The US dollar ended up mixed against major pairs after the release of the U.S. non farm payrolls (NFP) report for February and news of a potential meet up between North Korea and American leaders. The NFP was a mixed bag with a monster 313,000 jobs gain but underperforming wage growth at 0.1 percent. US President Donald Trump tweeted about a meeting with Kim Jong Un being planned which capped a difficult week for US international relations after the steel and aluminum tariffs could be a non starter as a long list of nations are demanding exceptions.

- US worker wages missed despite massive jobs gains in February

- US inflation expected to slowdown

- US retail sales forecasted to bounce back

Dollar Mixed on Strong Jobs but Tame Wage Growth

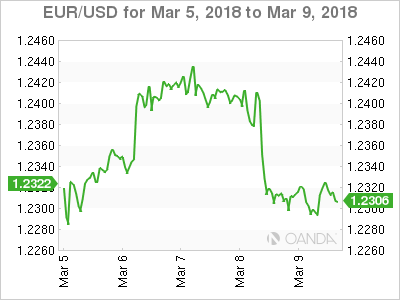

The EUR/USD lost 0.07 percent in the last five days. The single currency is trading at 1.2307 and its trading near where it opened on Monday. The EUR started the week appreciating versus the USD but it all took a U-turn on Thursday. The European Central Bank (ECB) kept rates and quantitive easing unchanged but did remove mention of adding more stimulus if the economy needed it. ECB President Mario Draghi was neutral with his comments as he praised rising European growth but also mentioned slow inflation and trade challenges ahead.

The EUR/USD lost 0.07 percent in the last five days. The single currency is trading at 1.2307 and its trading near where it opened on Monday. The EUR started the week appreciating versus the USD but it all took a U-turn on Thursday. The European Central Bank (ECB) kept rates and quantitive easing unchanged but did remove mention of adding more stimulus if the economy needed it. ECB President Mario Draghi was neutral with his comments as he praised rising European growth but also mentioned slow inflation and trade challenges ahead.

The pair stayed close to 1.23 after the NFP jobs report came out. The big gains in the number of jobs were more than offset by the low wage growth component. The lack of inflationary pressure will add ammunition to the doves within the Federal Open Market Committee (FOMC). The market still expected an interest rate hike on March 21, with 86 percent probably of a 25 basis points lift putting the range in 1.50–1.75 percent.

Next week will be more quiet with US inflation and retail sales to dictate the pace of the US dollar. Inflation anxiety has derailed stock market gains as rising costs of living would validate the Fed’s tightening policy and spell an even more rapid rise of interest rates. The consumer price index data will be published on Tuesday, March 13 at 8:30 am EDT. Retailers are hoping for a rebound on the last two months. Retail sales will be released by the Census Bureau on Wednesday, March 14 at 8:30 am EDT.

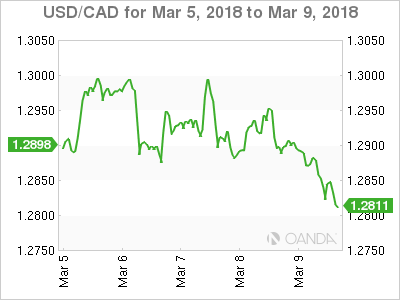

The USD/CAD lost 0.43 percent during the week. The currency pair is trading at 1.2829 after both Canada and the United States released employment reports for the month of February. The US added a massive 313,000 jobs last month, but investors were focused on the hourly earnings, which fell below expectations to 0.1 percent and the previous month’s data was also revised downward. Given the market anxiety with inflation this is a wrench in the plans of the U.S. Federal Reserve.

The USD/CAD lost 0.43 percent during the week. The currency pair is trading at 1.2829 after both Canada and the United States released employment reports for the month of February. The US added a massive 313,000 jobs last month, but investors were focused on the hourly earnings, which fell below expectations to 0.1 percent and the previous month’s data was also revised downward. Given the market anxiety with inflation this is a wrench in the plans of the U.S. Federal Reserve.

Canadian jobs came in below expectations with 15,400 positions instead of the forecast of 21,300 but they were enough to drive the unemployment rate lower to 5.8 percent. Concerns remain about the rise of part time jobs at the expense of full time positions. The loonie appreciated on a solid report, specially given last month’s drop of 88,000 jobs and the sell-off of the dollar that also put oil prices higher.

Bank of Canada (BoC) Governor Poloz will speak at Queen’s University on Tuesday, March 13 at 9:15 to deliver a very timely speech titled: “Today’s Labour Market and the Future of Work”. In the latest employment report it was clear the government was the biggest driver of employment with 50,300 jobs. It seems the job market like the rest of the Canadian economy is showing signs of the anticipated slowdown in the fourth quarter of 2017 with the BoC not in a rush to hike interest rates.

The CAD has had a horrible start to 2018 and is down 2.51 percent against the USD year to date as the uncertainty of the fate of NAFTA lingers with the 8th and final round to take place at the end of the month. The Canadian economy is slowing down, which in turn will make it less likely the Bank of Canada (BoC) keeps pace with the Fed’s rate hike path. With Canada being exempt from the steel and aluminum tariffs the threats from the Trump Administration are less credible, but that does not mean NAFTA is out of the woods yet as the White House can still push a unilateral move however unpopular it might be even within the Republican party.

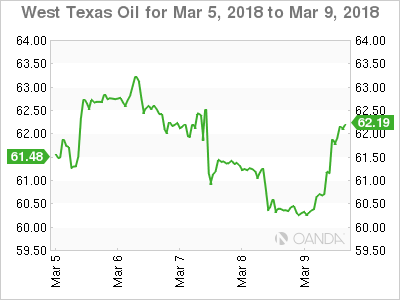

Energy prices bounced back on Friday and recouped most of the losses from earlier in the week. A 2 percent gain in the last day of the trading week took West Texas Intermediate to trade at $62.16. Oil prices started a weekly downward trend on Tuesday as inventories were coming out with confirmed buildups. The Energy Information Administration (EIA) weekly crude stocks report on Wednesday came in at 2.4 million additional barrels. The biggest factor keeping energy prices under pressure has been increase of supply concerns about US shale producers.

Energy prices bounced back on Friday and recouped most of the losses from earlier in the week. A 2 percent gain in the last day of the trading week took West Texas Intermediate to trade at $62.16. Oil prices started a weekly downward trend on Tuesday as inventories were coming out with confirmed buildups. The Energy Information Administration (EIA) weekly crude stocks report on Wednesday came in at 2.4 million additional barrels. The biggest factor keeping energy prices under pressure has been increase of supply concerns about US shale producers.

The EIA expected US crude production to reach 11.17 million barrels per day in the fourth quarter of 2018. This level of supply would put the US in the number one spot, overtaking Russia as the biggest producer. Russia and Saudi Arabia are part of the Organization of the Petroleum Exporting Countries (OPEC) crude output cut agreement along with other major producers. This has allowed US producers to ramp up production to take advantage of the stability in prices. Weather disruptions have impaired the ramp up in output, but analysts are tracking that potential surge in supply and see more downside for energy prices despite the best efforts of Russia and OPEC producers.

Market events to watch this week:

Tuesday, March 13

- 6:30am GBP Annual Budget Release

- 7:30 am USD CPI m/m

- 7:30 am USD Core CPI m/m

- 9:15am CAD BOC Gov Poloz Speaks

- 9:00pm CNY Industrial Production y/y

Wednesday, Mar 14

- 3:00am EUR ECB President Draghi Speaks

- 7:30am USD Core Retail Sales m/m

- 7:30am USD PPI m/m

- 7:30am USD Retail Sales m/m

- 9:30am USD Crude Oil Inventories

- 4:45pm NZD GDP q/q

Thursday, Mar 15

- 3:30am CHF Libor Rate

- 3:30am CHF SNB Monetary Policy Assessment

Friday, Mar 16

- 7:30am USD Building Permits

*All times EDT