Here are the latest developments in global markets:

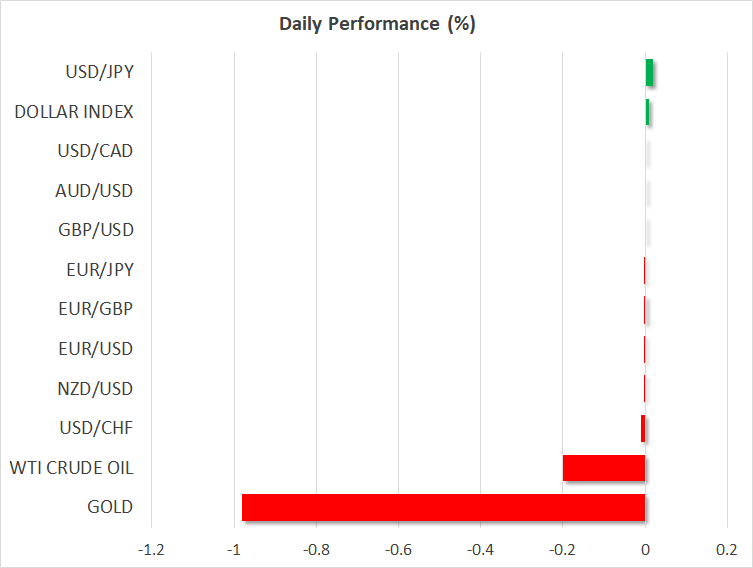

FOREX: The US dollar came under fresh selling pressure yesterday after President Donald Trump stepped up the trade war with China and threatened additional tariffs on Chinese imports. The greenback briefly dipped below the key 107 level, having hit a 5-week high of 107.49 yen earlier in the day. Market participants chose instead to focus on the strong economic fundamentals of the US and global economy and the dollar quickly recovered, with dollar/yen last trading around 107.40 and the dollar index around 90.50. The euro remained subdued after this week’s weak PMI readings for the Eurozone and stayed close to yesterday’s 5-week low of $1.2212. Sterling also lost ground versus the dollar following disappointing services PMI out of the UK and was trading lower at $1.3987 at the European open. The Canadian, Australian and New Zealand dollars were slightly down against their US counterpart too, though the loonie did hit a more than one-month high of C$1.2740 to the greenback yesterday on optimism about a NAFTA deal.

STOCKS: Asian stocks failed to get inspired by a third day of strong gains on Wall Street overnight as escalating trade tensions between the US and China weighed in risk sentiment once again. Japan’s Nikkei closed 0.4% down on the day but Hong Kong’s Hang Seng index managed to post gains of 1%. Markets in China were closed for a national holiday. In Europe, major indices opened lower, with the German Dax and the French CAC both down by 0.4%. London’s FTSE saw smaller losses and was last trading 0.25% lower. US stock futures were also in the red, indicating the recent run of gains is about to end.

COMMODITIES: Gold prices failed to get a boost from the dip in risk appetite after President Trump turned up the heat in the Sino-US trade dispute. The precious metal extended this week’s losses to fall towards $1321 to a more than 2-week low. Oil prices were also under pressure today, with WTI crude falling by 0.6% to $63.14 a barrel and Brent crude by 0.5% to just below $68 a barrel. The rise in trade tensions weighed on the oil market but losses were minimized as there was some support from the surprise increase in US crude stocks in this week’s EIA report.

Major movers: FX markets, dollar rebound undeterred by Trump’s latest move

Major pairs were relatively steady this morning despite the slight deterioration in risk appetite. The latest bout of risk-off came after the US President yesterday instructed his administration to find $100 billion worth of additional tariffs on Chinese products in an angry response to China’s retaliatory measures against the earlier import taxes announced by Trump.

On Wednesday, fears of a trade war appeared to be subsiding after the White House’s chief economic advisor Larry Kudlow indicated the US may not go through with the proposed tariffs and is seeking to negotiate a solution to the trade dispute with China. But the latest developments suggest the stand-off may get worse before the two sides come to an agreement.

For now though, traders are focusing their attention on the upcoming jobs report out of the US later in day as well as on the earnings season which gets underway next week. This was enough to drive the dollar to 5-week high against a basket of currencies, with its index hitting 90.60 in European trading today and dollar/yen holding comfortably above the 107 handle.

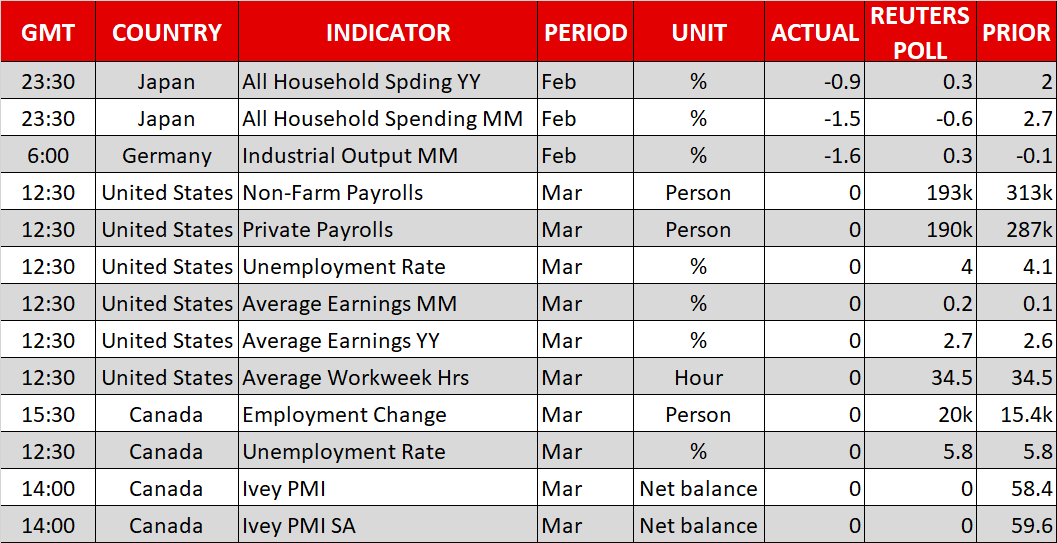

However, the risk-off and associated safe-haven demand helped the yen appreciate against most other currencies despite disappointing data out of Japan today. Household spending in Japan fell by a bigger-than-expected 1.5% month-on-month in February versus forecasts of a 0.6% fall. The yen was up by 0.1% against the euro and the pound at 131.31 per euro and 150.33 per pound.

The euro meanwhile continued its downtrend this week with more negative data dragging down on the currency today. Industrial output in Germany plunged by 1.6% m/m in February, missing forecasts of a 0.3% increase. The German data is the latest in a series of indicators pointing to slower growth in the Eurozone in the first quarter of 2018. The single currency was last trading at $1.2231.

The Canadian dollar paused for breath on Friday but looked set the be the week’s biggest riser against the greenback on signs that a NAFTA deal is within reach. The Canadian Prime Minister Justin Trudeau said on Thursday that talks between the US, Canada and Mexico were “moving forward in a significant way”. The loonie gave back some of those gains today however, easing to around C$1.2780 to the US dollar.

Day ahead: All eyes on US jobs report; Powell speech also awaited

As the first week of April comes to an end it’s time for another US jobs report with traders hoping for further evidence of a continuation of the goldilocks economy. Consensus forecasts are that the rosy picture of an expanding labour market and modest wage growth didn’t change last month. Nonfarm payrolls are expected to rise by 193k in March, down from February’s surge of 313k jobs but still a healthy figure. Average hourly earnings are forecast to edge up to 2.7% year-on-year.

Canada is also expected to report its jobs report. Employment is forecast to rise by 20k in March, with the unemployment rate holding steady at 5.8%. A stronger-than-expected reading could push the loonie to fresh highs, taking closer to the C$1.27 level. But a weaker report could deepen today’s correction versus the greenback.

Also on the horizon today is a speech by new Federal Reserve Chair, Jerome Powell at 17:30 GMT. Powell will give a speech on the economic outlook before the Economic Club of Chicago. The dollar could receive a double boost should the NFP report beat expectations and Powell to sound hawkish. But under the current climate of escalating trade tensions, disappointing jobs numbers and a cautious Powell could reverse the dollar’s recovery.

{kind=link}