- The Fed maintained its monetary policy unchanged in March, as widely expected by both consensus and markets.

- Powell refrained from strong forward guidance but appeared more concerned about inflation than downside risks to growth. Median ‘dots’ remained unchanged, but the distribution shifted towards later cuts.

- 2y UST yields shifted some 7bp higher, and EUR/USD declined back below 1.15. We still like our call for two more rate cuts from the Fed, but the timing remains highly sensitive to the length of the energy supply disruption.

The FOMC’s March statement was rather blunt about how the war in Iran is affecting monetary policy decisions for now, as the only new addition was: “The implications of developments in the Middle East for the U.S. economy are uncertain.” Powell joked about the policymakers having even considered skipping publishing the summary of economic projections given how sensitive the outlook remains to the assumptions made about the war in Iran.

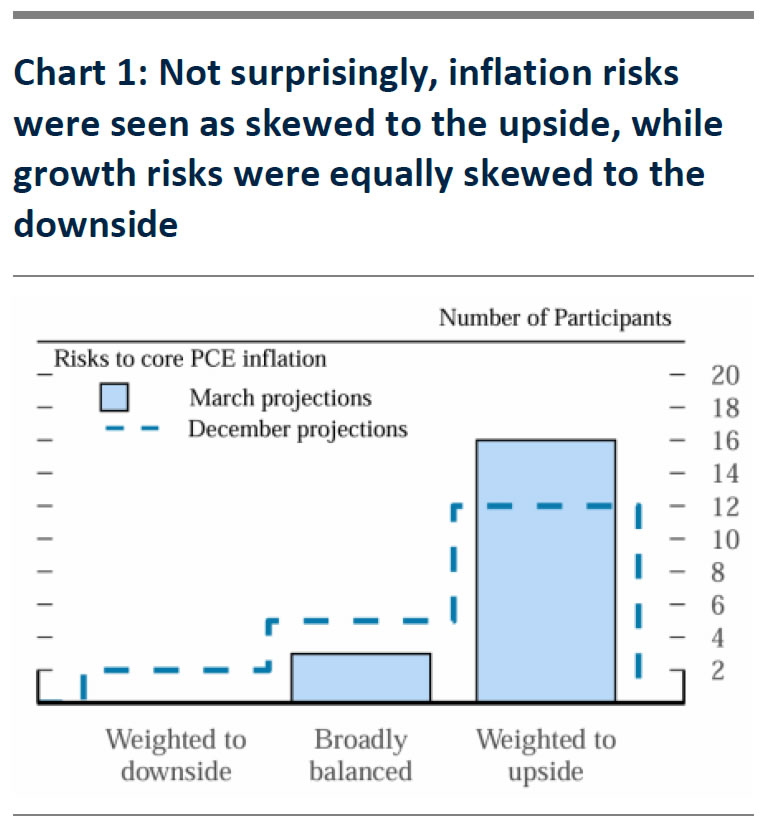

The GDP growth forecast was revised up (2.3% for 2027; Dec 2.0%) as was the median core PCE forecast (2.2% for 2027; Dec. 2.1%). Under ‘normal’ circumstances, we would have seen such revisions as hawkish signals, but markets paid little attention for now. Not surprisingly, the risk assessment showed GDP growth risks tilting back to the downside and inflation risks equally to the upside.

Powell did not appear particularly hawkish, but he also avoided some of the dovish arguments he could have presented. In our preview, we speculated that the negative growth impact from already tighter financial conditions could be an argument in favour of continuing rate cuts, but this was not even brought up.

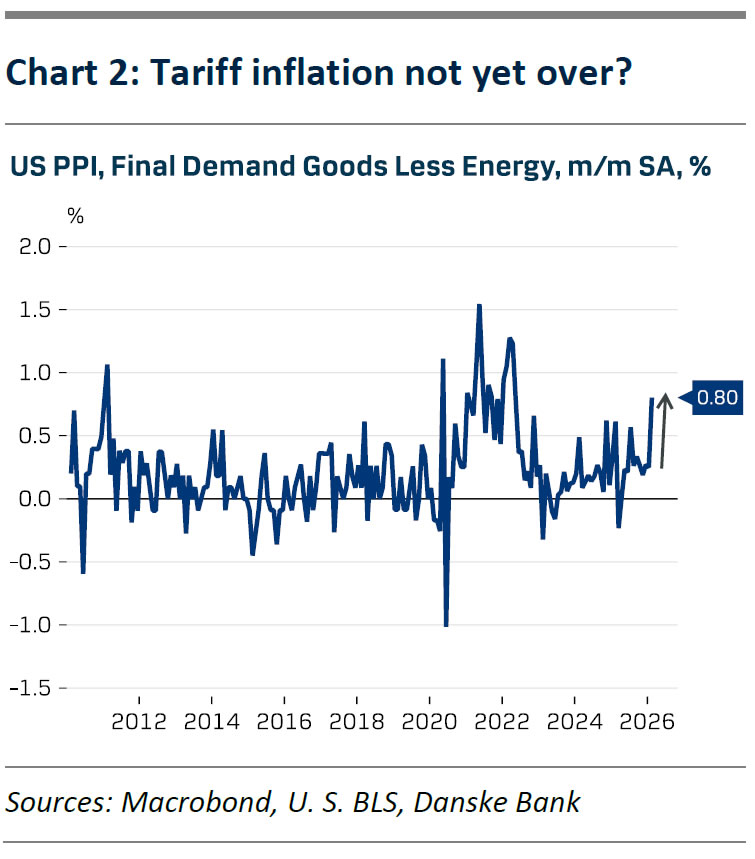

UST yields shifted modestly higher and broad USD gained during the press conference. Powell underscored that a ‘meaningful’ number of participants had shifted their rate expectations in favour of later cuts, even if the median projection still foresees two more 25bp reductions. He also emphasized the importance of tariff-driven inflation slowing over the course of this year. On that topic, note that the February PPI released earlier today showed core goods prices rising at the fastest monthly pace since April 2022 – certainly a concerning signal in this light.

Even so, we still like our call of two more rate cuts. Markets price in only 17bp worth of cuts over the next year. Our pre-war baseline forecast has been for cuts in June and September, though the timing is not a high conviction call, and we will evaluate it as we gain more clarity on the scale and length of the energy supply disruption.

Note that there was no discussion about the Fed’s balance sheet operations. We expect to see some guidance on the slowing of T-bill reserve management purchases in the meeting minutes. The base case is that the net purchase volumes will decrease substantially after the mid-April tax date.

{kind=link}