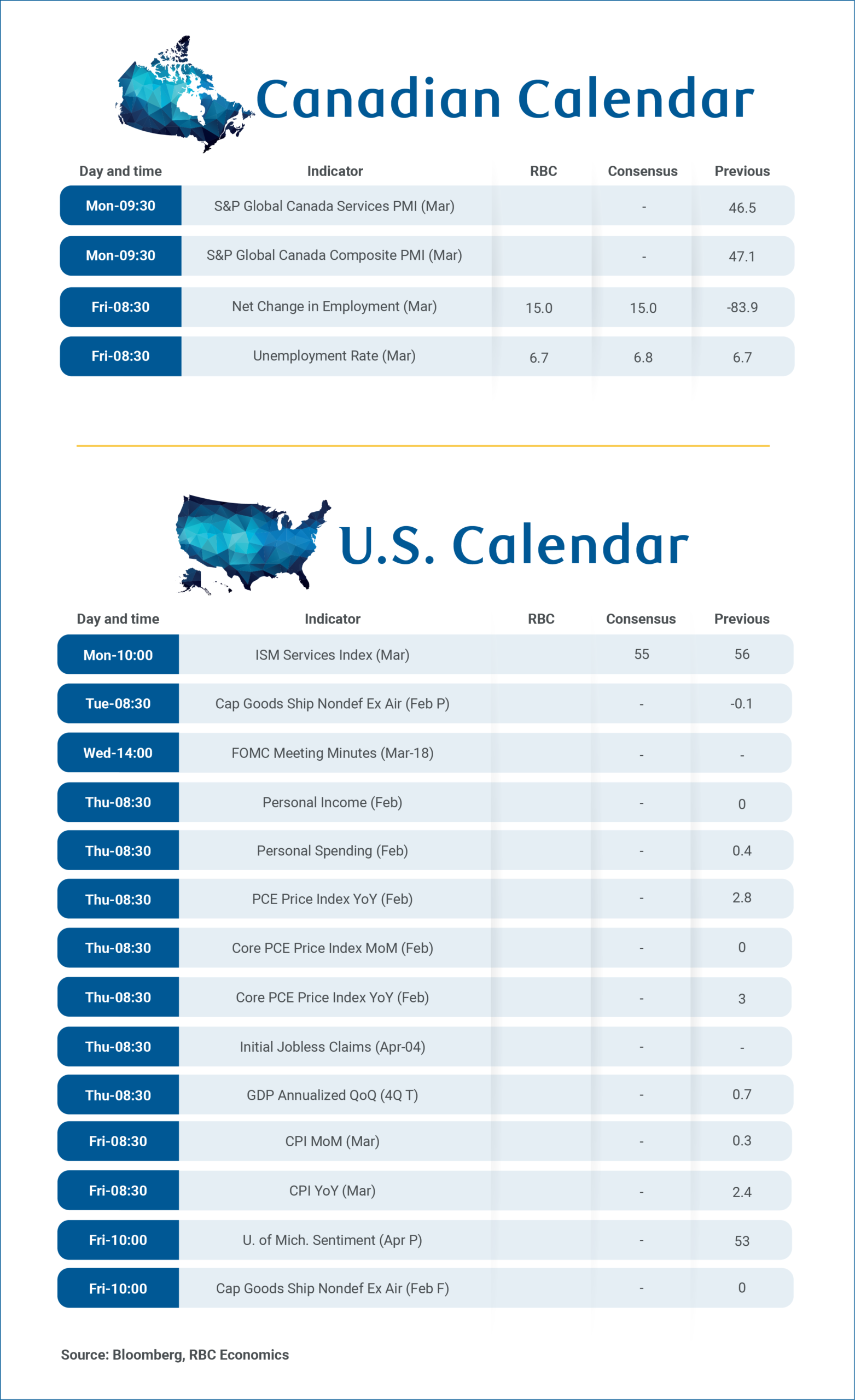

Next Friday’s Canadian Labour Force Survey should show a partial recovery in employment in March after consecutive job losses totalling 109,000 over the prior two months.

The monthly employment data is notoriously volatile, and despite the earlier losses, the unemployment rate still ticked slightly lower over the last two months. It partially retraced a 0.3 percentage point decline in January with a 0.2 percentage point increase to 6.7% in February, still below the 6.8% average in Q4, and recent peak of 7.1% in September.

Young workers aged 15 to 24 accounted for an outsized share of the earlier job losses, representing 60% of the total despite taking up only 14% of the overall labour force. As a result, their unemployment rate increased substantially by 0.7 percentage points in February compared to the Q4 average.

By contrast, the unemployment rate among prime-age workers (aged 25 to 54) has remained relatively steady, trending lower to 5.7% in February from 5.8% in Q4 2025.

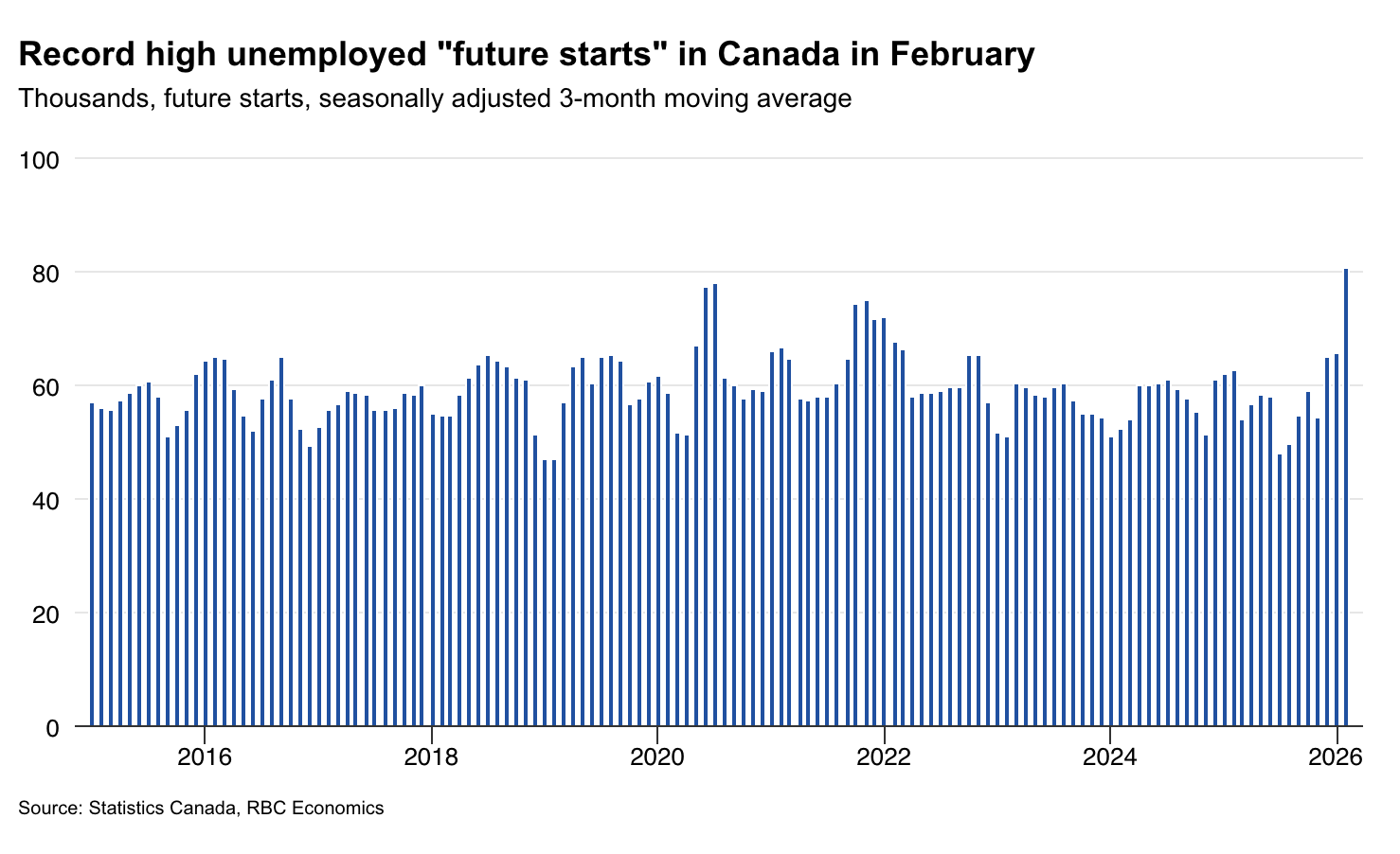

Notably, much of the latest increase in the unemployment rate (about half by our count) in February came from a rise in workers that were unemployed, but had a job lined up to start within the next four weeks (future starts). As some of these positions pass start dates, we expect a modest recovery of 15,000 jobs in March—enough to keep the unemployment rate steady at 6.7%.

The increase in future starts coincided with rising job postings in the second half of 2025 into the new year. However, recent data from Indeed.com flagged a sharp reversal in March, possibly due to rising economic uncertainty tied to escalating global geopolitical tensions dampening hiring demand. A similar plunge in job postings was seen in the United States and Australia.

Outlook for hiring remains stable amid uncertainty

Weak hiring sentiment in Canada could extend well into Q2 as geopolitical uncertainty, and ongoing tariff risks persist. However, recent gross domestic product growth numbers have looked better with Statistics Canada’s preliminary estimates pointing to 1 ½ % annualized growth in Q1 after a soft start, supported by resilient domestic demand.

Uncertainty remains elevated, but we retain our outlook that the per-worker labour market should continue to recover this year. Job growth will remain softer than historical norms given rapidly slowing population growth. However, the unemployment rate is tracking well against our prior assumption of 6.6% in Q1, and we expect it to move lower toward 6.3% by year-end.

Next Friday’s March U.S. Consumer Price Index will show a surge in headline inflation after the Middle East conflict pushed oil prices sharply higher. Core CPI, excluding food and energy, is expected to remain largely unchanged from February, driven again by pressure among core services as domestic demand remains strong. Core goods CPI will be closely watched for any tariff passthrough.

U.S. personal spending likely ticked higher in February after retail sales posted a 0.6% monthly increase following a 0.1% decline in January. The gain was driven largely by a 6% month-over-month surge in auto sales. Personal income likely continued its upward trend, as average hourly wages rose 0.3% while hours worked remained flat relative to January.

{kind=link}