Business confidence understandably fell in March, particularly later in the month as the consequences of the Middle East conflict for New Zealand became more apparent.

Key results, March 2026

- Business confidence: 32.5 (Prev: 59.2)

- Expectations for own trading activity: 39.3 (Prev: 52.6)

- Activity vs same month one year ago: 17.5 (Prev: 23.4)

- Inflation expectations: 3.08% (Prev: 2.93%)

- Pricing intentions: 60.3 (Prev: 53.5)

It’s entirely understandable that business confidence took a sharp blow in March, with the Iran conflict kicking off at the end of February. It’s also unsurprising that the later responses were much more downbeat than the earlier ones, as the consequences for this part of the world started to come to light over the course of the month.

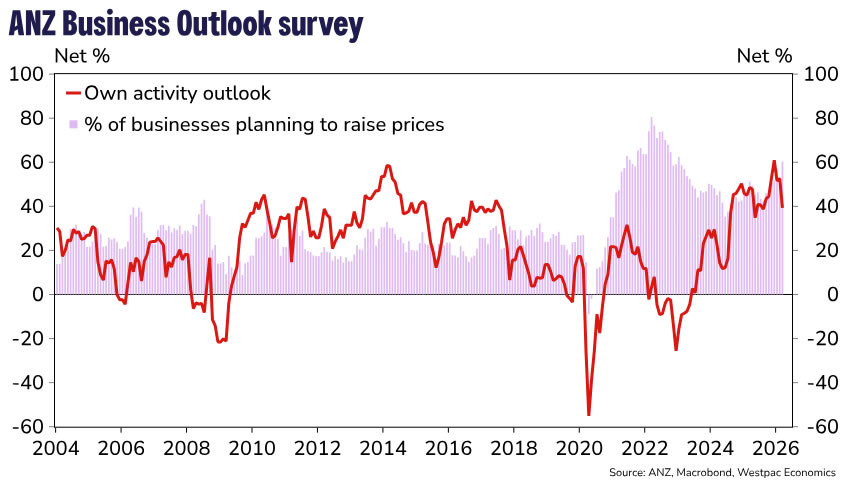

The forward-looking measures of confidence and business intentions were all down substantially in March compared to February, although they generally remained net positive. Firms’ own-activity expectations, which has typically had the closest correspondence with GDP growth, fell from 53% to 39%, the lowest level since last August (and the late-month responses were closer to the lows seen in mid-2024).

Notably, this weakness also extended to the backward-looking measures. Businesses’ activity compared to a year ago was a net 17.5% positive – but the early responses were similar to the net 23.4% in February, while the late-month responses were close to zero. There is probably a degree of sentiment going into these responses as well, but it is plausible that some businesses have seen such an immediate impact from the Iran conflict – for instance, the surge in fuel prices is likely to have weighed on consumers’ spending power elsewhere in the retail sector.

The pricing measures in the survey were unsurprisingly higher. Expected inflation for the year ahead rose to 3.08%, the highest since July 2024. A net 85% of firms expect their own costs to increase in the coming months, and a net 60% intend to raise their prices – in both cases the highest readings since early 2023.

These diverging messages on activity and inflation – typical for a supply-side shock such as a spike in oil prices – leave the Reserve Bank with a delicate balancing act. An initial surge in the inflation rate is unavoidable, but the key is whether the conditions are in place for repeating rounds of price increases.

And notably, while firms are aiming to pass on the fuel price shock into their own prices, that doesn’t extend to passing it on into bigger wage increases – both the past and expected wage growth measures in the survey fell compared to February. Above-average unemployment and limited bargaining power for workers is a crucial difference between today’s situation and the inflation surge that we saw in 2021-22.

{kind=link}