{kind=link}

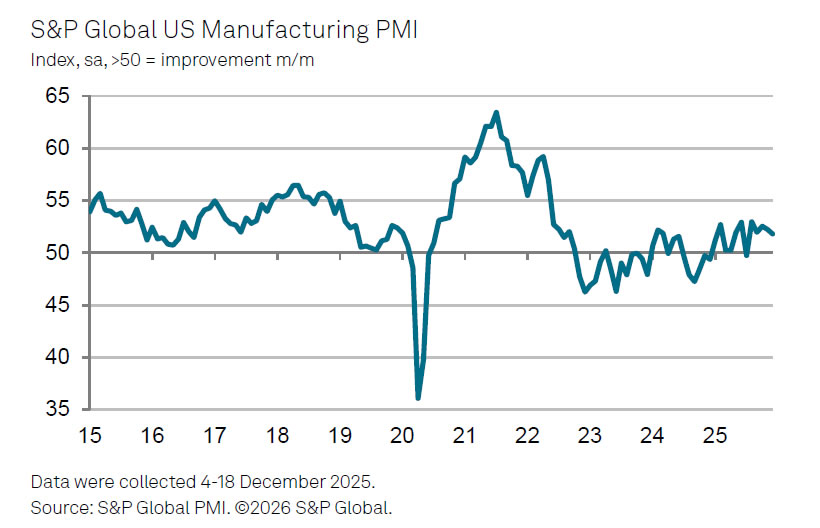

US PMI Manufacturing was finalized at 51.8 in December, easing from November’s 52.2 and marking the weakest expansion in the current five-month growth stretch. While activity remains in growth territory, the slowdown points to fading momentum as the sector heads into 2026.

According to S&P Global Market Intelligence, output continued to rise in December, implying manufacturing still supported solid fourth-quarter growth. However, Chief Business Economist Chris Williamson warned of a “Wile E. Coyote” dynamic: factories are maintaining production even as new orders fall. The gap between output growth and declining orders is now the widest since the 2008–09 financial crisis, raising concerns over sustainability.

Unless demand improves, production is likely to be scaled back, with adverse implications for payrolls. Cost pressures remain a key headwind, as firms continue passing higher tariff-related costs to customers. Input cost inflation did moderate to its lowest since January, suggesting tariff effects peaked last summer, but costs are still rising at an elevated pace relative to other major economies.