{kind=link}

Sunrise Market Commentary

- Rates: Core bonds under pressure despite tech correction

Core bonds lost ground yesterday despite the tech correction. Today’s eco data won’t be of main importance, but the risk-sentiment as reflected by the fate of equities and oil (OPEC meeting) might play a bigger role. We stick to a sell-on upticks strategy for core bonds. - Currencies: dollar faces mixed signals. Sterling extends Brexit rebound

Yesterday, the dollar initially profited from progress on a US tax bill and positive comments from Yellen. However, the rebound ran into resistance as tech stocks were sold. Today, the dollar will probably faces conflicting drivers. A further risk-off correction might prevent further USD gains. Sterling continues to profit from a positive Brexit momentum

The Sunrise Headlines

- The Nasdaq ended the US session down 1.3% as major tech stocks that have outperformed this year retreated sharply. The S&P 500 technology stocks segment slid 2.6%, while financials rose 1.8%, leading to a flat close for the S&P. Asian equities trade fairly weak with only Japan remaining in the black

- The alliance between OPEC (Saudi-Arabia) and Russia faces its first big test, with Saudi Arabia still waiting on a commitment from Russia to back an extension of output cuts throughout 2018, as OPEC meets today. Brent stabilizes.

- China’s manufacturing sector picked up unexpectedly in November as construction growth rose markedly. The official manufacturing PMI rose to 51.8 in November, easily besting consensus (51.4). Services PMI improved too.

- The pound strengthened to a two-month high on Thursday driven by hopes the UK had reached an agreement over a divorce payment to the EU and reports that a deal over the Northern Ireland border was close to a breakthrough

- Australia’s big four banks fell after the government announced a public inquiry into the country’s banking and financial system.

- The Bank of Korea has raised interest rates (25 bps to 1.5%) for the first time in more than six years, heralding the start of a tightening cycle. Decision wasn’t unanimous and comments soft. The won lost ground and yields fell on profit taking after strong anticipation.

- Japan’s industrial production returned to growth in October but grew at a slower pace than forecast. The 0.5% M/M increase fell short of the 1.9% M/M consensus. Y/Y, output was still up a strong 5.9%.

Currencies: Dollar Faces Mixed Signals. Sterling Extends Brexit Rebound

EMU and US inflation to guide FX trading?

Yesterday, the dollar gained slightly more ground as the progress on a US tax bill caused some USD shorts to reduce exposure. Yellen holding a positive tone at a Congressional hearing was also slightly USD supportive. At the same time, sentiment on risk deteriorated. The dollar received some breathing space as its traded off its recent lows. However, the technical picture didn’t really improve. EUR/USD closed the session at 1.1847. USD/JPY finished the session at 111.93.

Overnight, Asian equities trade with substantial losses as tech shares suffer from the Nasdaq correction yesterday. The November China PMI (both manufacturing and services) improved further, but doesn’t help sentiment. The Bank of Korea raised its policy rate by 25 bps, but the won declined as BOK comments remained soft. Japanese equities decouple from the broader correction supported by yesterday’s USD/JPY rebound. The pair trades in the 112 area. The kiwi dollar lost more than half a big figure as consumer confidence declined sharply. NZD/USD trades in the mid 0.68 area. EUR/USD shows no clear trend and trades in the 1.1860 area.

Today, the November EMU CPI is interesting. The consensus expects a rise from 1.4% to 1.6% (1.0% from 0.9 % for the core). We see a slight upward risk. German and EMU labour market data are interesting too, but no market movers. In the US, investors will keep a close eye at spending and income data. Especially the price deflators have market moving potential in case of the deviation from consensus. A modest rise of 0.1% (headline) and 0.2% (core deflator) is expected. The Chicago PM is expected to ease slightly from 66.2 to 63 after a sharp rise last month. The data might be mixed to slightly euro supportive. However, there is still plenty of event risk that might affect USD trading. The debate on the US tax bill (and the debt ceiling) are potential sources of market volatility (in both directions). We also keep a close eye at the stock market performance. Of late, the dollar often suffered more from a risk-off correction than the euro as US yields declined more than European ones. For now, the dollar holds up rather well given the correction in tech stocks (so do US bond yields) . However, the balance remains fragile

Earlier this week, we were cautious on a sustained USD rebound as markets still question the Fed’s rate hike intentions beyond December. Yellen remained optimistic on the economy. It helped to put a floor for the dollar, but nothing more than that. Today’s news flow might be uite diffuse (cfr supra). A big beat in the PCE deflators would be a USD supportive, but we don’t expect that to happen. Stronger (price) data or other positive events (tax cuts) are still needed for markets to reconsider a more USD positive scenario. Over the previous days price action was a bit more USD constructive, but not good enough to qualify it as a U-turn. We stay dollar neutral.

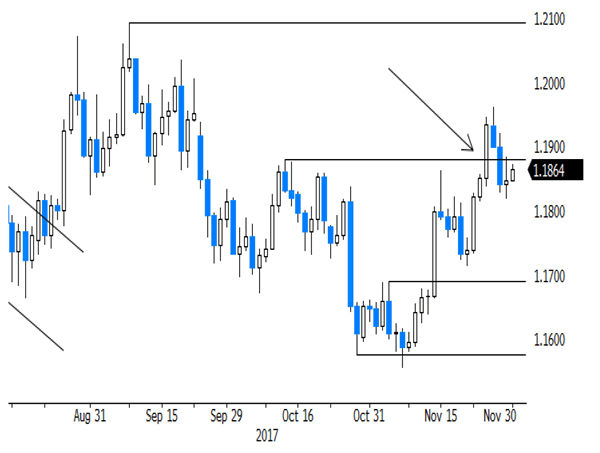

From a technical point of view, EUR/USD set a post-ECB low mid-November, but on Friday regained the 1.1880 MT correction top. This break opened the way for a full retracement to the 1.2092 top. A return below 1.1713 would signal that the rebound in EUR/USD is aborted. For now there is no clear technical signal. The USD/JPY momentum deteriorated this month. Last week, USD/JPY dropped below the 111.65 neckline. There was no aggressive follow-through selling but if confirmed, the break would make the picture USD negative.

EUR/USD: rally aborted, but no clear correction signal

EUR/GBP

Sterling extends ‘Brexit rebound’

Yesterday, sterling kept a cautiously positive bias, building on Wednesday’s gains. The preliminary EU/UK agreement on a divorce bill raised chances that negotiations on the future relationship start after the December EU summit. Ireland’s EU commissioner also suggested that a break-through on the issue of the Irish border could follow soon. EUR/GBP finished the session at 0.8835. Cable closed the session at 1.3409, confirming the technical break beyond 1.3350.

Overnight, UK consumer confidence declined from -10 to -12. However, sterling remains well bid on press headlines that the UK and Ireland are making progress on the issue of the Irish border. Later today, there are no important eco data in the UK. The is no formal decision on further Brexit talks yet, but there is apparently good progress. Markets will probably continue adapt positions for the December EU summit to give the green light for talks on the future relationship. Sterling might make some further progress.

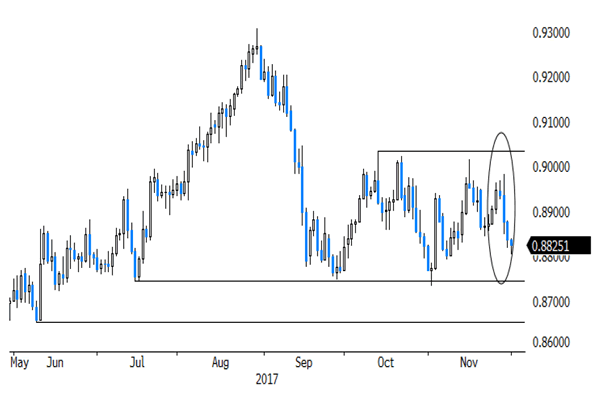

MT view/technical picture. A BoE driven sterling rebound ran into resistance early this month. Sterling declined again as markets anticipated that the rate cycle would be very gradual and limited. EUR/GBP trades in a 0.8733/0.9033 consolidation range. Brexit headlines cause day-to-day gyrations. We changed our ST bias on EUR/GBP from positive to neutral two weeks ago. The 0.9015/33 area might be tough to break short-term. In case of more positive news on Brexit, return action to the 0.8733 (or below) level is possible ST.

EUR/GBP: returning south in the consolidation pattern on positive Brexit headlines