Canadian Highlights

- Canada’s labour market weakness continued in February, with losses concentrated in full-time and private sector jobs. The unemployment rate rose to 6.7%.

- Canada’s trade deficit widened substantially in January, and we expect trade to subtract from Q1 GDP growth, with the recent oil price jump not yet reflected in the data.

- If elevated oil prices persist, the risk is that inflation expectations start to rise. For now, we expect the Bank of Canada to stay on hold next week, and continue to assess the impacts of the ongoing disruption.

U.S. Highlights

- The intensifying conflict in the Middle East continued to push global energy prices higher, as elevated uncertainty regarding the conflict’s duration weighed on financial markets.

- Inflation data for February, which pre-dated the uptick in energy prices, registered an annual reading of 2.4% ahead of next week’s Federal Reserve meeting.

- The U.S. announced new Section 301 tariff investigations covering dozens of countries, confirming that the administration will continue to levy tariffs in the wake of the Supreme Court ruling striking down the IEEPA tariffs.

Canada – Oil Shock Therapy

Wild swings in crude oil prices kept markets on their toes this week as the Strait of Hormuz – a choke point for roughly 20% of global oil supply – remained effectively closed. At time of writing, WTI crude is sitting above $96 per barrel, above last week’s close, but the path there has been a wild ride: prices have traded between $78 and $117 over that span. Equity markets weakened with the S&P TSX, declining 0.5%. Bond markets continued to price in higher inflation risks. The 10-year Government of Canada yield rose another 5 basis points to 3.46%, bringing the increase to more than 30 basis points since before the attacks on Iran.

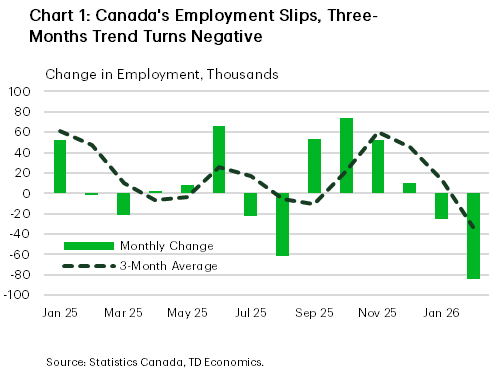

A view of Canada’s labour market immediately prior to the oil shock, came from Friday’s jobs report. Contrary to expectations for a rebound, February doubled down on January’s weakness with employment falling 84k, adding to the 25k decline the month before, moving the three-month trend back into negative territory (Chart 1). The details were also disappointing. losses were seen in full-time and private sector jobs, with Statistics Canada noting that private sector employment was virtually unchanged from a year earlier. The labour force also continued to contract, albeit at a more modest pace than in January.

Despite an exodus from the labour force, the unemployment rate rose to 6.7%. All in all, the report is decidedly weaker than markets expected, although the direction of travel was not entirely surprising given the multiple challenges facing the economy.

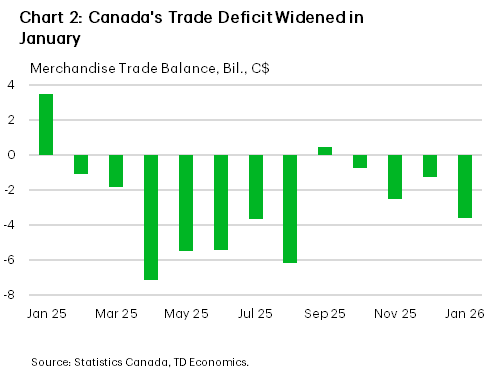

January’s merchandise trade report offered another reminder of the ongoing struggles. Canada’s trade deficit widened substantially, to $3.6 billion from $1.3 billion in December, as exports declined and erased gains from previous months (Chart 2). Much of the weakness came from the auto sector, where extended seasonal production shutdowns distorted both export and import numbers. As production schedules normalize, we expect some improvement over the next couple of months.

The recent jump in oil prices will not show up meaningfully in Canada’s trade balance until the March data. With limited information available, net trade is likely to subtract from Q1 2026 real GDP growth. If elevated oil prices persist, the risk is that cost-push inflation begins to spread beyond energy and inflation expectations start to rise. Deputy Governor Sharon Kozicki outlined how the Bank of Canada might respond to supply shocks in a speech last week. The size and persistence of the shock, coupled with the current state of the economy are the key determinants of the policy choice. It is the persistence of the oil shock that is a key uncertainty right now. As for the current state of the economy, Canada’s broader macro backdrop remains soft. With no boom in GDP on the horizon, we don’t see the conditions required for tightening this year, in contrast to the slight odds markets are currently placing on a hike. We expect the Bank of Canada to stay on hold next week, and continue to assess the impacts of the ongoing disruption in the Strait.

U.S. – Geopolitical Risks Keep Market on Edge

Financial markets faced another week of volatility as the conflict in the Middle East intensified. Iranian attacks against vessels passing through the Strait of Hormuz and energy infrastructure in the region has kept energy prices elevated, with oil prices remaining in the $90-100 per barrel range through the end of the week. The announcement that International Energy Agency member countries would release strategic oil reserves provided some relief to the tumult in financial markets, but on aggregate, the near-term risk outlook for the global economy remains elevated. As of the time of writing, the S&P 500 is down 1.2% and the U.S. 10-Year yield is up 14 basis points on the week to 4.27%.

The U.S. remains partially insulated from the spike in global energy prices as a net energy exporter, but the conflict is still expected to create a light headwind for growth this year. The duration of the conflict and its impact on energy prices remains highly uncertain, but the recovery time for energy markets is expected to be measured in months not weeks. This will likely weigh on U.S. consumers and businesses over the near-term.

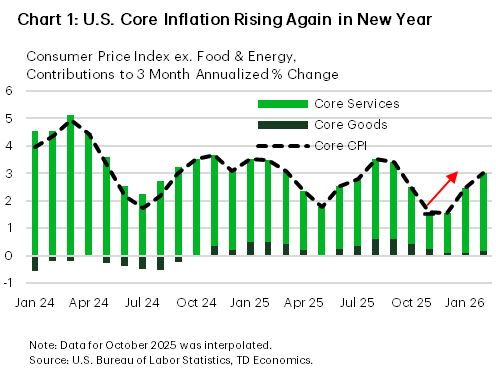

Inflation data for February, which pre-dated the rise in global energy prices, showed that inflationary pressures were still somewhat elevated to start the new year. The 3-month annualized percentage change in core CPI was back at 3% in February after briefly falling in the post-shutdown period (Chart 1). With energy prices rising sharply and tariff cost passthrough still occurring in the background, elevated inflation pressures are likely to keep the Federal Reserve cautious moving forward. As of the time of writing, financial markets have priced in a one-third chance of the Federal Reserve remaining on hold through this year.

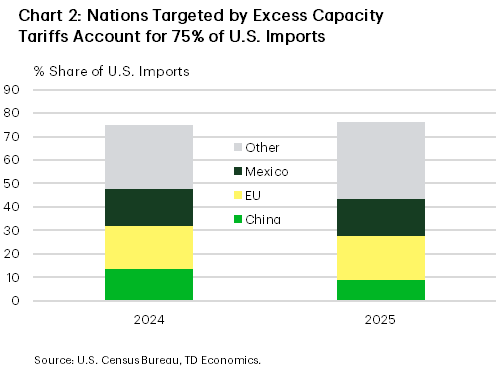

On the tariff front, U.S. Trade Representative Greer announced several new Section 301 tariff investigations covering dozens of countries this week. Section 301 tariffs are imposed against nations engaging in unfair/anti-competitive trading practices which disadvantage U.S. commerce. The first investigation announced on Wednesday relates to “structural excess capacity and production in manufacturing” which will target 15 countries and the E.U. The targeted countries account for roughly 75% of U.S. imports, with the E.U., Mexico, and China accounting for 40-50 percentage-points of that share (Chart 2). The other Section 301 tariff investigations relate to the failure of foreign nations to effectively prohibit the importation of goods produced using forced labor and targets the 60 largest U.S. trading partners. With the global 10% Section 122 tariff imposed last month set to expire at the end of July, the administration is likely to expedite these investigations to create a new tariff regime roughly equivalent to what was in place before the IEEPA tariffs were stuck down.

Looking ahead to next week, the Federal Reserve is widely expected to hold rates steady. However, investors will be keenly watching for their views on the balance of risks amid the spike in oil prices and elevated uncertainty. The labor market has weakened in recent months, but inflation pressures appear likely to keep inflation well above 2% through the year. Chairman Powell is likely to reiterate the data dependency of the FOMC and the need for patience to monitor the sustainability of emerging trends.

{kind=link}