- Consistent with guidance given by Governor Breman in a recent speech, we expect the RBNZ to hold the OCR at 2.25% at the 8 April review.

- Barring major developments over coming days in the Middle East, the associated commentary – which will include a post-meeting press conference – will likely closely mirror Governor Breman’s recent speech.

- We expect the Bank to emphasise that it will not react to the first-round impact of higher energy prices on near-term inflation but that it will respond should there be evidence of second‑round effects that might create persistent inflation.

- While the post-meeting statement will present the consensus view of the MPC, the Record of Meeting will likely reflect a diversity of views about the likelihood of second-round persistent inflation and thus the appropriate policy stance.

- The Bank is not scheduled to present revised economic projections at this meeting. However, it is possible that the RBNZ will provide some guidance of the likely magnitude of the upward revision to near-term inflation and downward revision to GDP growth that might be considered in May.

- We think the Bank will aim to balance a desire to avoid a further tightening of financial conditions with the desire to not sound complacent about the medium-term inflation risks that come with an energy price shock.

The RBNZ will announce the outcome of the next Monetary Policy Review (MPR) at 2pm NZT on 8 April. In addition to the usual release of a post-meeting statement and the Record of Meeting, this meeting is notable as it will feature the first post-meeting press conference at a MPR meeting – a welcome innovation introduced as part of Governor Breman’s drive for greater transparency.

In the absence over coming days of major developments in the Middle East, we think that the Bank’s communication at this meeting is likely to closely mirror the speech given by Breman on 25 March – a speech that had received input from the Bank’s Monetary Policy Committee (MPC), albeit it not necessarily representing every member’s view. And so, with the Bank already indicating that it will not respond in a knee-jerk manner to a near-term oil-driven lift in inflation, the OCR is almost certain to be held at 2.25% next week, as would have been the case in the absence of the oil shock.

The RBNZ’s guidance about what to expect at future meetings will also likely echo the Governor speech. In crafting this guidance, the MPC will aim to reassure markets that it will not overreact to the shock, which could cause markets to further tighten financial conditions. At the same time, the RBNZ will need to ensure it sounds credible to households and businesses about its willingness to tighten policy if inflation expectations and pricing behaviour evolve in a manner inconsistent with achieving the inflation target over the medium-term. While monetary policy should look through a temporary spike in energy prices, the MPC will need to be vigilant – and be seen to be vigilant – against the risk that inflation becomes persistent.

The magnitude of that risk will depend in part on the duration of the conflict, with a more protracted conflict likely to lead to greater damage to energy infrastructure and enduring damage to supply chains, prolonging the inflation shock. It will also depend on the state of the domestic economy. As the Governor noted in her speech, while the recovery may be broadening, it is still early – as demonstrated by the disappointing Q4 GDP outcome – and the economy is operating well below capacity. In this context, many businesses may struggle to fully pass on cost increases without losing demand – a dynamic that should delay or limit second‑round inflation effects stemming from the rise in oil prices.

While the post-meeting statement and the Governor’s press conference will largely represent the consensus view of the Committee, the Record of Meeting will likely reveal a diversity of views. Key areas where the views of the Committee could diverge include the likely duration of the conflict, the impact on the economy, the likelihood of second-round effects driving persistent inflation over the medium-term, and the appropriate course for monetary policy over time. Such discussions might provide some insight into how the consensus view of the MPC might evolve as more is learnt about the evolution of the conflict and its economic impact.

The RBNZ is unlikely to provide a full update of its economic projections next week – that will likely come as usual when it releases the next Monetary Policy Statement (MPS) in May. That update will include reaction to pre-conflict data, such as the slightly disappointing Q4 GDP report. It will also allow reflect reaction to the first reports showing how the global and domestic economies have responded to the oil shock (so far there has been some evidence of softer PMI readings offshore, together with a marked drop in consumer confidence in New Zealand). Developments in financial conditions, including the exchange rate, will also factor into those revisions.

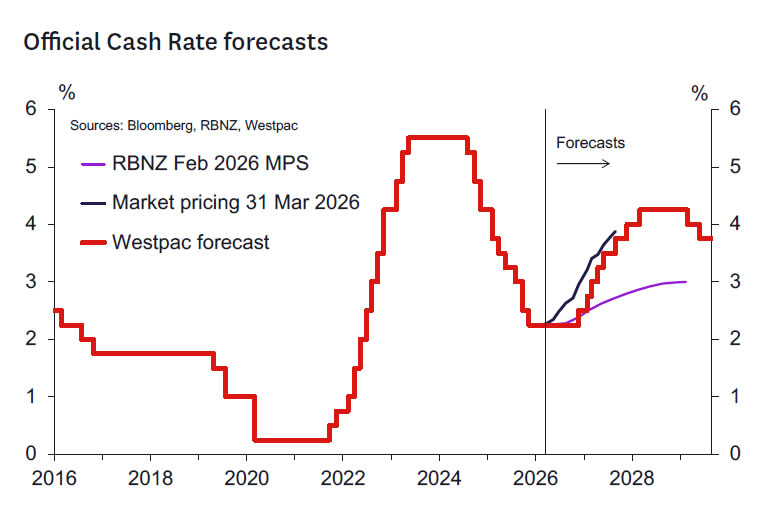

But we don’t rule out the possibility that next week the RBNZ could provide some preliminary quantification of how the conflict has impacted the near-term outlook for inflation and GDP growth that was presented in the February MPS (such as where inflation may peak and how much growth might be impacted this year). Such estimates could be refined in May based on developments in the Middle East and with the benefit of early economic data and further anecdotes quantifying the impact on New Zealand consumer and business behaviour. In our own recent forecast update, we upgraded our outlook for CPI inflation (now expected to peak at 4.1%y/y this year) and downgraded our forecasts for economic growth (now expected to be 1.9%y/y this year, down from a pre-war forecast of 3.3%y/y).

In its communications on 8 April, the RBNZ will balance a desire to avoid a further tightening of financial conditions with the desire to not sound complacent about the medium-term inflation risks that come with an energy price shock. Reinforcement of the approach communicated in Breman’s speech guidance should continue to lean against the market’s current pricing of more than three 25bp OCR hikes by the end of this year, especially once current liquidity issues in the domestic market ease. As we discussed in our own forecast update, we continue to forecast just one 25bp hike this year, but also that significant tightening will occur in 2027 once the activity implications of the energy shock begin to dissipate.

Kelly’s take.

No change is very appropriate for now. This supply shock is extremely unwelcome and will likely significantly boost headline inflation for a while. But at least for now the large, accumulated level of excess capacity likely means the risk of entrenched inflation remains modest.

The MPC has time to assess how the outlook will evolve. We don’t know how far and for how long inflation will remain elevated. Forecasts are necessarily uncertain if only because the duration of the war and restriction of oil supplies remain uncertain.

We can’t assume inflation will automatically revert to more normal levels, but we also can’t assume it won’t. We should be alert to the possibility of financial stability issues globally that could see financial conditions tighten. That’s another reason for not putting maximum weight on forecasts that suggest risks of inflation remaining elevated for a long time. The market might do some of the job for us. And there might be bigger fish to fry.

If inflation rises for a protracted period, then it won’t be appropriate to have interest rates in the 2’s or even the low 3’s as real interest rates will be too low. But there’s time to assess and plenty of scope to move quickly once it’s determined that real interest rates closer to more neutral settings are appropriate. I’d want to see a lot more data before coming to that judgement.

at 2pm NZT on 8 April. In addition to the usual release of a post-meeting statement and the Record of Meeting, this meeting is notable as it will feature the first post-meeting press conference at a MPR meeting – a welcome innovation introduced as part of Governor Breman’s drive for greater transparency.){kind=link}