EUR/USD

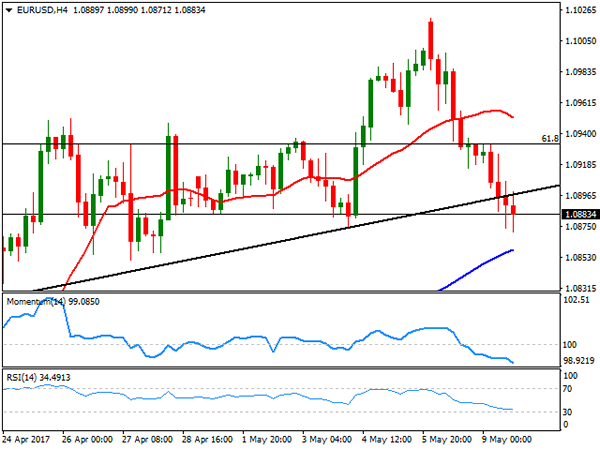

The American dollar advanced for a second consecutive day against its European rival, resulting in the pair setting a fresh 2-week low of 1.0863. The macroeconomic calendar was light in both economies, with minor reports still indicating steady growth in the Euro area, and slightly disappointing figures in the US. Nevertheless the greenback stood victorious, as speculative interest kept shifting its attention to Central Banks’ imbalances, and soft US data were not enough to prevent the Fed from acting next month.

The IBD/TIPP Economic Optimism Index, showed that US consumer confidence retreated modestly in May, down to 51.3 after printing 51.7 in April. Wholesale inventories surged by 0.2% in March, against market´s hopes for a 0.1% decline. A couple of Fed speakers hit the wires, with Kansas George saying that the US economy is on track to grow at “a slightly above-trend rate,” and therefore gradual rate hikes are the right path. In a different event, Rosengren centered on employment stating that further falls in the unemployment rate below 4%, would overheat the economy, prompting higher rates.

The EUR/USD pair was unable to regain the 1.0900 level, even despite German finance minister Schaeuble state that the normalization of the ECB’s monetary policy should start "shortly." The pair has broken below an ascendant trend line coming from April 24th low at 1.0820, and even completed a pullback to it before reaching the mentioned low, indicating that the slide is not over yet. Technical readings in the 4 hours chart also favor a new leg lower, as technical indicators maintain their strong bearish slopes near oversold territory, as the 20 SMA turns south well above the current level.

Support levels: 1.0850 1.0820 1.0770

Resistance levels: 1.0895 1.0930 1.0965

USD/JPY

The American dollar advanced for a second consecutive day against its European rival, resulting in the pair setting a fresh 2-week low of 1.0863. The macroeconomic calendar was light in both economies, with minor reports still indicating steady growth in the Euro area, and slightly disappointing figures in the US. Nevertheless the greenback stood victorious, as speculative interest kept shifting its attention to Central Banks’ imbalances, and soft US data were not enough to prevent the Fed from acting next month.

The IBD/TIPP Economic Optimism Index, showed that US consumer confidence retreated modestly in May, down to 51.3 after printing 51.7 in April. Wholesale inventories surged by 0.2% in March, against market´s hopes for a 0.1% decline. A couple of Fed speakers hit the wires, with Kansas George saying that the US economy is on track to grow at “a slightly above-trend rate,” and therefore gradual rate hikes are the right path. In a different event, Rosengren centered on employment stating that further falls in the unemployment rate below 4%, would overheat the economy, prompting higher rates.

The EUR/USD pair was unable to regain the 1.0900 level, even despite German finance minister Schaeuble state that the normalization of the ECB’s monetary policy should start "shortly." The pair has broken below an ascendant trend line coming from April 24th low at 1.0820, and even completed a pullback to it before reaching the mentioned low, indicating that the slide is not over yet. Technical readings in the 4 hours chart also favor a new leg lower, as technical indicators maintain their strong bearish slopes near oversold territory, as the 20 SMA turns south well above the current level.

Support levels: 1.0850 1.0820 1.0770

Resistance levels: 1.0895 1.0930 1.0965

GBP/USD

The GBP/USD pair closed the day flat around 1.2940, recovering from a fresh weekly low set at 1.2903 early London. There were no big news coming from the UK, although at the beginning of the day, the BRC report showed that retail sales jumped by 5.6% in April when compared to a year earlier, reverting the soft figures seen in the previous month. Investors are waiting for the upcoming BOE meeting, before making decisions on the pair. The Central Bank is expected to revise its inflation and growth forecasts, but also to maintain rates unchanged. Attention will therefore focus on how policy makers vote, as on the previous meeting 1 member voted for a hike. The technical picture is neutral-to-bearish, as despite bouncing from the mentioned low, the pair was unable to regain ground above its 20 SMA, whilst technical indicators have turned lower, but remain within neutral territory. Furthermore, the pair posted a lower low and a lower high daily basis, another sign of fading buying interest.

Support levels: 1.2900 1.2865 1.2830

Resistance levels: 1.2960 1.2995 1.3030

GOLD

As the dollar advanced gold prices extended their slide, with spot ending the day at a fresh 2-month low of $1,214.78 a troy ounce. The commodity closed the day barely $1 above that low, as coupling with dollar’s strength was lower physical demand for the metal. Improved market’s sentiment and chances of a Fed rate hike next month, will likely keep gold prices under pressure during the upcoming sessions. From a technical point of view, the daily chart shows that the price extended its slide below all of its moving averages, whilst technical indicators remain near oversold territory, with the RSI indicator accelerating its slide, anticipating a bearish continuation. In the shorter term, and according to the 4 hours chart, the commodity is also biased lower, given that the upside was contained by selling interest around a bearish 20 SMA, whilst the Momentum indicator holds well below its mid-line and the RSI indicator heads south around 24.

Support levels: 1,214.10 1,203.80 1,194.95

Resistance levels: 1,221.10 1,231.85 1,242.50

WTI CRUDE OIL

Oil prices were once again under pressure, with West Texas Intermediate futures ending the day at $45.90 a barrel, despite news headlines indicating that Saudi Arabia will reduce its crude oil exports to the Asian market by around 7 million barrels in June, as market participants still weigh more rising US production. Ahead of the US monthly stockpiles reports, expectations are of a 1.8 million barrels’ decline. In the meantime, the technical picture keeps favoring the downside, given that daily indicators resumed their declines after a brief upward correction, whilst the price remains far below all of its moving averages. For the shorter term, technical readings in the 4 hours chart also support a bearish extension, as the price is back below a bearish 20 SMA, while technical indicators turned sharply lower, entering negative territory after the price topped for the day at 46.76.

Support levels: 45.30 44.70 44.10

Resistance levels: 46.70 47.20 47.75

DJIA

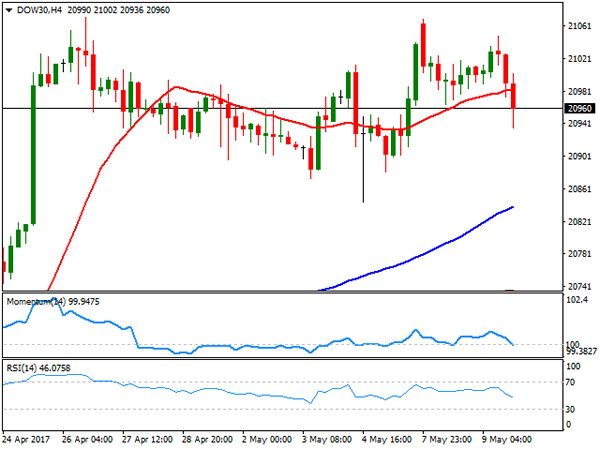

US equities closed mixed, with the DJIA settling at 20,975.78, down by 36 points, and the S&P losing 2 points and settling at 2,396.92. The Nasdaq Composite, on the other hand, added roughly 18 points to close at fresh record highs of 6,102.59. The energy sector was the worst performer, and within the DJIA, Chevron was the worst performer, shedding 1.56% followed by Cisco Systems that lost 1.24% and El du Pont that closed 1.12% lower. Nike led advancers by adding 1.05%, followed by Wall Mart that gained 0.83%. The Dow remained within its usual range, unable to find direction, and the daily chart shows that it holds above a bullish 20 SMA, whilst technical indicators extended their declines, but still holding above their mid-lines. The 20 DMA heads modestly higher around 20,840, limiting the downside. In the 4 hours chart, the index is currently breaking below its 20 SMA, whilst technical indicators are entering negative territory, leaning the scale towards the downside in the short term.

Support levels: 20,936 20,898 20,845

Resistance levels: 21,030 21,071 21,138

FTSE100

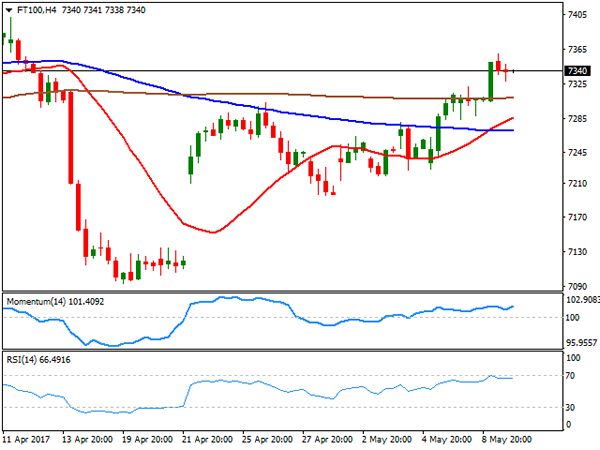

The FTSE 100 advanced 41 points to settle at 7,342.21 underpinned by a rally in mining equities, amid a rebound in copper prices. The London benchmark advanced for a fourth consecutive session, further helped by a softer Pound. Glencore added 2.27% and made it to the top 10 list, after the company cancelled its plans to close an Australian coal mine. Rolls-Royce was the best performer, adding 4.64%, while also up were Billiton, with a 2.22% gain and Fresnillo that gained 1.78%. Micro Focus led decliners, ending the day 5.65% lower, while the energy sector also edged lower, after PM Theresa May promised lower energy bills if she wins the General Election next June. The index stands at its highest in three weeks, and poised to extend its advance according to technical readings in the daily chart, as indicators accelerated their advances, now nearing overbought levels, whilst the benchmark moved further above its moving averages. In the 4 hours chart, the index is also biased higher after finally extending beyond its 200 SMA, and as technical indicators resumed their advances within positive territory.

Support levels: 7,327 7,284 7,247

Resistance levels: 7,360 7,402 7,447

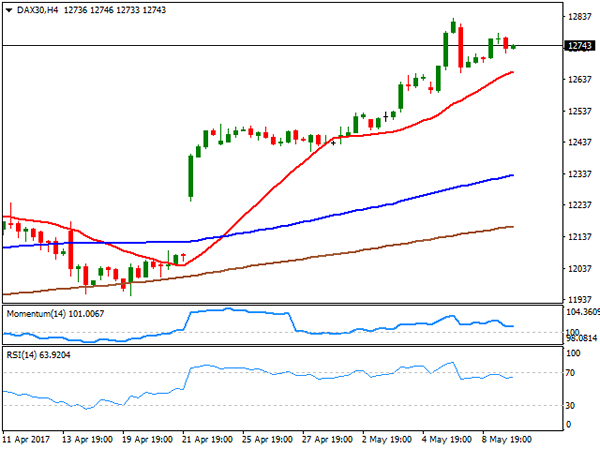

DAX

The German DAX added 54 points or 0.43% this Tuesday to settle at 12,749.12, backed by solid local data, as despite the trade balance headline missed expectations, exports surged to a record of €118.2 billion, whilst imports surged by 2.4% to €92.9 billion. Factory orders in the country fell, but by less than anticipated in March. E.ON was the best performer, up 3.86%, followed by Merck, which added 1.28%. The worst performer was insurer Muenchener that lost 1.34%, followed by Deutsche Post that shed 0.88%. Despite closing in the green, the DAX trimmed most of its daily gains ahead of the close, but so far, the bullish tone persists, as in the daily chart, the Momentum indicator regained the upside, now heading north at fresh multi-month highs, whilst the RSI barely corrected extreme overbought conditions before settling around 70. In the 4 hours chart, however, technical indicators eased within positive territory before losing directional strength, somehow anticipating decreasing buying interest. In this last time frame, the 20 SMA keeps heading north below the current level, offering a strong dynamic support around 12,661, with a break below it favoring additional declines.

Support levels: 12.720 12,668 12,623

Resistance levels: 12,765 12,812 12,850