Wednesday January 24: Five things the markets are talking about

There is no rest for the wicked and that includes the once “mighty” dollar, as the buck, for a third consecutive session, extends its decline to a new three year low against most G10 currency pairs overnight. Global equities, again, have had another mixed session, while gold added to its recent gains.

Investors’ attention now shifts to tomorrow’s European Central Bank (ECB) monetary policy meeting, while keeping one eye on the annual economic conference in Davos, Switzerland.

The dollar remains a key focus as traders increasingly cite concerns about a widening U.S trade deficit and the markets growing belief that G7 monetary policy, ex-U.S, will shift away from their ultra-easy monetary policies this year.

Not aiding the U.S dollar are comments from Treasury Secretary Mnuchin who noted that he “was not concerned about the current level.”

Note: Barring any last minute changes in Washington, President Trump is expected to join other world leaders in Davos.

1. Stocks mixed results

In Japan, the Nikkei share average took a breather overnight after rising to a three-decade high Tuesday, as weakness in exporters offset gains in real estate stocks. The Nikkei dropped -0.4%, while the broader Topix shed -0.3%.

Down-under, Aussie shares closed higher Wednesday, boosted by financial and healthcare stocks. The S&P/ASX 200 index rose +0.3%.

In Hong Kong, the benchmark Hang Seng Index has rallied for a seventh consecutive session to end at a new high, as strength in energy shares offset weakness in IT and finance plays. At the close of trade, the Hang Seng index was up +0.08%, while the Hang Seng China Enterprises index rose +0.97%.

In China, stocks extended their climb, with the main indexes reaching new two-year peaks. At the close, the Shanghai Composite index was up +0.4%, while the blue-chip CSI300 index was up +0.19%.

In Europe, regional indices trade mostly lower, consolidating after recent gains with the exceptions of the Swiss SMI, which trades modestly higher. The U.K’s FTSE is underperforming on the back of continued strength in sterling (£1.4090) weighing.

U.S stocks are set to open in the black (+0.2%).

Indices: Stoxx600 -0.1% at 402.3, FTSE -0.5% at 7694, DAX -0.1% at 13544, CAC-40 -0.2% at 5524, IBEX-35 -0.2% at 10588, FTSE MIB -0.2% at 23779, SMI +0.5% at 9595, S&P 500 Futures +0.2%

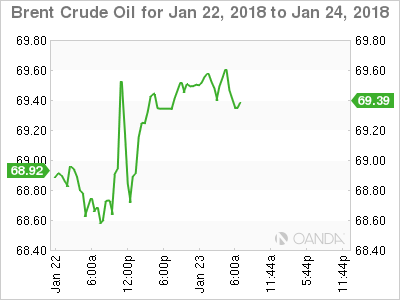

2. Oil prices ease as U.S. crude inventories rise unexpectedly, gold higher

Oil prices have slipped a tad, under pressure from a rise in U.S crude inventories.

Ahead of the U.S open, Brent futures have eased -24c to +$69.72 a barrel, after climbing above +$70 this month for first time in three-years. U.S West Texas Intermediate (WTI) futures are unchanged at +$64.47 a barrel.

Data yesterday from the American Petroleum Institute (API) showed crude inventories rose by +4.8m barrels over the week, compared with expectations for a decline of -1.6m barrels. Gas stocks also rose.

Traders will take their cues from today’s official U.S government inventory data (EIA), which is due out at 10:30 am EDT.

Note: Data shows that investors hold more ‘bullish’ positions in crude futures and options than at any time on record, which has been encouraged by falling global inventories.

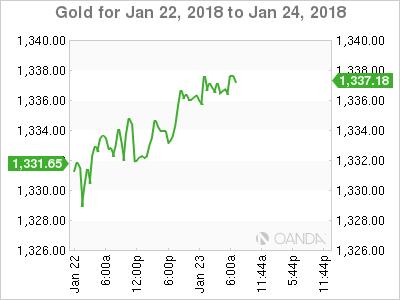

Gold prices have again edged higher, drifting towards its four-month high print of last week, as the U.S dollar sank to a fresh three-year low. Investor worries about a potential trade war has promoted the risk-aversion trading strategy. Spot gold is up +0.1% at +$1,342.30 per ounce.

3. ECB rate decision looms

Ahead of the U.S open, Euro bond yields again have backed up a tad, as caution settles into the fixed income markets ahead of tomorrows ECB rate announcement and press conference.

Tomorrow’s event is expected to be livelier than recent meeting, now that ECB policy makers have suggested that ‘early’ 2018 for a revision of its policy guidance.

However, the EUR (€1.2332) sitting atop of its three years highs could throw a spanner into the works and encourage President Draghi, in his press conference, to play down talk of an imminent change in the ECB’s policy stance.

Note: The EUR has gained +17% outright in the past 12-months – its strength puts downward pressure on inflation.

The yield on 10-year Treasuries has backed up +1 bps to +2.63%. In Germany, the 10-year Bund yield has gained +1 bps to +0.57%, while in the U.K, the 10-year Gilt yield has climbed +1 bps to +1.366%, the highest yield in almost three-months.

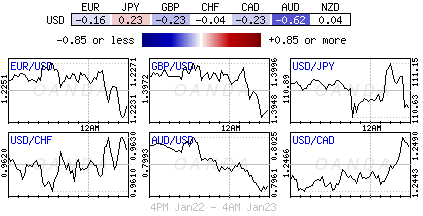

4. Dollars downfall continues

The U.S dollar has managed to print fresh lows against most G10 currency pairs after U.S Treasury Secretary Mnuchin said he “welcomed its weakness” and Euro data (see below) showed that the eurozone economy has started the new year at its strongest pace in over a decade.

EUR/USD (€1.2332) is trading atop of its three-year highs. Stronger regional fundamentals have been the ‘single units’ biggest supporter. Now that the EUR has breached the psychological €1.2300 handle, tech traders have the sights firmly on the €1.25 barrier.

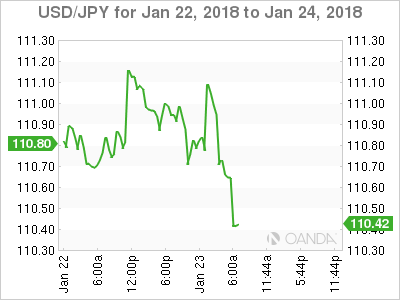

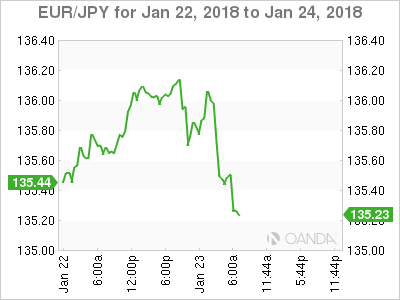

Meanwhile, on the back of the greenback’s weakness and despite ‘dovish’ talk from the Bank of Japan (BoJ) this week, the yen has pushed through the ¥110 barrier to ¥109.53 for the first time in four-months.

Sterling has managed to trade above the £1.4100 level despite mixed wage and jobs data.

Bitcoin (BTC) is trading at around $11,000.

5. Eurozone economy picks up speed

Data this morning shows that the Purchasing Managers Index collectively for the eurozone rose to 58.6 this month from 58.1 in December, reaching its highest level in almost 12-years.

Note: This mornings reading is consistent with a q/q growth rate of +1%, which would mark a pickup from the +0.7% recorded in the three-months through September and reason why the ECB has halved its monthly purchase of bonds (QE).

Digging deeper, the strong pace of growth appears set to continue over coming months since the flow of new orders was also robust. All the ECB requires now is inflation!