The IMF has warned that the global economy faces a more prolonged and damaging shock if the Middle East conflict escalates, with oil prices potentially averaging as high as $125 in 2027 under a severe scenario. Crucially, this is not a short-lived spike but a sustained high-price environment, implying persistent inflation pressure and a more challenging policy backdrop.

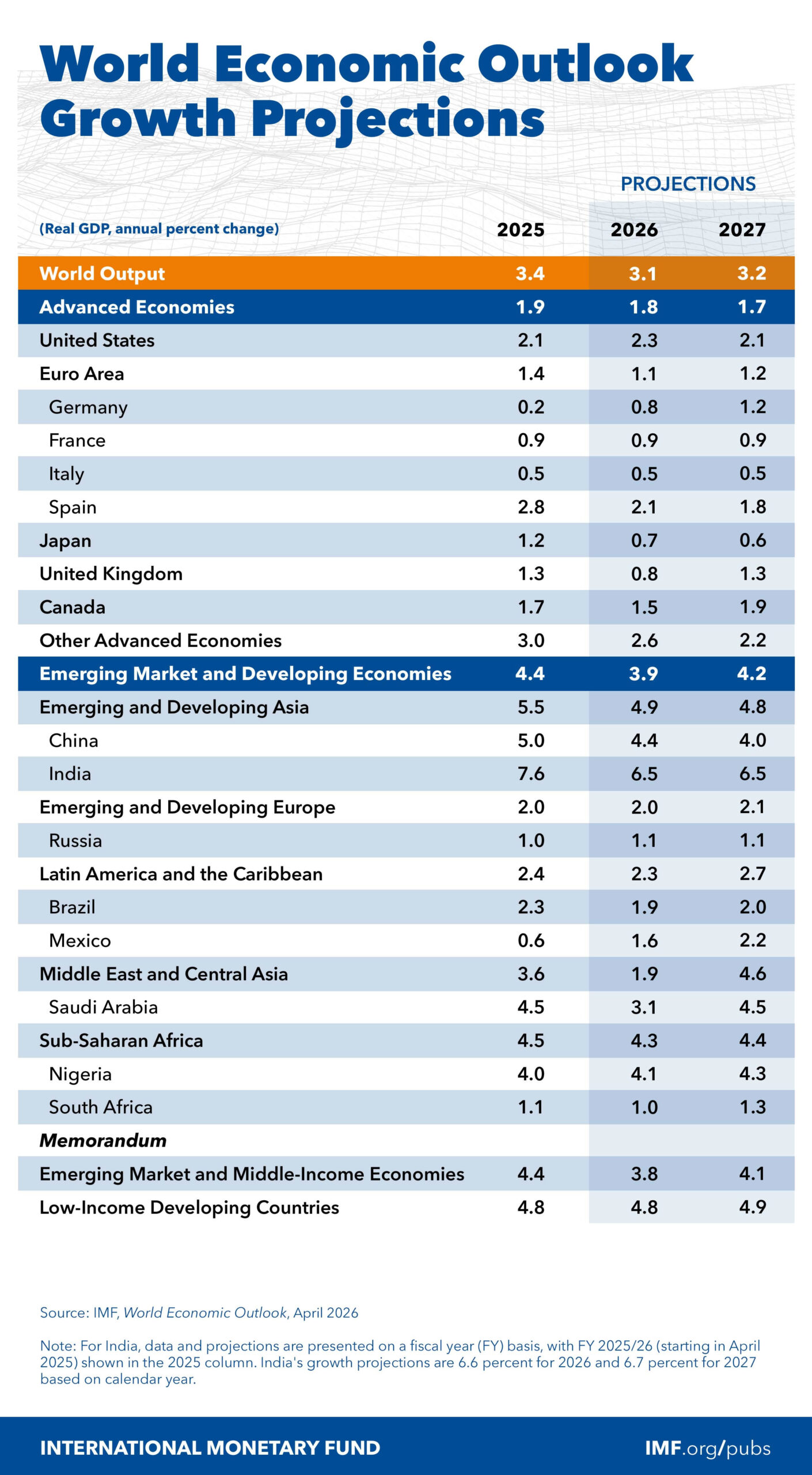

Under its baseline assumption that the conflict remains limited, the IMF projects global growth to slow to 3.1% in 2026 before edging up to 3.2% in 2027. Inflation is expected to rise modestly in 2026 due to energy costs before resuming its decline. However, even this relatively benign scenario points to a fragile balance between slowing growth and lingering price pressures.

The severe scenario paints a much more concerning picture. Oil prices are projected to double relative to earlier assumptions and remain elevated, averaging around $110 in 2026 and $125 in 2027. At the same time, global headline inflation could climb to 5.8% in 2026 and exceed 6% in 2027, reflecting both higher energy costs and a rise in inflation expectations.

| IMF Scenario | 2026 | 2027 |

| REFERENCE FORECAST | ||

| Global GDP growth | 3.1% | 3.2% |

| Oil price average | $82 | $75 |

| Headline inflation | 4.4% | 3.7% |

| ADVERSE SCENARIO | ||

| Global GDP growth | 2.5% | 3.0% |

| Oil price average | $100 | $75 |

| Headline inflation | 5.4% | 3.9% |

| SEVERE SCENARIO | ||

| Global GDP growth | 2.0% | 2.2% |

| Oil price average | $110 | $125 |

| Headline inflation | 5.80% | 6.10% |

That rise in expectations is a key transmission channel. The IMF estimates that one-year-ahead inflation expectations could increase by up to 100 basis points in advanced economies and 130 basis points in emerging markets. This would reinforce price pressures and make it more difficult for central banks to bring inflation back under control.

Financial conditions would also tighten significantly. The IMF warned of a broad risk-off episode, with corporate credit spreads in advanced economies and China widening by around 100 basis points, while emerging markets could see sovereign spreads rise by a similar magnitude and corporate spreads by as much as 200 basis points.

Importantly, policy responses in such a scenario would be constrained. Rather than supporting growth, central banks would be forced to focus on containing inflation, even as activity weakens. This creates a classic stagflationary setup, where tightening financial conditions and elevated borrowing costs further weigh on economic momentum.

Even in the IMF’s adverse scenario, growth slows meaningfully to 2.5% in 2026, with oil averaging around $100 and inflation rising to 5.4%. This underscores that risks are already skewed to the downside, even without a full escalation.

{kind=link}