{kind=link}

Yen’s inability to stage a meaningful rebound has become a defining feature of late-year trading. Even the BoJ’s December rate hike failed to generate sustained support, highlighting how entrenched the bearish forces have become.

Carry trade dynamics remain central. Nikkei has enjoyed a powerful uptrend this year, helped by optimism surrounding Prime Minister Sanae Takaichi’s new administration and ongoing enthusiasm for AI- and tech-linked stocks, despite persistent valuation concerns.

The scale of the rally has been striking. From levels around 30,000 in April, Nikkei surged to fresh record highs above 50,000 by early November, marking one of its strongest advances in decades. While some jitters have emerged since November, the index has so far held comfortably in a broad range around 50,000. That consolidation suggests underlying momentum remains intact, leaving scope for another leg higher early next year.

At the same time, fiscal concerns are quietly intensifying. Japan’s expansive budget stance has pushed long-dated yields higher. Thirty-year JGB yields remain close to record highs near 3.4%, while 10-year yields hover above the 2% mark, levels not seen in decades. Even so, yields remain artificially suppressed. The crucial context is that the BoJ is still a massive buyer of government bonds in gross terms, effectively capping long-term yields.

As a result, risks that would normally push yields much higher—such as fiscal sustainability concerns—are instead being priced into Yen. That dynamic leaves the currency vulnerable to further downside in the months ahead. Even direct government intervention, should it move beyond verbal warnings, is unlikely to offer lasting relief

Among Yen crosses, AUD/JPY and NZD/JPY are particularly constructive, supported by emerging speculation that RBA and RBNZ could return to rate hikes in early 2027, or even in late 2026.

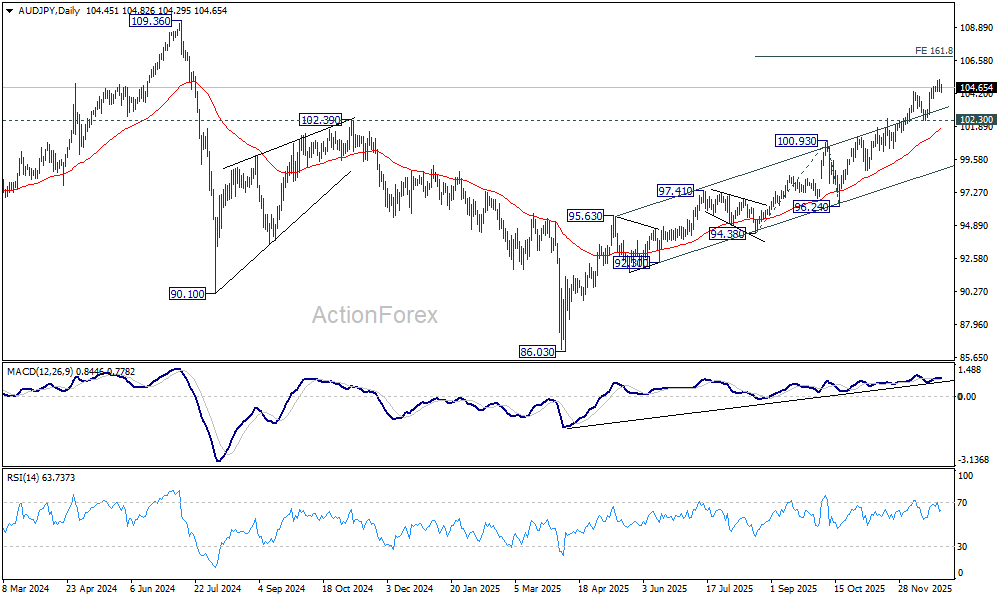

Technically, AUD/JPY’s up trend from 86.03 is still in progress. The strong bounce from prior medium term channel ceiling is a clear bullish signal, which solidifies that it’s in upside acceleration. Outlook will continue to stay bullish as long as 102.30 support holds. Next target is 161.8% projection of 94.38 to 100.93 from 96.24 at 106.83. There is prospect of retesting 109.36 (2024 high) next year if momentum continues.

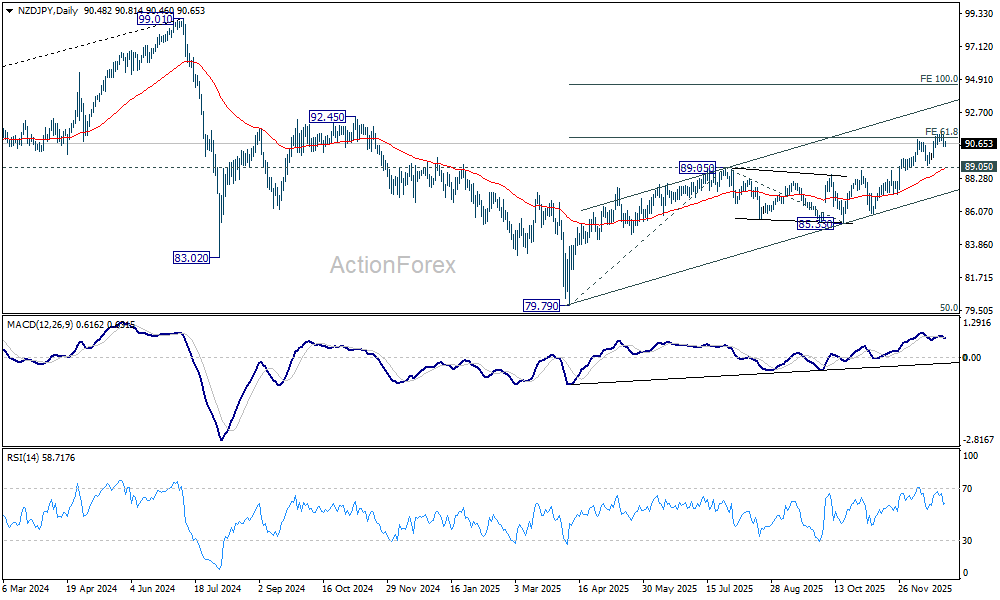

NZD/JPY is underperforming AUD/JPY primarily because RBNZ out-eased RBA much this year. Still, the up trend from 79.79 remains intact and healthy. Near term outlook in NZD/JPY will stay bullish as long as 89.05 resistance turned support holds. Sustained trading above 61.8% projection of 79.79 to 89.05 from 85.33 at 91.05 would likely prompt upside acceleration towards 100% projection at 94.59 next.