Disappointing US GDP and contradictory comments on currency strength at Davos burden dollar

The USD depreciated against majors as soft Q4 GDP numbers on Friday and mixed comments on the desired strength and weakness of the currency made at the World Economic Forum in Davos put downward pressure on the greenback. The Trump administration is pushing its tough stance on trade, but tried to soften the tone in an effort to be more inclusive. Economic fundamentals and monetary policy have been supportive of the currency, but political lack of stability has hurt the buck. Next week the market will focus on the U.S. Federal Reserve and the U.S. non farm payrolls (NFP).

- US President Trump to deliver his first State of the Union Address

- Fed anticipated to keep rates on hold at 1.25-1.50 percent

- US forecasted to have added 184,000 jobs in January

Dollar Confused Ahead of US Jobs Report and Fed Statement

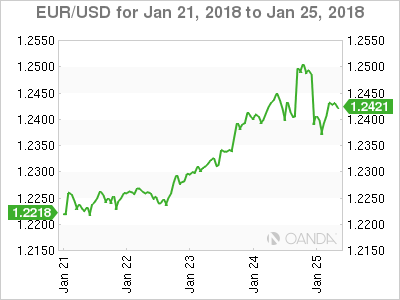

The EUR/USD gained 1.73 percent in the last five days. The single currency is trading at 1.2426 after contradictory statements from the Trump administration confused markets. Secretary of the Treasury Steve Mnuchin said on Wednesday that the weaker dollar was good for the US in relation to trade. The USD retreated and the EUR touched three year highs. Next day President Trump said the he ultimately wants to see a strong dollar as the currency is a reflection of the strength of the economy. The USD recovered some ground versus the EUR, but the damage had already been done and the EUR advanced 0.27 percent on Friday.

The first estimate for US GDP for the fourth quarter was released and it was short of expectations at 2.6 percent. The forecast the market was looking for was 3.0 percent, but given its the advanced estimate there will be two more released that could see the final GDP figure higher in the following months.

The EUR has been rising despite the words from European Central Bank (ECB) President Mario Draghi. The central bank kept its rate and massive quantitive easing program untouched. Draghi made sure to mention that stimulus would remain for as long as needed, but had to concede there were few chances it will change interest rates. The ECB President made a comment warning about using verbal intervention to talk down a currency when asked about the Davos statement from Mnuchin.

US President Trump will deliver its first Sate of the Union address on Tuesday, January 30, at 9:00 pm EST. Failing to avoid a government shutdown Trump will focus on the positives during his first year. His achievements in passing legislation came late in 2017 but he is sure to mention the tax reform bill. The stock market record breaking pace and overall strength of the economy while inherited will also be mentioned with the infrastructure plan something to look for in the immediate future. The USD got a Trump bump in late 2016 when just after winning the elections

The U.S. non farm payrolls (NFP) will be published on Friday, February 2 at 8:30 am EST. Economists are expecting the US to add 184,000 positions in January. Last month’s report came in lower than expected but the saving grace for the USD was that hourly wages grew 0.3 percent as expected. There are similar gains forecasted for January wages with a special emphasis on inflationary data as the Fed ponders what to do with stagnant wages despite a strong job component.

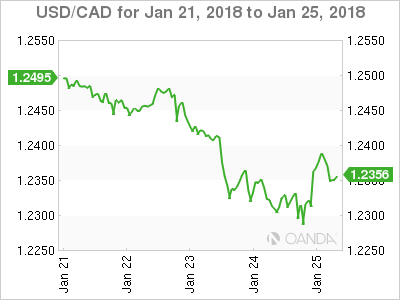

The USD/CAD lost 1.38 percent during the week. The currency pair is trading at 1.2323 with a weaker greenback sliding against a stronger loonie. The Bank of Canada (BoC) lifted its benchmark rate 25 basis points earlier in the month and Friday’s release of Canadian inflation coming in even lower than expected at –0.4 percent and validates the slowing inflationary rise view from the central bank.

The uncertain future of NAFTA had previously sapped the loonie from any positive impact from the interest rate hike, but comments this week about the importance trade by the Trump administration have lessened the anxiety about the trade deal. While the US representatives were sure to mention America first, even Trump conceded that America is not alone. The March deadline is fast approaching and negotiations have little to show for it. Elections in Mexico and the United States will make the trade deal a heavy politicized item in 2018. The biggest surprise at Davos from the White House was the apparent softening of their hard line on the Trans Pacific Pact (TPP). The now 11 nation deal was one of the first casualties of the administration and the remaining members agreed to go ahead without the US this week.

Oil prices have been boosted by the weak US dollar and encouraging signs that the global demand for energy is on the rise. The Organization of the Petroleum Exporting Countries (OPEC) production cut agreement was instrumental in stopping the free fall of crude. US shale producers were predicted to have ramped up their supply by now, but weather and other factors have stood in their way. The main risk for crude is a sudden revival of the US dollar that could trigger a sell off in commodities with investors looking to book profits at current three level highs.

Market events to watch this week:

Tuesday, January 30

- 10:00am USD CB Consumer Confidence

- 10:30am GBP BOE Gov Carney Speaks

- 7:30pm AUD CPI q/q

- 9:00pm USD President Trump Speaks

Wednesday, January 31

- 8:15am USD ADP Non-Farm Employment Change

- 8:30am CAD GDP m/m

- 10:30am USD Crude Oil Inventories

- 2:00pm USD FOMC Statement

- 2:00pm USD Federal Funds Rate

Thursday, February 1

- 4:30am GBP Manufacturing PMI

- 10:00am USD ISM Manufacturing PMI

Friday, February 2

- 4:30am GBP Construction PMI

*All times EST

. ){kind=link}