Here are the latest developments in global markets:

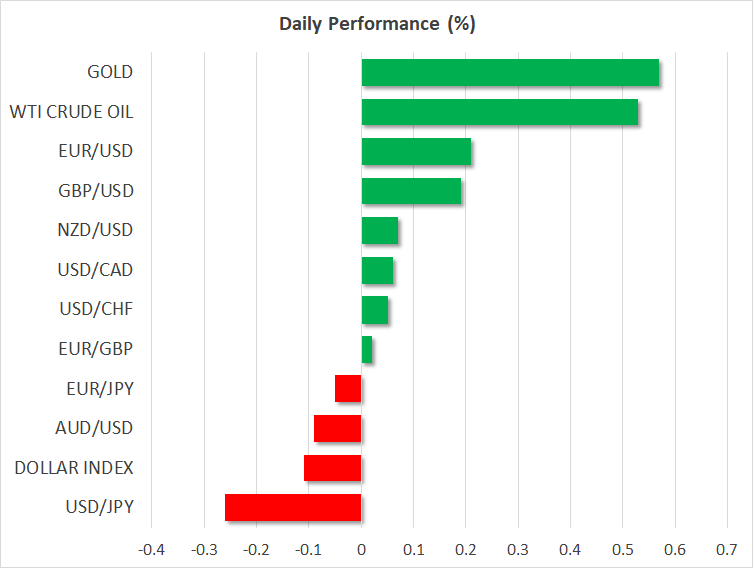

FOREX: While trade concerns seemed to ease following an encouraging speech by the Chinese President yesterday, who promised to improve the business environment for foreign companies, a pledge later outlined in more detail by the People’s Bank of China Governor, geopolitical fears appeared in the horizon. Particularly investors turned cautious after Western countries including the US and France were considering taking military action against Syria’s government in response to last week’s chemical attack in the region, with Russia warning Washington that it would shoot down any US missiles. The dollar index edged down to a two-week low of 89.44 (-0.08%) ahead of the US CPI figures and the FOMC meeting minutes due today, while dollar/yen almost reversed yesterday’s gains, falling to 106.93 (-0.24%). On the other hand, pound/dollar was on the rise today reaching a two-week high of 1.4222, but worse-than-expected industrial figures pushed the pair down to 1.4193 afterwards (+0.14%). Euro/dollar was also enjoying some gains, crawling up to a fresh two-week peak of 1.2386 (+0.19%) on the back of a weaker dollar despite an ECB spokesman playing down ECB Nowotny’s rate hike comments. In antipodean currencies, aussie/dollar inched down to 0.7754 (-0.05%), while kiwi/dollar managed to reverse today’s losses, rising slowly to 0.7365 (+0.08%). Dollar/loonie was flat at 1.2607 (+0.03%). The Turkish lira hit a fresh record low against the greenback at 4.1552 per dollar.

STOCKS: European stocks retreated moderately during early European session affected by rising tensions in Syria, with the European air control warning airlines over airstrikes on Syria over the next 72 hours. The pan-European STOXX 600 was down by 0.22% at 0900 GMT, with the British supermarket Tesco being the best performer after the company reported a 28% growth in full-year profits. The blue-chip Euro STOXX 50 fell by 0.33%, the German DAX 30 declined by 0.26%, the French CAC 40 retreated by 0.25%, while UK’s FTSE 100 moved lower by 0.07%. Asian equities closed mixed, while indices tracking US stock futures were in the green, pointing to a positive open.

COMMODITIES: Geopolitical risks also affected oil prices negatively early on Wednesday as the Middle East is considered one of the largest world crude exporters and any military activities in the region could disrupt oil markets. However, the market shrugged off those risks afterwards, following comments by the Saudi Arabian energy minister who expressed his satisfaction regarding the current market conditions and said that Saudi Arabia would not let another supply glut to develop. WTI crude and Brent were last seen at $65.81/barrel (+0.46%) and $71.19/barrel (+0.21%) respectively. In precious metals, gold hit a one-week high of $1346.40 (+0.53%).

Day Ahead: US CPI & FOMC meeting minutes gather attention

The dollar will be in the spotlight later in the day as FOMC meeting minutes and US CPI figures could bring fresh volatility to the currency.

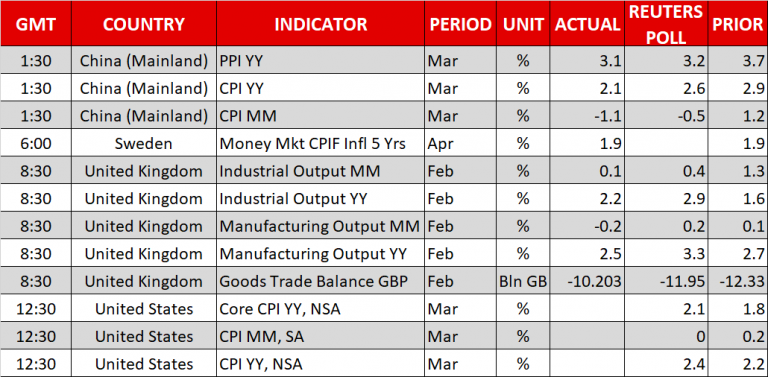

At 1230 GMT, the US Bureau of Labour Statistics will release CPI figures for the month of March. According to forecasts, the index is expected to gain 0.2 percentage points, rising to 2.4% y/y, while the core equivalent is anticipated to inch up 0.3 percentage points to 2.1% y/y. While this is not the Fed’s preferred inflation measure – this is the core PCE index –, an upside surprise in the CPI numbers could increase speculation that inflation is probably running to the upside. Note that on Tuesday the core PPI came in at 2.9% y/y in the 12 months through March, printing the biggest increase since August 2014, after climbing by 2.7% y/y in February.

Later at 1800 GMT, the Federal Open Market Committee will publish minutes from its latest meeting on March 20-21 which was chaired for the first time by Jerome Powell. At that meeting, policymakers raised interest rates as was widely expected and the closely-watched dot plot signaled two more rate hikes for 2018, which was already priced in by the markets. The latter was interpreted as a dovish sign since speculation was in the air that the Fed could deliver four rate hikes in total in 2018 instead of three. Policymakers, though, appeared more optimistic about this year’s rate path as the number of officials backing a steeper monetary tightening increased despite the median “dot” remaining unchanged at three hikes. The minutes could also reveal the Fed’s view on Trump’s trade policy, another spot that could add some volatility to the dollar. It should be also noted that with easing concerns over trade war, traders are widely expecting a rate hike in June. As indicated by the Fed funds futures, chances of a 25bps hike in June surged this week to 95%.

Also, on the agenda today, investors will look through the EIA report on US crude oil inventories. Crude inventories are anticipated to drop by 0.189 million barrels in the week ending April 6 compared to a fall of 4.617mn in the preceding week.

During early Asian session, New Zealand electronic card retail sales for the month of March are scheduled to be released at 2245 GMT, with forecasts supporting a growth of 0.5% y/y compared to a contraction of 0.3% y/y seen previously. A few minutes later at 2300 GMT, RICS house price balance will come into view in the UK.

As for today’s public appearances, ECB President, Mario Draghi will be speaking in Frankfurt at 1100 GMT, while ECB members Pentti Hakkarainen and Ignazio Angeloni are scheduled to deliver remarks at 1300 GMT and 1440 GMT respectively. In the US, Facebook’s chief executive, Mark Zuckerberg, will be in the hot seat for the second day, testifying before the House Energy and Commerce Committee regarding the sharing of private information with the London-based data mining firm Cambridge Analytica which had connections with Trump’s campaign in 2016.

{kind=link}