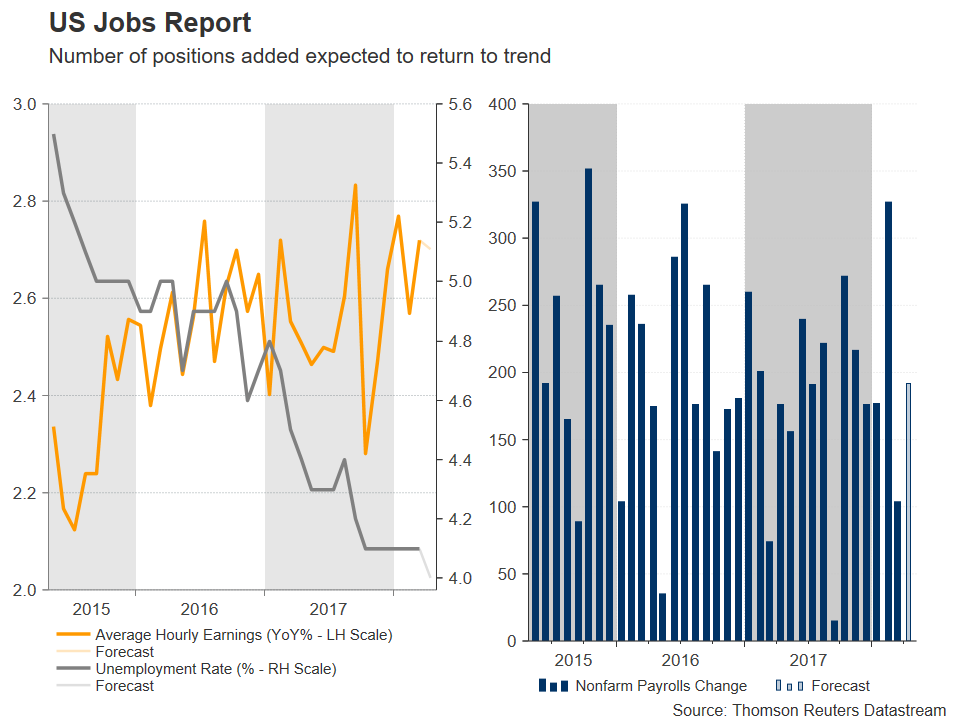

The US jobs report for the month of April is due on Friday at 1230 GMT. The report is arguably the most important monthly release out of the world’s largest economy. Tomorrow’s release is expected to show a return to trend in terms of the number of positions added to the economy after a weak weather-distorted number in March. Meanwhile, wage growth data are again likely to attract the most attention.

Analysts’ project the addition of 192k job positions in the US economy during April, far above March’s seven-month low of 103k. The previous month’s nonfarm payrolls print was attributed to transitory factors though – poor weather conditions in parts of the country – rather than signaling weakness in the labor market. The unemployment rate is forecast to tick down to 4.0%, its lowest since late 2000, after standing at 4.1% for six straight months – it is noteworthy, though, that this forecast has been missed in previous occasions. Meanwhile, average earnings, which have been attracting the lion’s share of attention in recent reports, are projected to expand by 2.7% y/y, the same pace as in March. However, wage growth is expected to ease on a monthly basis, with average earnings growing by 0.2%, down from March’s 0.3%.

There has been a gradual rise in wage growth in the US, something which attests to the tightening labor market but has also been instrumental for market participants in discounting a more aggressive policy normalization cycle by the Federal Reserve. Specifically, Fed funds futures currently show that markets have priced in two additional quarter percentage-point hikes by the US central bank in 2018, while they also assign a 15% probability for a third increase, which would take the total number for the year to four.

There has been a gradual rise in wage growth in the US, something which attests to the tightening labor market but has also been instrumental for market participants in discounting a more aggressive policy normalization cycle by the Federal Reserve. Specifically, Fed funds futures currently show that markets have priced in two additional quarter percentage-point hikes by the US central bank in 2018, while they also assign a 15% probability for a third increase, which would take the total number for the year to four.

The economic rationale for the abovementioned is that strong wage growth would stoke inflationary pressures, pushing inflation to reach the Fed’s target of 2%. In this respect, stronger-than-anticipated numbers on average earnings are likely to support the greenback tomorrow. However, gains in such a scenario may not be as profound as could have otherwise been the case, as FOMC members’ communication upon completion of the central bank’s meeting yesterday hinted that the Bank may be comfortable in allowing inflation to overshoot its 2% target without responding by steepening its rate path.

A print that is not discussed much but deserves a mention is U6 underemployment. This is a broader measure of unemployment which includes individuals who want to work but are discouraged to search for jobs, and those working in part-time positions but seeking full-time employment. In March, the relevant reading touched 8.0%, falling back to 11-year lows. It would be interesting to see whether it will continue edging lower in April.

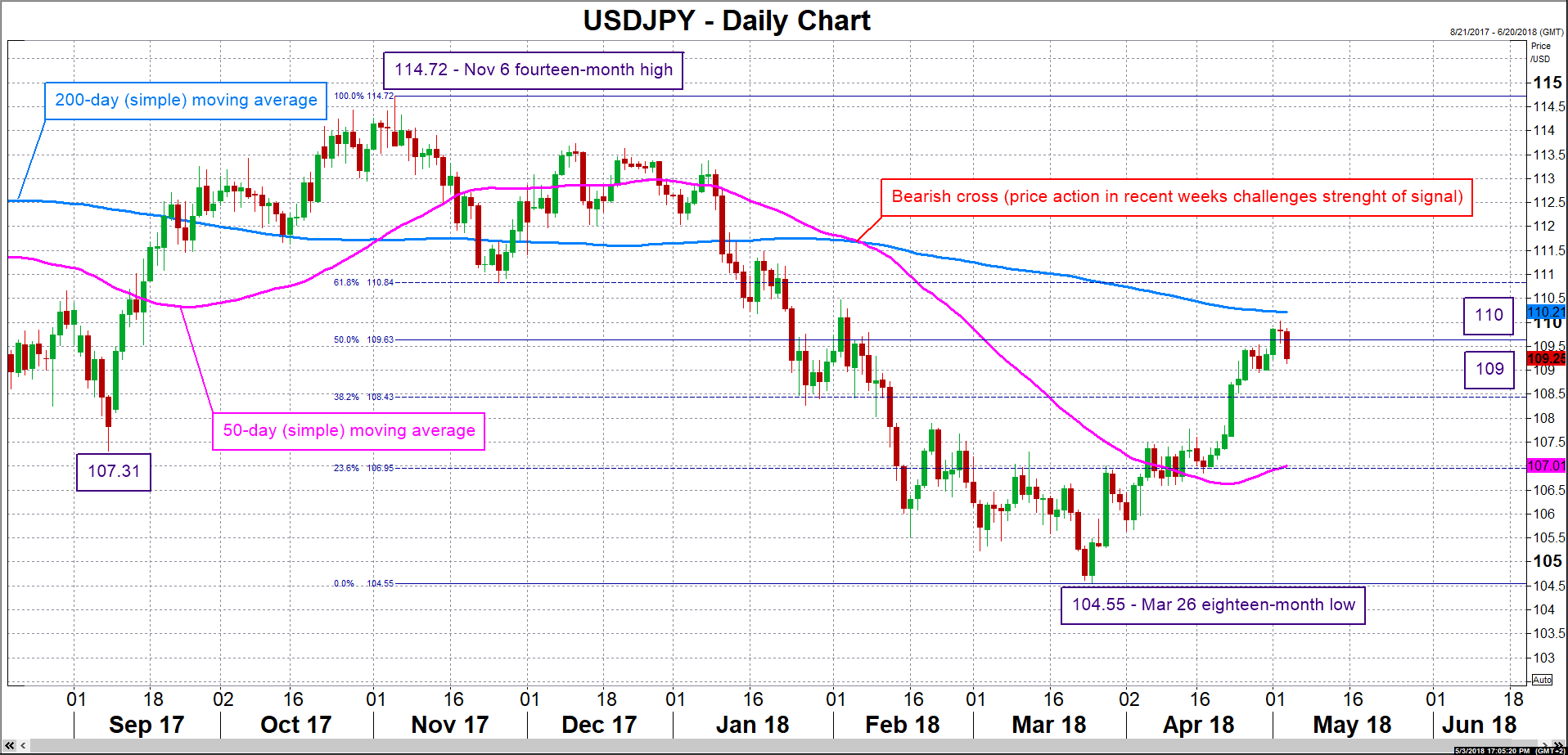

In terms of market reaction, upbeat figures are anticipated to boost the dollar versus other major currencies, refueling the currency’s rally from earlier in the week which seems to be somewhat running out of steam on Thursday. Focusing on dollar/yen, the pair seems to be meeting resistance at the moment at the 50% Fibonacci retracement level of the November 6 (a 14-month high) to March 26 (an 18-month low) downleg at 109.63. An upside break would turn the attention to the region around the 110 round figure for additional resistance; the area around this includes the current level of the 200-day moving average at 110.21, as well as Wednesday’s three-month high of 110.02. The 61.8% Fibonacci mark at 110.84 could act as an additional barrier further above. Disappointing readings on the other hand, are likely to exert downside pressure in USDJPY. Initial support might come around the 109 handle, with the focus shifting to the 38.2% Fibonacci level at 108.43 in case of steeper declines.

Earlier in the week, the ADP employment report showed the addition of 204k positions by the US private sector in April. This is sometimes viewed as a preamble to the more comprehensive nonfarm payrolls report which covers both the public and private sectors. It should be kept in mind though that it does not always deliver as an NFP precursor; for instance, it provided poor guidance in March by not offering an indication of the sharp fall in nonfarm payrolls.

{kind=link}