On Wednesday at 1400 GMT, the Bank of Canada will announce its interest rate decision and issue its press release, explaining the factors behind the decision. For the fifth time, though, policymakers are expected to keep borrowing costs unchanged at 1.25% as NAFTA and the US trade agenda remain a source of uncertainty for the Canadian economy, while the overloaded debt overhang continues to weigh despite a strong labor market. No conference or financial projections are scheduled to follow.

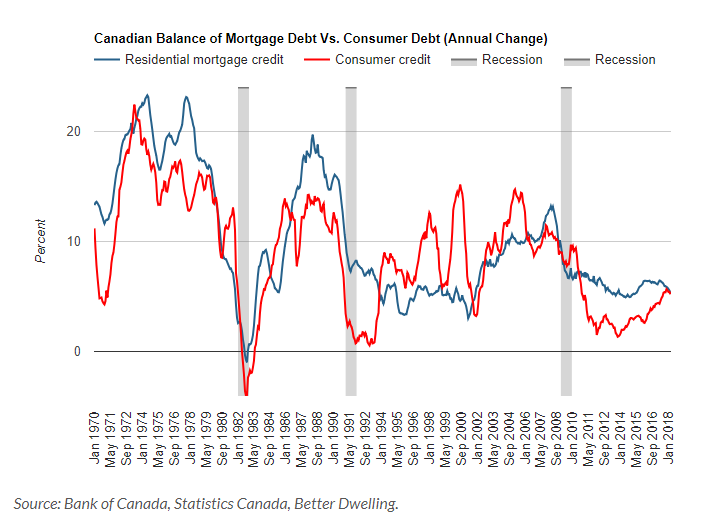

Two weeks ago, CPI readings out of Canada showed that headline inflation in April grew by 2.2%, less than the 2.4% forecast by analysts, though, still above the 2.0% midpoint of the BoC target range of 1-3.0%. Core measures, closely watched by the BoC, remained around 2.0% as well. Yet, wage growth at the same time was rising faster than inflation by 3.6% y/y, recording the highest expansion in six years, while the unemployment rate remained at the lowest in a decade at 5.8% – factors that otherwise could comfortably lead to higher interest rates. Nevertheless, the central bank might choose to lift rates later rather than now when it meets on May 30 as a quicker pace of rate hikes could put high indebted Canadian households and therefore consumption under pressure. However, a slower pace could increase demand for debt, making the country more vulnerable in case negative shocks emerge. Recall that Canadian household debt to disposable income stood near record highs in the fourth quarter of 2017, although the Bank of Canada has raised interest rates three times since July. Regarding mortgage debt, which holds a significant share of the total debt, it touched a new record in April, but the annual growth slowed to the lowest since 2001. In terms of consumption, retail sales – a proxy for household spending – posted the strongest expansion in five months in March. Having said that, the central bank will likely wait for better results as the gains were largely driven by auto sales. Excluding this volatile component, retailers saw their sales declining.

On the trade front, the latest data showed a wider trade deficit, with imports surpassing the rise in exports and jumping to record highs under a steady currency. Precarious NAFTA negotiations could have also kept exporters cautious as the latest round of talks failed once again to secure an agreement and more importantly meet a deadline of May 17 imposed by House speaker, Paul Ryan, in order for the US Congress to review it. Tensions are now intensifying ahead of a new deadline set by the end of May, while the member countries, Canada, the US and Mexico, are rushing to find a common ground before the Mexican elections on July 1 and the US mid-term elections in November take place, potentially prolonging the process under new legal bodies. Moreover, the clock is ticking down for US import tariffs on steel and aluminum which were temporarily exempted for Canada, and Mexico until June 1, while Trump’s recent order to investigate the auto industry – a key outstanding issue in NAFTA talks – added further stress to the markets on fears of new import tariffs. On the other hand, the rally in oil prices last week, brought smiles to Canadian oil exporters, offsetting losses related to trade risks in the commodity-linked loonie. But whether the rally in oil prices is overdone is another question to be considered.

According to overnight indexed swaps, chances for a rate rise on Wednesday are currently standing at 25.53% compared to nearly 31% last week, with analysts widely expecting the central bank to deliver two more rate hikes this year in July and December. Standing pat on rates, though, sounds reasonable for now as policymakers will likely prefer to wait for GDP growth readings due on Thursday to indicate how the economy evolved in the first quarter of the year.

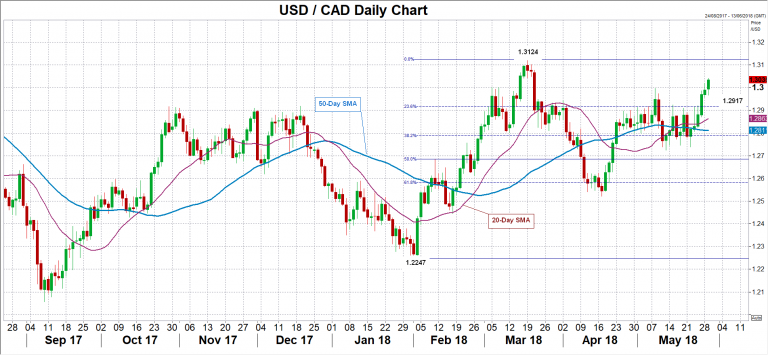

Still, in the forex markets, the loonie could attract gains if the decision statement embraces a positive economic outlook, pushing dollar/loonie down to the 23.6% Fibonacci of 1.2917 of the upleg from 1.2247 to 1.3124. Steeper declines could also target the area between the 20- and the 50-day simple moving averages currently at 1.2862 and 1.2810 respectively. On the other hand, if policymakers emphasize risks related to the US trade strategy, helping the dollar to extend gains, dollar/loonie could crawl towards the March peak of 1.3124, the highest level reached since the end of June.

{kind=link}