The US dollar is mixed as risk aversion has made traditional safe haven currencies (JPY and CHF) advance versus the greenback. The USD is higher against the EUR as the Spanish PM faces a confidence vote with the single currency still reeling from the Italian political crisis that in a worst case scenario could mean the exit of Italy from the European Union. Global stock markets have fallen as fears of contagion rise. The China and US trade stand off continues with the White House set to announce the list of items that are subject to new tariffs in June 15. The Bank of Canada (BoC) will release its rate statement on Wednesday, May 30 at 10:00 am EDT.

- ADP report forecasted to add 186,000 jobs

- US GDP second release for Q1 to remain unchanged at 2.3%

- BoC expected to leave interest rate unchanged at 1.25%

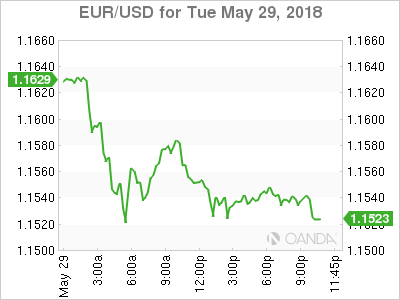

EUR Falls After Political Drama

The EUR/USD lost 0.77 percent on Tuesday. The single pair is trading at 1.1549 after the one-two punch of Spain and Italy. European politics were top of mind as euro sceptic parties rose in relevance across the board. The two largest economies faced their own battle but France and Germany avoided and end of the union scenario earlier. Italy as the third biggest economy is facing economic hardship and in certain aspects not fully recovered from the 2008 crisis. The coalition between the 5-star movement and the League was the last attempt to form a government, but their proposal got rejected as their spending plans could put the EU membership of Italy in jeopardy. If a new vote is called it would be a proxy exit referendum where Italians decide as early as July if they want to remain in the EU.

Spanish Prime Minister Mariano Rajoy will face a no-confidence vote on Friday and the ouster of his party could end up in new elections within months. The market event calendar will mostly focus in the US employment sector. The strongest pillar of the US economic recovery will not bring any headaches to the dollar. In contrast European data will be scarce with flash inflation data on Wednesday the biggest releases.

The biggest economic release in the market will come on Friday, June 1 with the publication of the U.S. non farm payrolls (NFP) report at 8:30 am EDT. The forecast is calling for a gain of 190,000 jobs after a strong 164,000 gain last month. Hourly wages will be in focus with a gain of 0.3 percent expected. The Fed is not worried about the US economy staying above 2 percent for long but it will be a decisive factor in the number of rate hikes in 2018.

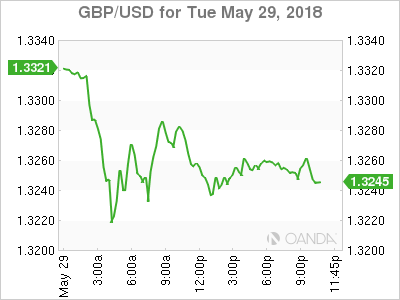

Hard Brexit Outcomes Pressure Pound

The GBP/USD lost 0.49 percent in the last 24 hours. The currency pair is trading at 1.3249 as risk aversion has benefited the USD. The health of the UK economy has taken off the table a short term rate hike from the Bank of England (BoE) and the warming from Governor Carney on a disruptive Brexit. Mr Carney said that if there is a smooth transition the central bank could take a more traditional path, but if there is a disorderly exit the BoE would have to act with a potential rate cut in the cards similar to the post Brexit referendum outcome in 2016.

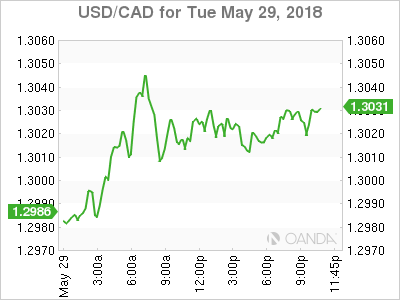

Bank of Canada (BoC) to Hold Citing Uncertainty

The USD/CAD gained 0.23 percent on Tuesday. The currency pair is trading at 1.3019 ahead of the rate statement form the Canadian central bank. The market does not expect a change in the benchmark rate given the surrounding uncertainty about the NAFTA negotiations and less than stellar economic indicators. High levels of household debt will give the BoC food for thought and the bank is not expected to lift rates until after the U.S. Federal Reserve does so again in June.

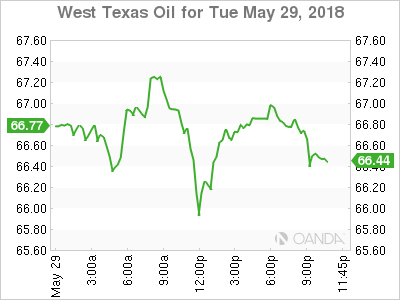

The price of oil has come off highs after the Organization of the Petroleum Exporting Countries (OPEC) is pondering easing the production cut agreement with other major producers. The deal was able to stabilize prices that were in free fall in 2014. The move worked, but it was only until there was geopolitical friction that prices really had upward momentum. Now with crude at a higher level producers could relax their production quotas and try to reap the benefits of higher prices. The main issue is that demand has not grown enough to justify current levels, and is more of a supply disruptions that have boosted oil prices.

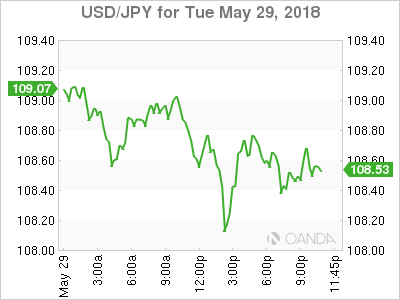

Yen Rises to One Month High on Safe Haven Flows

The USD/JPY lost 1.00 percent in the last 24 hours. The currency pair is trading at 108.32 with a surging yen touching a 30 day high. Safe haven buying of the JPY as trade concerns between the US and China escalate, as well as the political turmoil in continental Europe have put the currency

Market events to watch this week:

Tuesday, May 29

8:00pm JPY BOJ Gov Kuroda Speaks

Wednesday, May 30

8:15am USD ADP Non-Farm Employment Change

8:30am USD Prelim GDP q/q

10:00am CAD BOC Rate Statement

10:45am CHF SNB Chairman Jordan Speaks

9:00pm NZD ANZ Business Confidence

9:30pm AUD Private Capital Expenditure q/q

Thursday, May 31

All Day G7 Meetings

8:30am CAD GDP m/m

11:00am USD Crude Oil Inventories

Friday, June 1

4:30am GBP Manufacturing PMI

All Day G7 Meetings

8:30am USD Average Hourly Earnings m/m

8:30am USD Non-Farm Employment Change

8:30am USD Unemployment Rate

10:00am USD ISM Manufacturing PMI