Here are the latest developments in global markets:

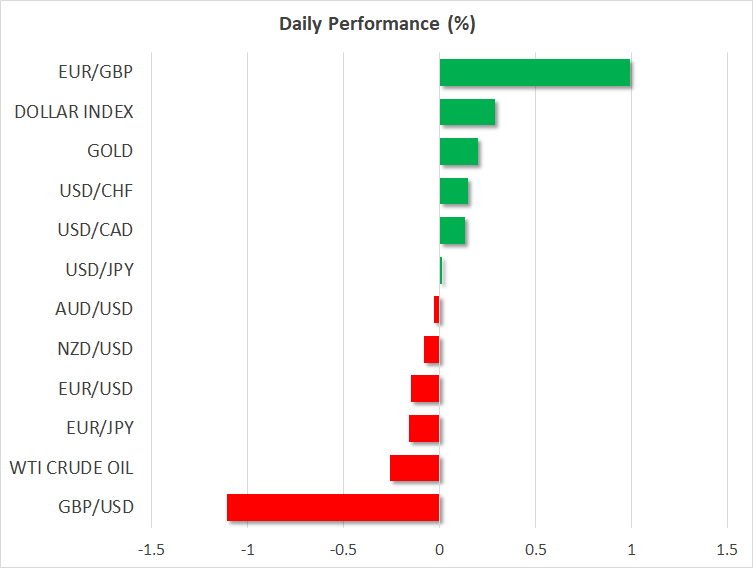

FOREX: Dollar bulls were set to win another battle for the fifth week mainly on the face of rising Treasury yields and in the absence of negative trade headlines. Geopolitical risks eased further as well after the North and South Korean leaders signed on Friday a declaration to end the war between the regions and confirmed their common prospects to denuclearize the Korean peninsula ahead of a crucial meeting between the North Korean leader and the US President at the end of May or early June. Dollar/yen remained mostly bid above the 109 key-level, last seen at 109.33 (+0.04%) and little changed after the BoJ decided to keep its rates steady but remove the timeframe for achieving its inflation goal. Against a basket of major currencies though, the dollar managed to win further ground as the pound and the euro were heading downwards on the day, with the dollar index hitting a fresh 3 ½ -month high of 91.90 (+0.28%). Particularly, pound/dollar dived to a two-month trough of 1.3778 (-0.91%) as the UK economy experienced the lowest growth rate in five years in Q1 2018. Euro/dollar was weaker as well at 1.2086 (-0.11%) despite Eurozone’s economic sentiment coming in better than expected in April. In the wake of the data, euro/pound recovered losses made during the past four-days, peaking at 0.8767 (+0.81%). Aussie/dollar and kiwi/dollar were flat at 0.7561 and 0.7063 respectively, near four-month lows. Dollar/loonie was also steady at 1.2869.

STOCKS: Upbeat earnings results in the banking sector and a recovery in tech stocks helped European shares to extend yesterday’s gains and tick another green box for the fifth consecutive week. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were up by 0.08% and 0.07% respectively at 0900 GMT, with the satellite firm SES being the biggest winner after its Q1 2018 earnings surpassed projections. The German DAX 30 surged by 0.76%, the British FTSE 100 jumped by 0.45% hitting almost 3-month highs as the pound was diving on the back of disappointing UK GDP growth data, while the French CAC 40 climbed by 0.12%. The Italian FTSE MIB declined by 0.65%. In Asia, stocks closed higher, while in the US, futures tracking stock indices were in the red, pointing to a negative open.

COMMODITIES: A rising dollar weighed on oil prices today, with WTI crude and Brent retreating to $67.94 (-0.37%) and $74.51(-0.31%) per barrel respectively. Fears whether the US will re-impose sanctions on Iran, however, continued to linger in the background, limiting the pullback in prices. Note that on May 12, the US President will decide whether to hold or leave the 2015 nuclear deal with Iran. In precious metals, gold remained near to its opening price, trading at $1,317.70 (+0.06%) per ounce, on track to close lower for the second week

Day Ahead: US GDP Growth and University of Michigan consumer sentiment int the spotlight

Friday’s calendar features key US data releases in the remainder of the day, with the dollar probably going through another round of volatility today if the numbers surprise ahead of a busy week, including the Fed’s next policy meeting, the NFP employment numbers, and core PCE inflation numbers.

US GDP growth figures for the first quarter are due at 1230 GMT, with analysts predicting a growth rate of 2.0% on an annualized basis, significantly below Q4 2017’s reading of 2.9%. While the pullback could be in line with the measure’s trend in recent years, a surprising miss could pressure the dollar. Alternatively, stronger-than-expected releases could help the greenback to continue its bullish run. Investors will also take a look at Q1 employment costs and the advance estimate of core PCE prices which will be published along with the GDP report.

At 1400 GMT, the focus will turn to April’s final readings on consumer sentiment delivered by the University of Michigan.

In oil markets, investors will keep a close eye on the US oil rig count issued by the Baker Hughes company at 1700 GMT. Potential increases in active drilling rigs could add losses to oil prices.

Turning to today’s public appearances, at 1400 GMT, Bank of England Governor Mark Carney will speak at the launch of the EconoME programme.

In politics, the German Chancellor Angela Merkel is meeting US President Donald Trump today in an attempt to avert a trade war between the EU and the US.