Central banks and growth indicators to feature alongside Washington Turmoil

The USD dollar remains weak versus most majors due to the downward pressure from the threat of a government shutdown. The House of representatives have passed a short term funding bill, but it faces an uphill battle in the Senate with the midnight deadline fast approaching.

- Bank of Japan expected to add clarity to bond purchases

- European Central Bank (ECB) unlikely to send end of QE signals

- US first GDP estimate for Q4 forecasted at 2.9 percent

US Government Shutdown Dragging Dollar Lower

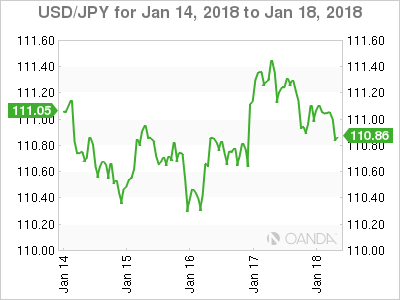

The USD/JPY dropped 0.35 percent during the last five days. The currency pair is trading at 110.68 as the weakness in the US dollar has combined with strong economic indicators in Japan. The Bank of Japan (BOJ) is optimistic about the economy and the 2 percent inflation target is looking like less of an impossible dream. The BOJ will release its monetary rate statement on Monday, January 22 at midnight EST to be followed by a press conference with BOJ Governor Haruhiko Kuroda on Tuesday, January 23 at 1:30 am EST. Economists see little chance of a change in monetary policy announced at the January meeting, with odds rising slightly starting in the fall.

The BOJ could add some details on why it cut some of the long-dated bonds purchases last week and if not is sure to be part of press conference. G10 central banks are putting pressure on the Fed as the gap between easing and tightening is smaller. The US dollar enjoyed some support from the Fed reducing stimulus and eventually hiking rates, but now with political instability and the Bank of Canada (BoC), the European Central Bank (ECB) and even the BOJ moving closer to reducing stimulus the greenback is struggling.

The EUR/USD gained 0.27 percent in the last five trading days. The single currency is trading at 1.2236 ahead of the midnight deadline for the shutdown of the US government. The EUR has been gaining against the USD on the back of improved economic indicators in Europe. Rising inflation could help the European Central Bank (ECB) set an end to their massive quantitative easing program. The ECB has said that inflation is still too weak, with stimulus to continue for the time being, but stronger growth has the market increasing the odds of the end of European QE sooner rather than later.

The USD has failed to gain traction in 2018 and politics is very much a part of what is wrong with the greenback this year. US congress is having trouble finding a way got avoid a government shutdown with the clock ticking down and President Trump complicating matters. The primaries in the fall are not looking good for the Republican party, but they are finding it challenging to break away from the President and that could cost them control of the House and the Senate.

The US Bureau of Economic Analysis (BEA) will release the first estimate of the gross domestic product (GDP) for the fourth quarter of 2017. US growth has been strong and with the highly anticipated tax reform finally a reality it is expected to continue trending upwards. There are three releases for the GDP figures as more data refines the final indicator. The first release is the most impactful given its only 30 days after the end of the quarter. The 4Q GDP will be released on Friday, January 26 at 8:30 am EST. Forecasts are calling for a gain of of 2.9 percent. A reading above that first estimate could bring some relief for the USD based on the strength of US fundamentals and the expectations of strong growth in 2018. A lower than expected GDP indicator could put even more pressure on the US currency at a time when the Trump Administration is dealing with multiple fronts.

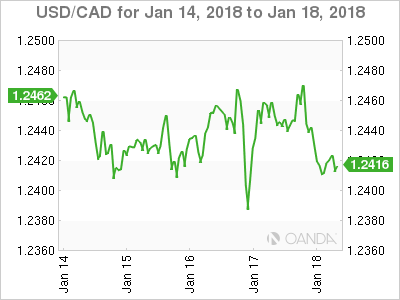

The USD/CAD rose 0.20 percent this week. The currency pair is trading at 1.2481 despite the Bank of Canada (BoC) rising rates 25 basis points. The monetary policy decision did not have the usual impact as the loonie remain subdued due to political risks. The growing risk the US pull out of the trade agreement has been already been voiced by anonymous Canadian officials and has put the loonie under pressure versus the US dollar. The three members of NAFTA originally wanted to avoid going into 2018 without the details of the deal hammered down. Mexican presidential elections in July and the US primaries in November could interfere with the already divisive topic and could politicize even further forcing it decision based on populism and not economics.

The sixth round of negotiations will kick off in Montreal on January 23 and will go until the 28. This round is of particular note given that the Foreign ministers will rejoin the talks after skipping the November and December talks.

The Bank of Canada (BoC) has now hiked three times since the summer of 2017. After two rate cuts in 2015 Governor Poloz had been cautious to remove the stimulus, but that suddenly changed in July in which various members of the monetary policy team dropped heavy hints that a hike was coming. The BoC followed that with a small surprise by hiking one month ahead of the expected date in September. The tone of the CB changed to one more neutral with no rate moves expected until the end of the first quarter.

The November and December job reports in Canada changed all that. Both had gains of 70,000 jobs and brought the unemployment rate to a 40 year low. Governor Poloz had a tough task, keep removing stimulus but at the same time warn about potential headwinds. His strategy was to focus on the actions of the Trump Administration. The tax cuts approved in December in the US could end up reducing investment in Canada, just as the negative impact of the end of NAFTA could derail the Canadian growth story.

Market events to watch this week:

Monday, January 22

- Midnight JPY Monetary Policy Statement

- Midnight JPY BOJ Outlook Report

Tuesday, January 23

- 1:30 am JPY BOJ Press Conference

Wednesday, January 24

- 4:30 am GBP Average Earnings Index 3m/y

- 10:30am USD Crude Oil Inventories

- 4:45 pm NZD CPI q/q

Thursday, January 25

- 7:45am EUR Minimum Bid Rate

- 8:30 am CAD Core Retail Sales m/m

- 8:30 am EUR ECB Press Conference

Friday, January 26

- 4:30 am GBP Prelim GDP q/q

- 8:30 am CAD CPI m/m

- 8:30 am USD Advance GDP q/q

- 8:30 am USD Core Durable Goods Orders m/m

*All times EST

is optimistic about the economy and the 2 percent inflation target is looking like less of an impossible dream. ){kind=link}