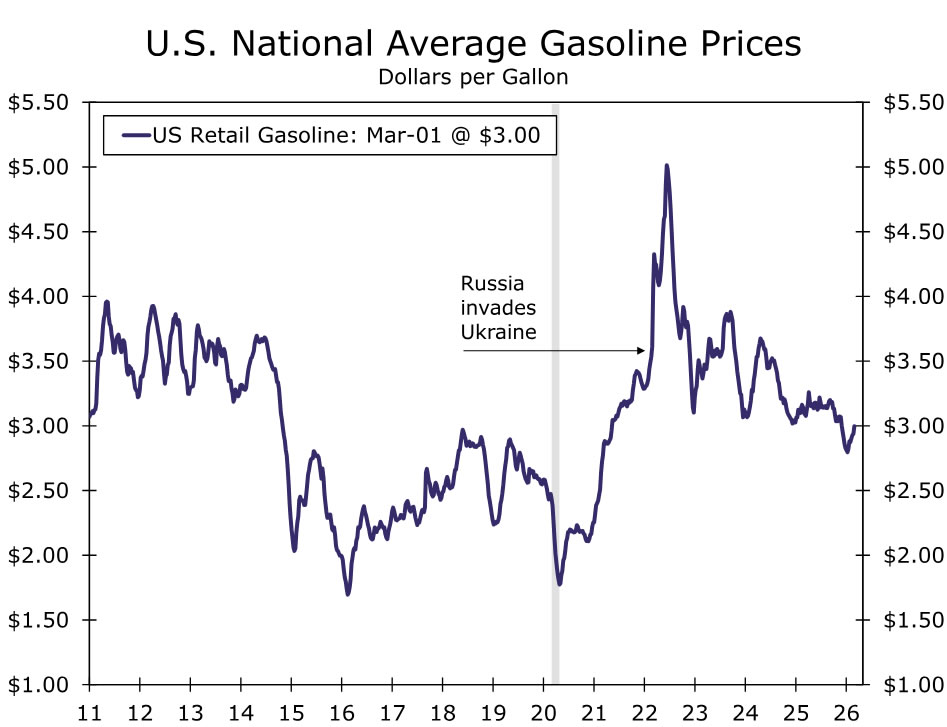

- U.S. consumer confidence tends to correlate more strongly with jobs and inflation than foreign conflict headlines. Of course, foreign conflict and inflation can also go hand in hand. That makes retail energy prices (mostly gasoline) the most important consideration for many households as it relates to this conflict. The average national price at the pump currently sits around $3/gallon. In the immediate wake of Russia’s invasion of Ukraine in February 2022, the average price initially jumped and remained elevated for around four months before receding (Figure 3). In the end, the fate of pump prices and the consumer’s reaction function will be dictated largely by any prolonged disruptions in the Strait of Hormuz.

How big of a hit could we expect an oil-price shock to have on U.S. economic growth?

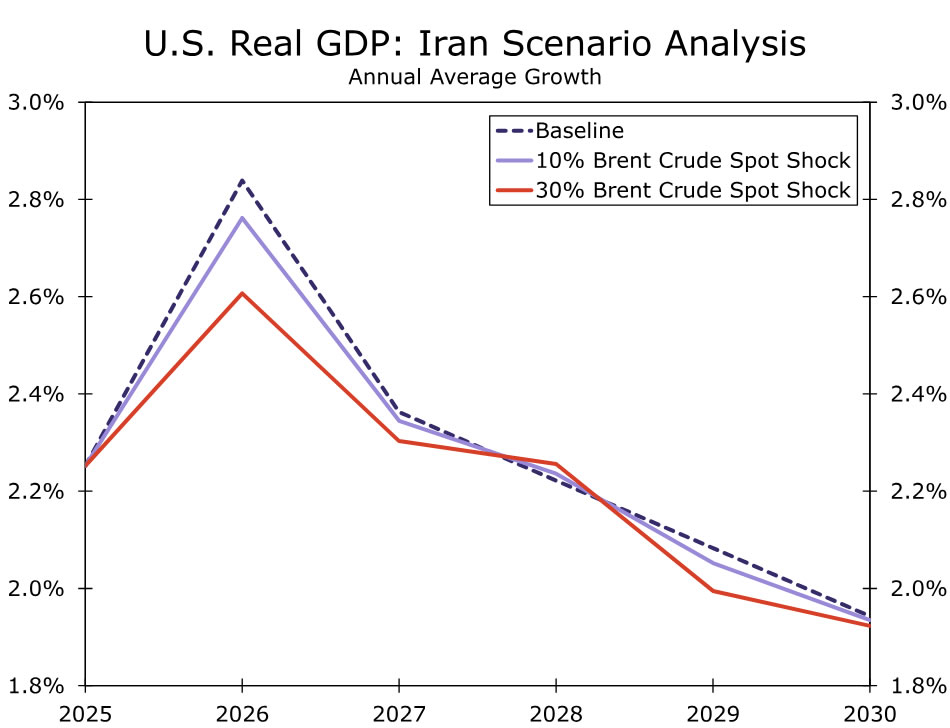

- Our model simulations suggest a 10% rise in oil prices would dampen average annual U.S. GDP growth by a very modest 0.08 percentage points (pp) this year (Figure 4), primarily through lower consumer spending with a 0.15pp reduction in real personal consumption expenditures growth. Business fixed investment spending actually rises modestly in this scenario, likely due to higher oil prices spurring some additional investment in domestic oil and gas production, which happened in the wake of Russia’s invasion of Ukraine. Even in the 30% price-shock scenario, the hit to real GDP growth this year is only 0.23pp. It takes very large and persistent gas price increases to meaningfully restrain household consumption.

Will a surge in commodity prices slow the U.S. tech build out?

- A temporary spike in oil and gas prices will pressure input costs but not meaningfully limit the pace of new data center construction. Higher energy commodity prices will likely flow through to building material and freight costs, representing a modest headwind to new development. Operationally, data centers are increasingly powered by natural gas, and while higher global LNG prices could have modest short-run negative cost implications, we generally do not see increased energy prices as a major limitation on new construction.

- The tech buildout relies on other trade routes. The Straight of Hormuz is a key energy chokepoint, but high-tech trade flows are minimal with the Straight of Malacca serving as the primary passage for global electronics, advanced chips, critical minerals and other inputs predominantly sourced from Asia. For the U.S., tech shipments from Asia are straight-shotted to West Coast ports or routed through the Panama Canal. So long as supply disruptions are contained to Hormuz, the negative effects on high-tech capex should be limited.

How will the Fed react to the conflict?

- The weekend’s events probably will not have a major impact on the Federal Reserve’s reaction function. A jump in oil prices would generate higher headline inflation, but this would be driven by a supply shock rather than overly hot aggregate demand. Accordingly, tighter monetary policy would do little to mitigate the hotter inflation and instead would further compound the hit to economic growth. In short, a supply-driven oil price shock is a classic example of something most FOMC officials will attempt to “look through.”

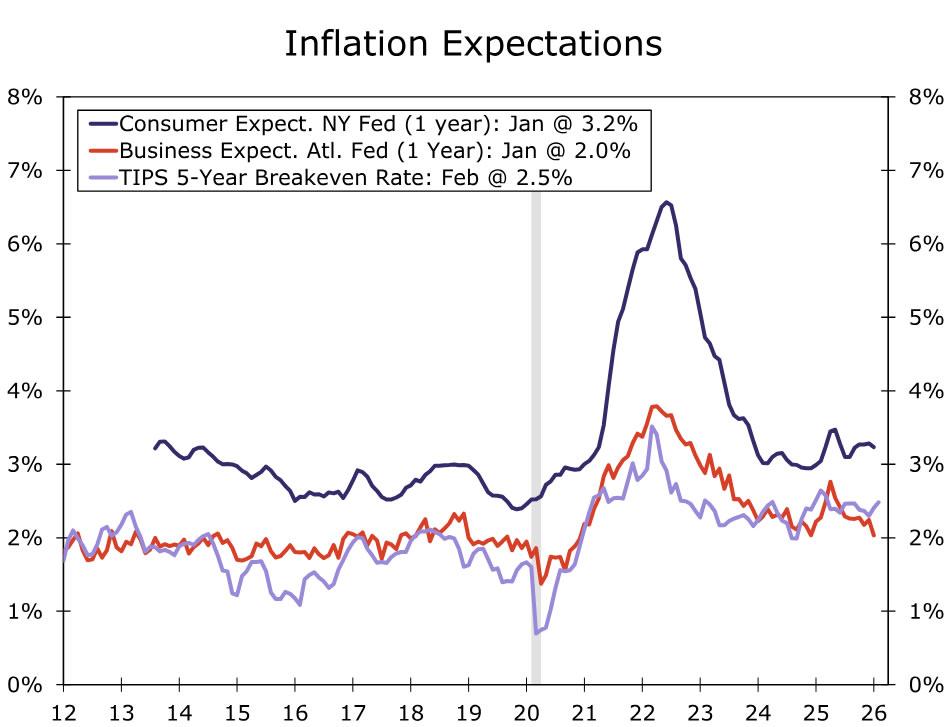

- Key will be the behavior of inflation expectations. The Fed will likely be sensitive to any notable deviations from what have been well-behaved inflation expectations. But again, any unanchoring here would stem from prolonged conflict and persistently higher energy prices. If higher prices in the short-run start to lead to higher expected inflation in the future, the inflationary shock can become more persistent. In 2021-2022, inflation expectations rose abruptly across a broad range of measures, causing the FOMC concern that the higher inflation of the time may not prove to be transitory (Figure 5).

Could more Fed easing be coming?

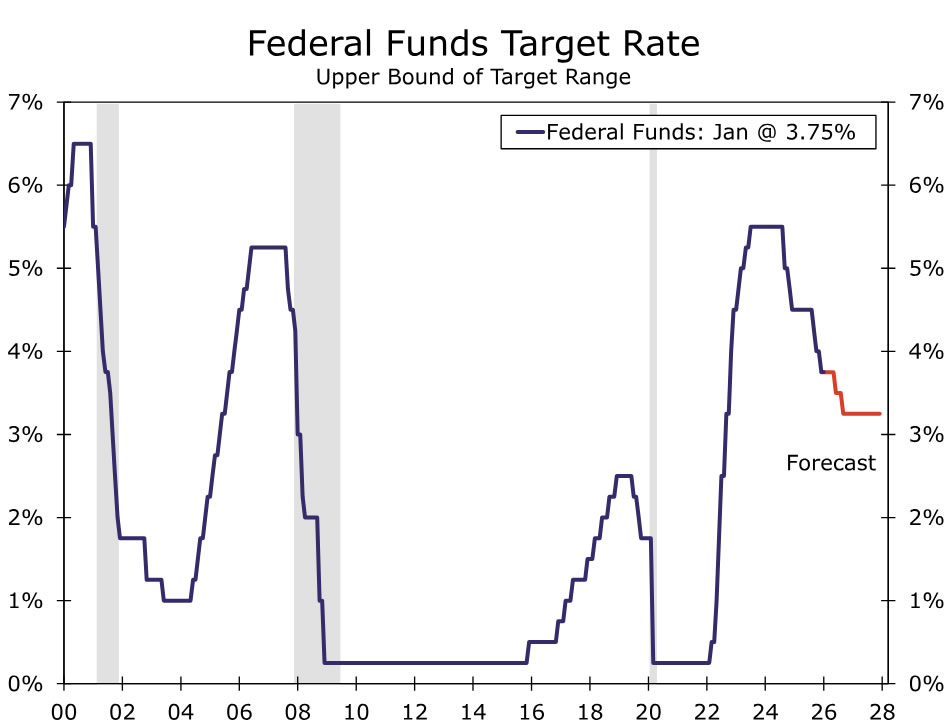

- We doubt more easing will be forthcoming than our base case projection of 50 bps (Figure 6). We expect the impact on the U.S. economy from the conflict to be modest, and we think the FOMC will take the long view on this rather than knee-jerk react in a foggy environment. While we suspect the FOMC will want to “look through” higher inflation from a jump in energy prices, they also may be wary about adopting accommodative monetary policy given the past five years (and counting) of above-target inflation. In the very near term, we expect the FOMC to remain in wait-and-see mode as they seek additional clarity on the geopolitical situation.

How will foreign central banks respond?

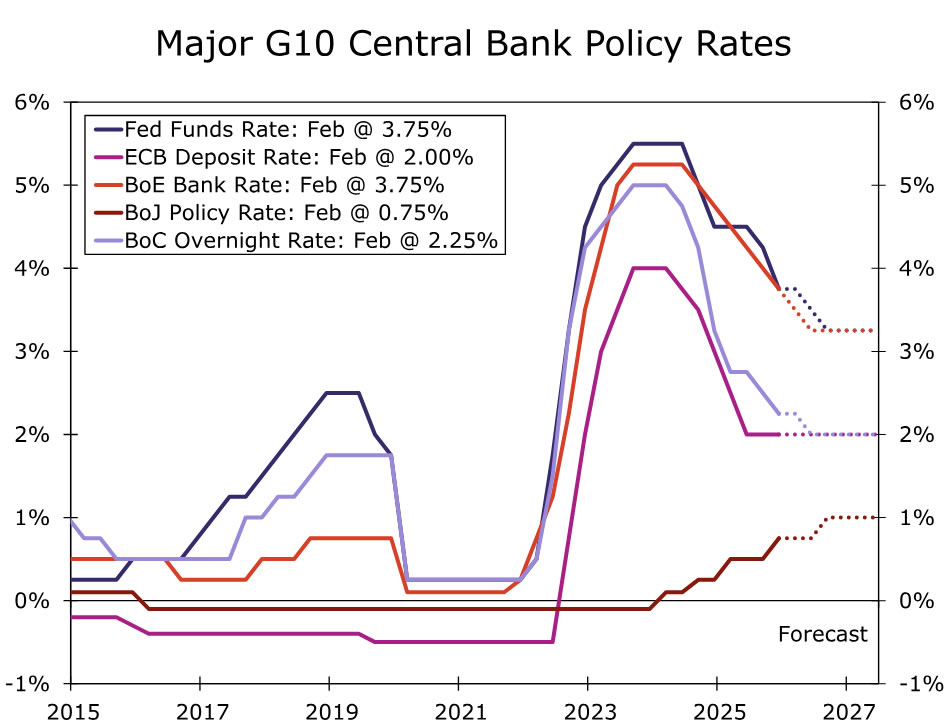

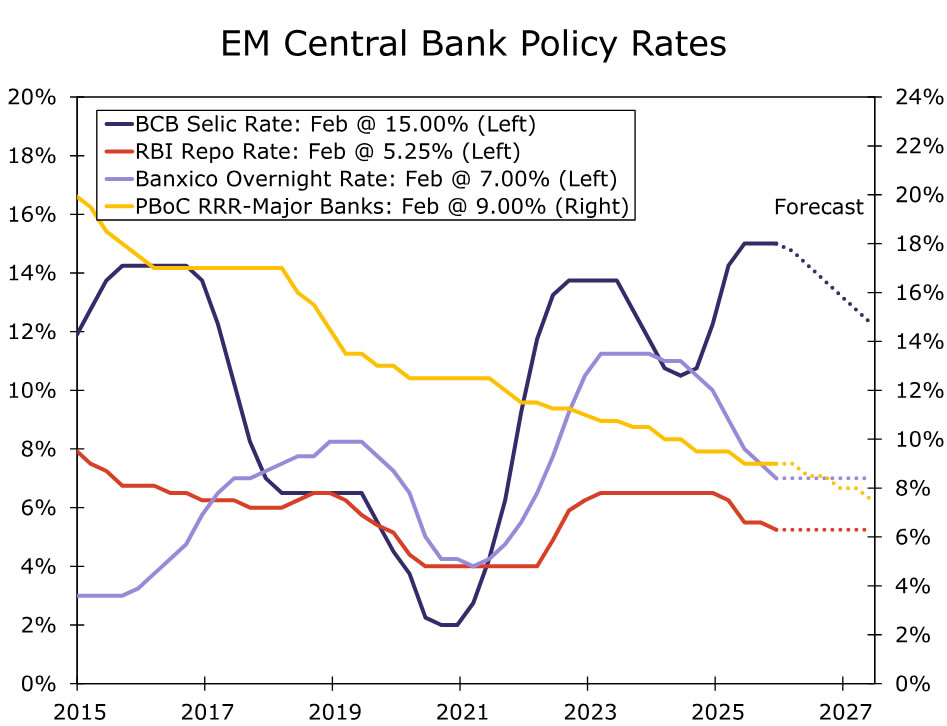

- Under our assumption that renewed military confrontation in the Middle East proves to be a temporary shock, international central banks are unlikely to adjust monetary policy paths all too materially. Similar to how we are thinking about the Fed, foreign central bank policymakers are likely to view the rise in oil and broader energy prices as a supply shock rather than a sharp upswing in demand. In that sense, pre-conflict guidance on rates is likely to remain in effect, and we are not making adjustments to our G10 (Figure 7) nor EM (Figure 8) central bank policy rate forecasts. At the same time, central banks will weigh the increase of geopolitical uncertainty on investor sentiment adding to existing downside risks to growth from trade and policy uncertainty. As such, absent a more sustained disruption from the Middle East, we see greater asymmetry of global central banks to ease policy.

- For advanced economy central banks where we forecast rate cuts prior to renewed conflict in the Middle East (e.g., Bank of Canada and Bank of England), our conviction in those calls is stronger, and we believe the balance of risk is now tilted toward more BoC and BoE easing than we currently forecast. Central banks where we felt the pre-conflict balance of risk was asymmetrically tilted toward restarting easing cycles (e.g., European Central Bank) may now have new rationale to lower rates. And in Japan, we already hold a less hawkish view on Bank of Japan rates than market pricing, a place we remain comfortable.

- Emerging market economies are more exposed to events in the Middle East and have more exposure to two-sided risks, but under the assumption of only temporary market disruptions, we do not believe EM central bank preferences for rates are set to change. Oil price shocks can be more impactful in EMs as energy tends to account for a greater share of CPI baskets relative to advanced economies. But if energy price rises are temporary, a transitory disruption to disinflation trends can also be shrugged off by EM policymakers. Also, and while not unique to EMs, local currency depreciation and the subsequent pass-through to prices is more of a risk in EMs. For now, EM currencies are under only modest pressure, which for us, is not enough to generate less dovish or more hawkish postures from major EM central banks. Even in a scenario where EM FX depreciation is more intense or longer-lasting, EM currencies have rallied over the past 12–18 months. Baked in currency strength offers central banks a degree of flexibility to maintain easing biases, or at least not rush to communicate rate hikes, going forward.

{kind=link}