Here are the latest developments in global markets:

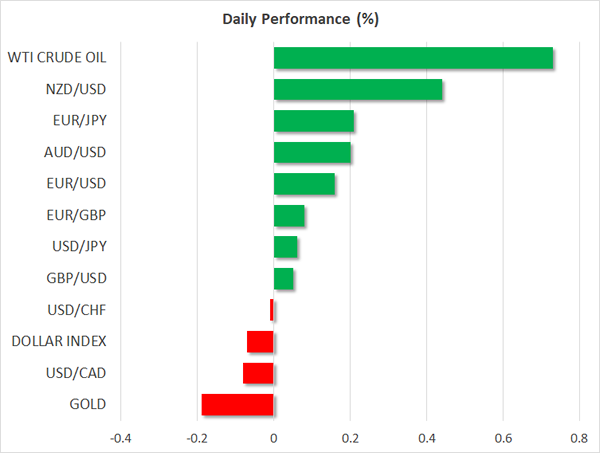

FOREX: The US dollar traded 0.1% lower against a basket of major currencies during the Asian trading session Thursday, after posting gains on Wednesday.

STOCKS: All three major US equity indices (Dow Jones, S&P 500, Nasdaq Composite) closed at fresh record highs yesterday, buoyed by optimism around the US economy following strong data releases and a cheerful tone in the FOMC minutes. Futures tracking the Dow, S&P and Nasdaq 100 are currently in the green as well. In Asia, Hong Kong’s Hang Seng was up 0.5%, while Japan’s Nikkei 225 and Topix indices finished higher by 3.2% and 2.6% respectively, both closing at multi-decade high levels.

COMMODITIES: Gold fell, trading 0.2% lower as the Asian session was coming to a halt, after trading lower yesterday as well. Meanwhile, WTI and Brent crude oil were up 0.7% and 0.5% respectively, as the continued political instability in Iran lead to concerns that the nation’s oil production may be disrupted in the future.

Major movers: Dollar recovers as FOMC minutes reaffirm steady path; gold declines

The US dollar regained some of its lost glamour on Wednesday, after the ISM manufacturing PMI for December surprisingly rose, beating expectations that projected it to tick down, and indicating that the sector finished 2017 on a very strong footing. The greenback recovered further a few hours later, after the FOMC minutes from the December meeting reaffirmed the central bank remains committed to continue its normalization cycle in 2018, even despite below-target inflation.

The only worried remarks came from a “couple of participants”, which were probably Neel Kashkari and Charles Evans, both of which dissented from the decision to raise rates. The absence of any other signals suggesting that we could see a pause in rate hikes next year if inflation continues to undershoot likely came as a relief to dollar bulls. Gold traded lower after the minutes, possibly due to the gains in the US currency, as gold is denominated in dollars.

However, the dollar did not hold on to its gains, trading slightly lower during the Asian session Thursday. Euro/dollar was up nearly 0.2%, while sterling/dollar was marginally higher as well. The commodity-linked currencies outperformed the greenback once again with kiwi/dollar leading the charge, trading 0.4% higher. Meanwhile, aussie/dollar was up 0.2%.

Day ahead: ADP jobs data out of the US and UK services PMI on the agenda

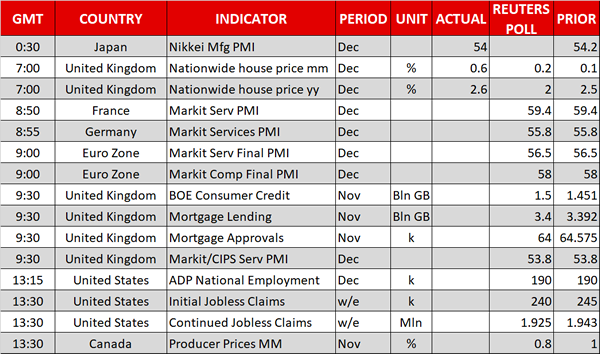

The eurozone will see the release of the readings on December services PMI as well as composite PMI – the measure that blends the manufacturing & services sectors – at 0900 GMT. However, the data will pertain to the final release and are unlikely to spur much positioning by markets. A little before that, Germany and France, the eurozone’s two largest economies, will see the release of their respective readings.

Earlier in the week, the UK was on the receiving end of weaker than expected manufacturing and construction PMIs. The December reading for the all-important for the UK economy services sector is due today at 0930 GMT. Further disappointment is anticipated to push sterling lower. Data on UK consumer credit and mortgage lending/approvals are scheduled for release at the same time.

In the US and having the capacity to spur dollar positioning is the December ADP report on positions added to the economy by the private sector. The release is viewed by some analysts as a preview to the much-awaited nonfarm payrolls report which includes data on both the private and public sector and is due on Friday. The ADP national employment report will go public at 1315 GMT and is projecting the addition of 190k private positions to the economy, the same number as in November. A little after (at 1330 GMT) weekly data on US initial and continued jobless claims will be released.

Data on Canadian producer prices for the month of November are due at 1330 GMT.

St. Louis Fed President James Bullard (a non-voting FOMC member) is scheduled to give a presentation on the US economy and monetary policy at 1830 GMT.

The EIA weekly report, that includes information on US crude oil and gasoline inventories, will be made public at 1600 GMT. Crude stockpiles are expected to decline by around 5.1 million barrels in the week that preceded. The report tends to cause volatility in oil prices.

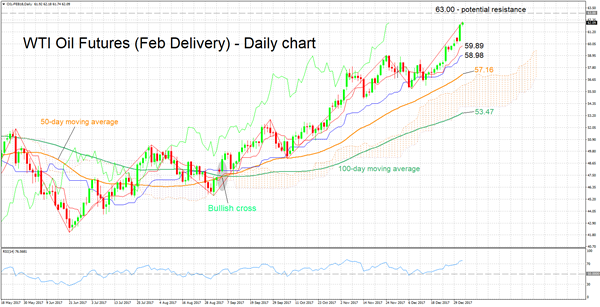

Technical Analysis: WTI oil futures hit fresh 2½-year high; bullish in short-term though RSI overbought

WTI oil futures for February delivery recorded a fresh 2½-year high of 62.18 during today’s trading.

The Tenkan-sen line being above the Kijun-sen line is a positive alignment pointing to bullish momentum in the short-term. The RSI is supporting this view as it continues rising, though notice that it has crossed into overbought territory above 70.

A bigger-than-anticipated drawdown in crude stockpiles out of today’s EIA report could lend further support to prices. In such an event, the area around the 63.00 handle could act as a barrier to the upside. This is a potential psychological level that has also served as a peak back in mid-2015 (as well as an area of congestion).

On the contrary, a smaller-than-projected drawdown could weaken prices. In this case, the range around the Kijun-sen at 59.89 might provide support. The area around this level encapsulates a peak from the recent past, as well as the 60.00 mark, another potential psychological level.