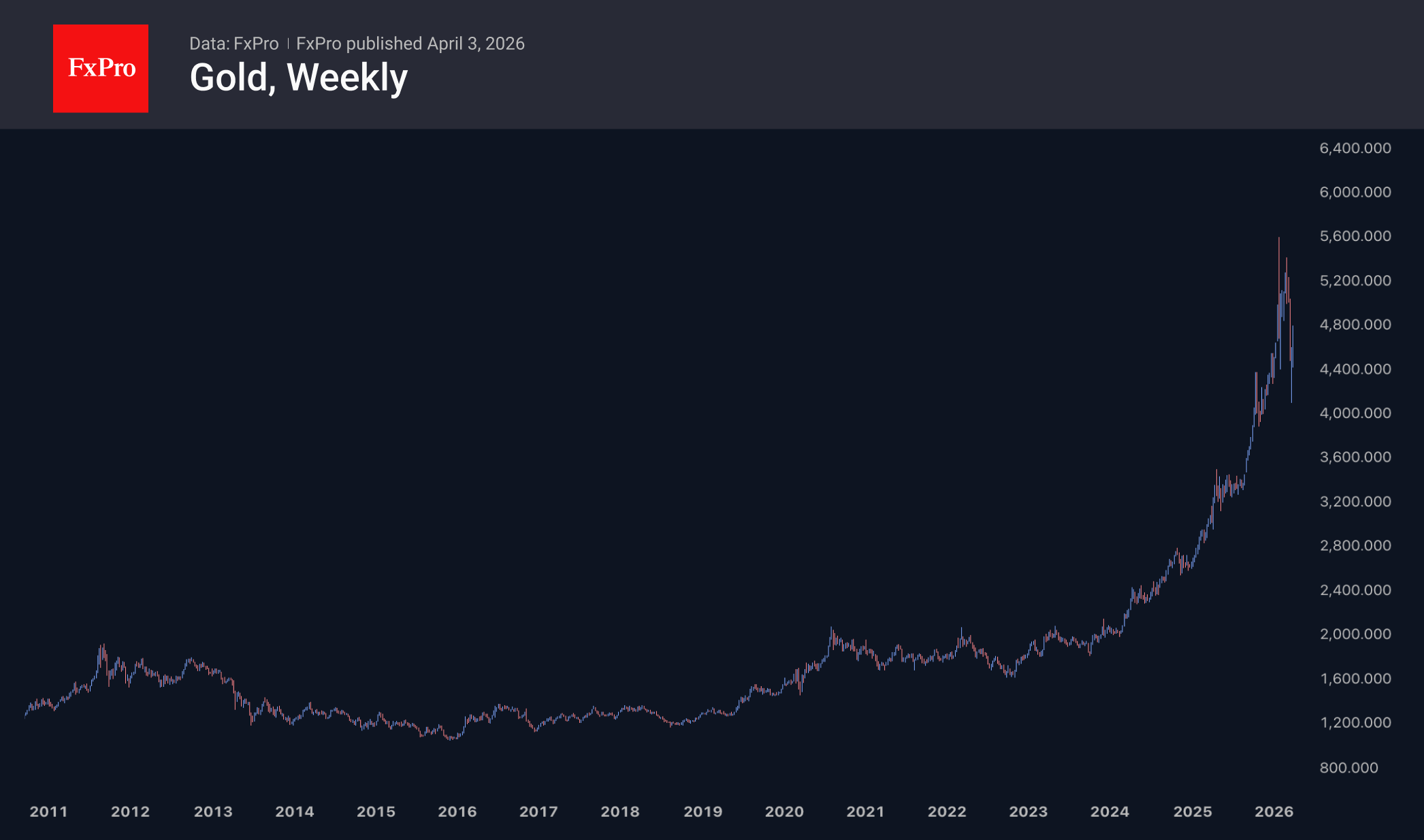

The Middle East conflict is weighing on gold prices amid expectations that central banks will raise interest rates to address rising inflation driven by oil prices. This seems like a knee-jerk reaction, as this is precisely how central banks acted in 2022. Moreover, it is widely acknowledged that this was a belated response. Another factor working against gold is the reduction in gold purchases, as well as the sale of gold from reserves to support national currencies, as India and Turkey have been doing recently. It is possible that many others are doing the same, but we are not yet aware.

This is a rather short-sighted approach, as current fuel prices are a shock to consumers, and this will be followed by a shock to the economy, requiring monetary policy to be eased, not tightened. However, we first need to hear that central banks share this view; for now, they remain focused on inflation.

Among the medium-term price targets, $4,200 remains significant. A fall in the price of gold to this level would still be within the uptrend. A break below this level would signal a reversal of the three-year uptrend. A rebound from this level would keep alive the hope that the bullish trend in gold is not yet over.

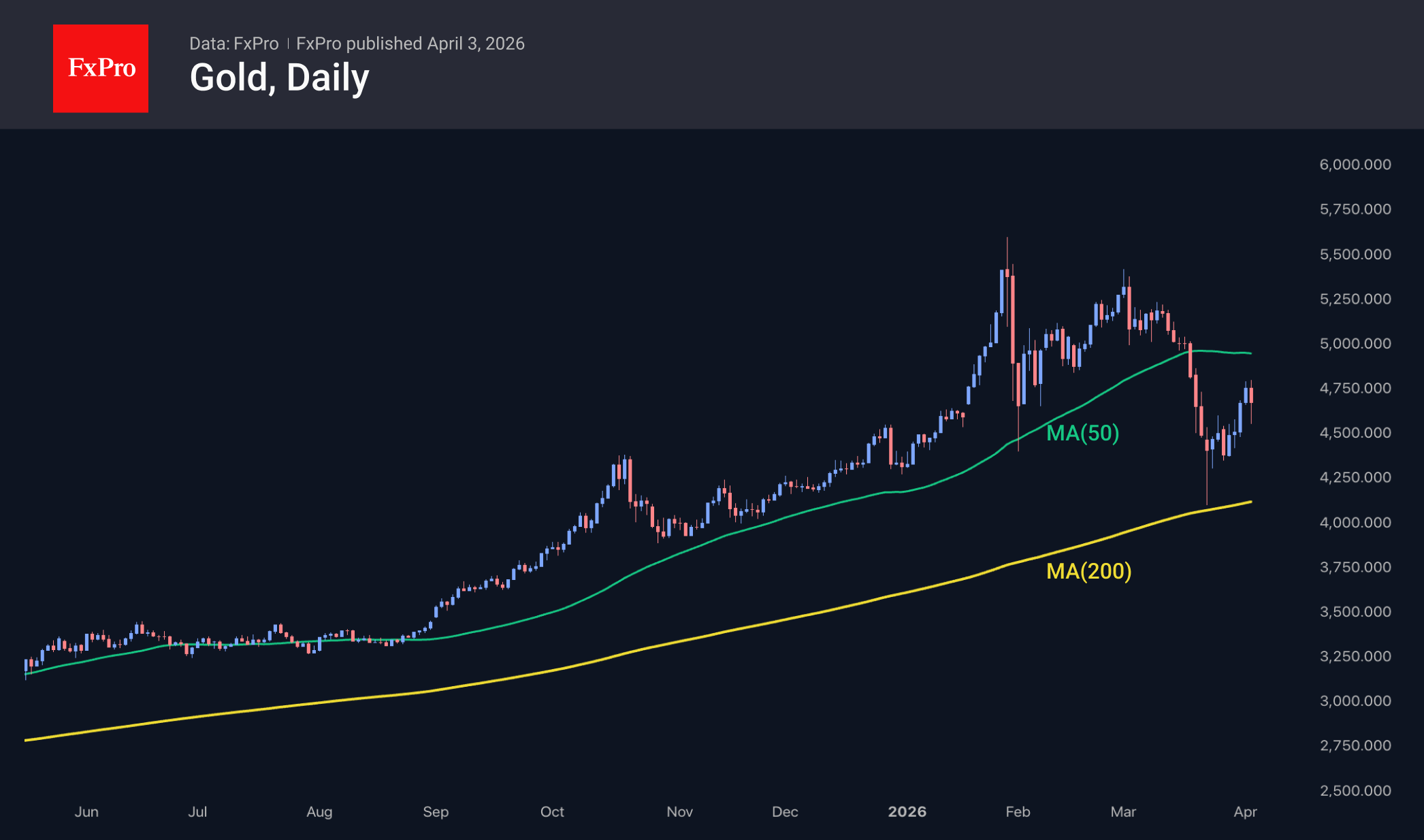

From a technical analysis perspective, last week, gold may have found support at the 200-day MA during its decline to $4,100. Strong buying continued right up until Thursday morning, when the price touched $4,800. The subsequent dip following Trump’s hawkish rhetoric did not trigger a fresh wave of selling in gold, keeping hopes alive for a return to the bullish trend.

It is quite possible that gold will test the 50-day MA near $5,000 once again next week, finally shaking off oversold conditions. This suggests a positive outlook for next week, but we remain cautiously pessimistic over the longer term, anticipating a decline to $4,200 in the medium term and a low of $3,300 for the bearish cycle we are already in.

{kind=link}