{kind=link}

Attention in US markets centers on November CPI today, against a backdrop of deteriorating risk sentiment. Despite a slight post-NFP lift in March Fed cut pricing, equities have failed to find support, and risk appetite deteriorated sharply overnight.

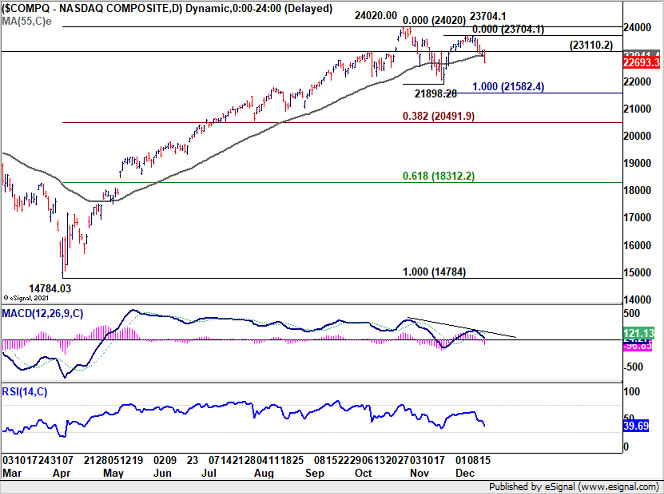

NASDAQ led the downside overnight, breaking decisively below key near-term support and its 55 D EMA. That move shifts the technical picture bearish for the near term and raises the risk of further downside once the CPI event risk passes.

The inflation data itself will be incomplate. The BLS confirmed that the release will omit certain one-month changes due to missing October data after the extended government shutdown. As a result, the CPI print may lack the usual granularity markets rely on for strong directional signals.

Consensus expects headline CPI to tick up to 3.1% yoy, with core CPI holding at 3.0%. Absent a major deviation, Fed expectations should remain broadly stable. A January hold remains the base case, while March cut odds sit near 55%, with three more months of jobs and inflation data still to come.

Technically, NASDAQ’s strong break of 23110.2 suppor as well as 55 D EMA suggests that corrective patternf rom 24020.00 high is now in the third leg. Deeper fall should be seen to 21898.2 support, and possibly below to 100% projection of 24020.0 to 21898.28 from 23704.1 at 21582.4.