- Deflationary spiral risk has negated confidence in China equities.

- US dollar has continued to hold steady against the yuan despite a broad-based sell-off against other major currencies ex-post US non-farm payrolls.

- The key intermediate support to watch on the USD/CNH will be at 7.2160.

Weak China inflation data offset positive China Big Tech news flow

The dreaded fear of a deflationary spiral in China has reached “code red” where the latest consumer inflation rate for June has flattened to 0% year-on-year from a gain of 0.2% year-on-year in May and came in below expectations of an increase of 0.2%. This latest reading in CPI is the weakest rate since February 2021.

In addition, producers’ prices (factory gate prices) continued to deteriorate further into contraction mode; it dropped -5.4% year-on-year, faster than a 4.6% fall in May, and worse than expectations of a -5.0% decline. Overall, it has marked the ninth consecutive month of producer deflation and its steepest fall since December 2015.

Time is running out for Chinese policymakers to negate the steepening rout in the internal demand environment that can potentially lead to further loss in consumer and business confidence if the deflationary spiral starts to be persistent. It may lead to a liquidity trap scenario in China where monetary policy tools will be less effective to stimulate real economic growth.

The forward pricing mechanisms of the stock market seem to have started to take into account some aspects of the negative feedback loop triggered by the liquidity trap scenario, earlier intraday gains of between 1% to 3.2% seen in today’s Asian session on the Hang Seng indices as well as China’s benchmark CSI 300 driven by China Big Tech equities as Chinese regulators have signalled on last Friday after the close of the Asian session to end a two-year plus of crackdown on the technology sector have been reduced by slightly more than half, CSI 300 (0.5%), Hang Seng Index (0.8%), Hang Seng TECH Index (1.25%), and Hang Seng China Enterprises Index (0.7%) at this time of the writing.

China’s yuan remained soft despite the broader USD sell-off

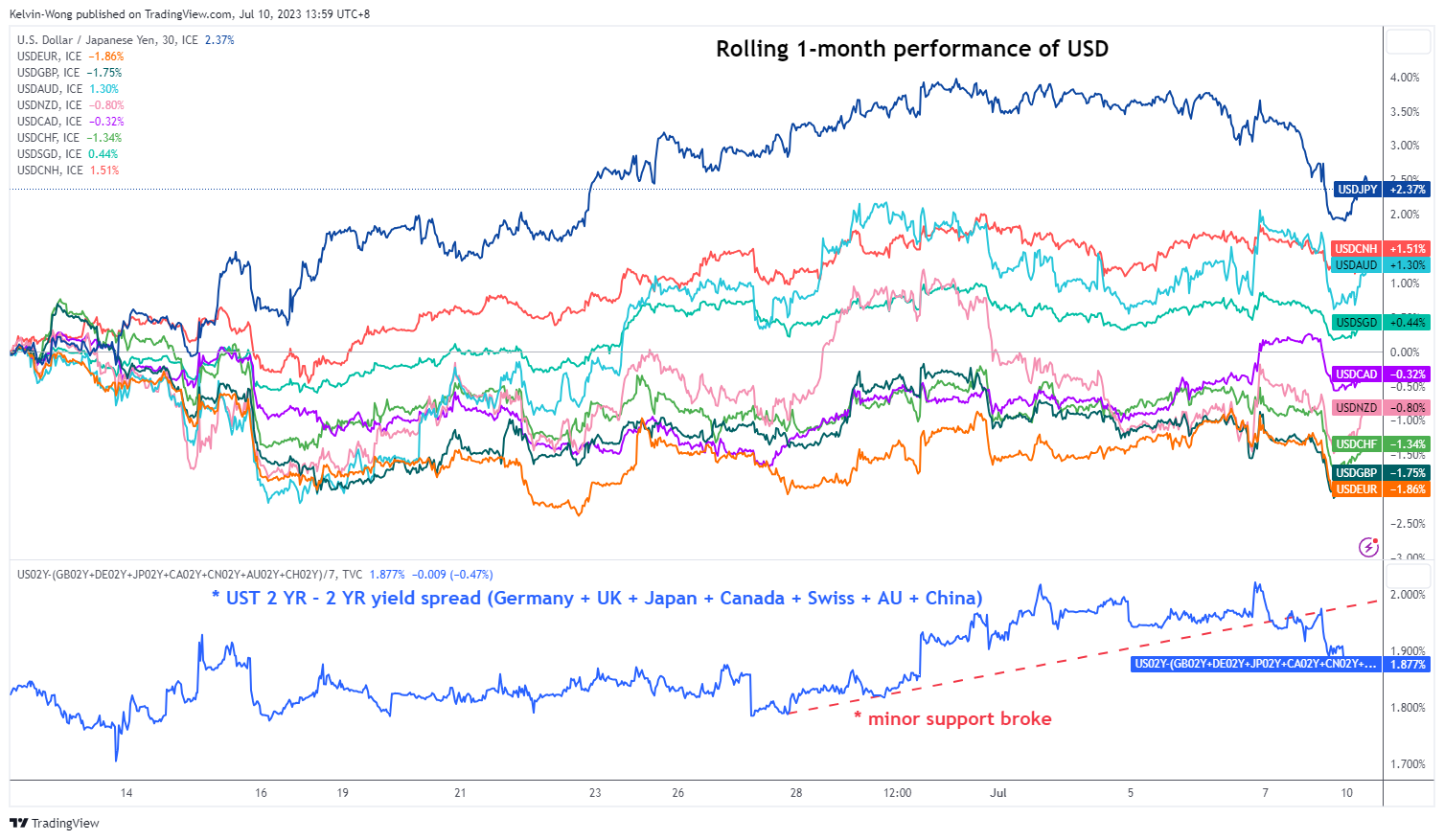

Fig 1: US dollar rolling 1-month performance as of 10 Jul 2023 (Source: TradingView, click to enlarge chart)

The US dollar sold off last Friday, 7 July reinforced by technical factors after the US Dollar Index cracked below its 50-day moving average that had been acting as a prior minor support since 28 June 2023, also ex-post US non-farm payrolls for June that came in below expectations (209K added vs. 225K consensus). Based on the rolling one-month performances as of today, the USD is weakest against the EUR (-1.89%), GBP (1.81%), and CHF (-1.35%) while holding steady against the offshore yuan, CNH (+1.44%).

In addition, the US Treasury 2-year yield premium over an average of key developed nations’ 2-year sovereign yields (Germany, UK, Japan, Canada, Switzerland, Australia, China) has narrowed as well.

USD/CNH short and medium-term uptrend phases remain intact

Fig 2: USD/CNH short & medium-term trends as of 10 Jul 2023 (Source: TradingView, click to enlarge chart)

Since the start of its upside acceleration on 4 May 2023, the USD/CNH has managed to evolve above its 20-day moving average and today’s price action has managed to stage a rebound after a retest on it. If the 20-day moving average now acting as a key intermediate support at 7.2160 is not broken down, the USD/CNH is likely to remain in its short-term bullish trend trajectory which in turn may see further potential weakness in the CSI 300 and Hang Seng indices.

The only catalyst for a potential revival of bullish animal spirits in China equities is a clear signal from China’s State Council on the implementation of new fiscal stimulus measures in terms of scope and timing.

{kind=link}