{kind=link}

Eurozone inflation held firmer than expected in July, with headline CPI steady at 2.0% yoy, defying expectations for a slight dip to 1.9% yoy. Core CPI was unchanged at 2.3% yoy as forecast. Today’s inflation release reinforces the growing expectation that ECB already completed the easing cycle, as the bar for additional easing is increasingly high.

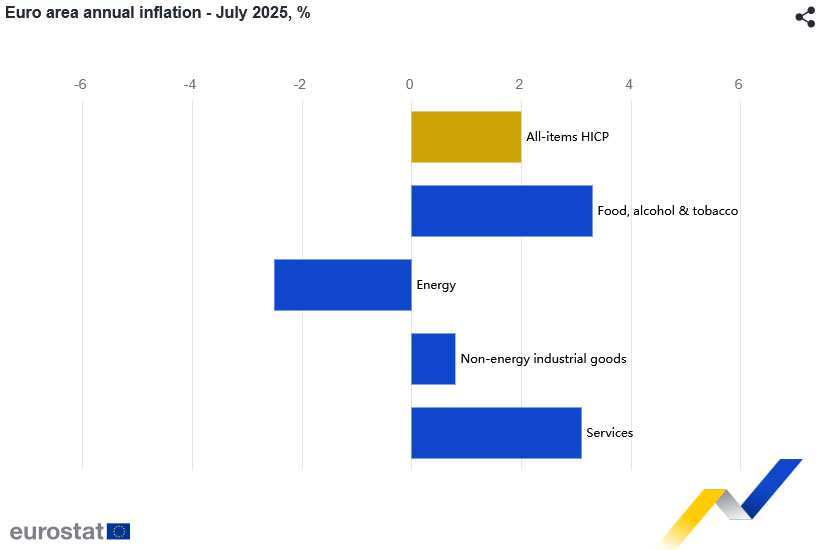

The underlying components show little sign of disinflation picking up momentum. Non-energy industrial goods inflation rose to 0.8% from 0.5%. While energy inflation remained deeply negative at -2.5%, that decline is slowing. Food inflation ticked up slightly from 3.1% to 3.3%. Services inflation eased only modestly from 3.3% to 3.1%.

Swaps now price in less than 50% chance of another rate cut this year. Comments from officials in recent weeks have leaned cautious, citing inflation stabilization at and waning downside risks tied to the global trade environment. The recent breakthrough in US-EU trade negotiations has also removed a key external headwind.

Besides, major banks are shifting their forecasts in line with this view. Deutsche Bank, Goldman Sachs, and BNP Paribas have all walked back expectations for more cuts in 2025.