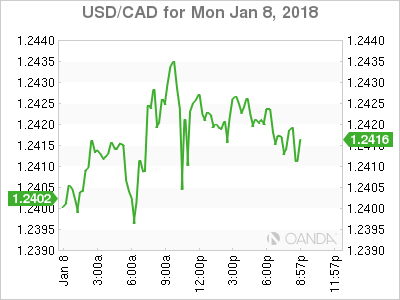

The Canadian dollar was slightly lower agains the US dollar at the start of the week. The loonie is up 1.17 percent versus the greenback so far in 2018. The American currency has not had the best of starts this year. The tax reform and December interest rate hike by the Fed had already been priced in and investors are looking ahead to a highly political year for the USD. Canadian employment was a huge surprise to the upside with another massive job gain. The number of jobs added to the economy in December was 78,600 much higher than the forecasted 1,000. The monster gain has prompted Canadian financial institutions to update their forecasts for the January policy meeting of the BoC with the majority expecting a rate hike. The loonie continued rising after the slow start to the year of the US and the boost from higher oil prices.

The fate of NAFTA remains a possible threat to the CAD, but today’s release of the Bank of Canada (BoC) Business survey shows that companies are not suffering extra anxiety in their outlook. The BoC hiked twice in 2017 before a slowdown in the economy forced the central bank to adopt a more neutral tone. Governor Poloz ended the year with a speech focusing on the topics that kept him up at night but the solid December jobs report and the BoC Survey have all but convinced the market that a rate hike will be announced on the January 17 central bank meeting. Societe Generale is forecasting a price level of 1.2050 or lower if the Bank of Canada (BoC) goes ahead with life of the interest rate to 1.25 percent next week.

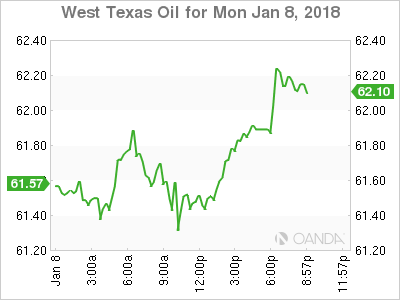

Oil is still near 2015 highs but as supply disruptions or geopolitical risks remain investors are looking at higher production from US producers starting to ramp up. The Organization of the Petroleum Exporting Countries (OPEC) deal to cut production enlisted major producers, but those not included could be the biggest winners if prices remain in current levels.

The USD/CAD rose 0.09 percent on Monday. The currency pair is trading at 1.2422 as the USD seeks to regain traction after a disappointing U.S. non farm payrolls (NFP) report on Friday, January 5 and a monster number of jobs gain in Canada on the same day. The near 80,000 added jobs convinced major institutions to change their forecast for the January 17 central bank meeting. A 25 basis points has been forecasted by most major banks with Royal Bank of Canada being one of the outliers who does expect higher rates, but later in the year. The BoC is expected to lift rates 2 or 3 times this year, the same as the U.S. Federal Reserve. The Canadian central bank has been aware of the high level of household debt but improving economic indicators could hasten the monetary policy decision.

West Texas Intermediate is trading at 61.87. The price of crude remains high as political tension in Iran and the North Sea pipeline maintenance work continues. Drilling has not been particularly strong in the US but that is expected to change soon as weather improves and shale operations could ramp up at a higher rate explaining the lack of new oil rigs.

Geopolitical risk in the oil market has been high as various members of the Organization of the Petroleum Exporting Countries (OPEC) are facing political headwinds. The big three: Saudi Arabia, Iraq and Iran have all experienced different forms of uncertainty as leadership has either changed or had to respond to different challenges. The relationship between them has also been frayed which could put into question how effective the OPEC’s production cut agreement will remain in place, or even the organization if there is a major disagreement between its biggest producers.

Market events to watch this week:

Wednesday, January 10

4:30am GBP Manufacturing Production m/m

10:30am USD Crude Oil Inventories

7:30pm AUD Retail Sales m/m

Thursday, January 11

8:30am USD PPI m/m

8:30am USD Unemployment Claims

Friday, January 12

8:30am USD CPI m/m

8:30am USD Core CPI m/m

8:30am USD Core Retail Sales m/m

8:30am USD Retail Sales m/m