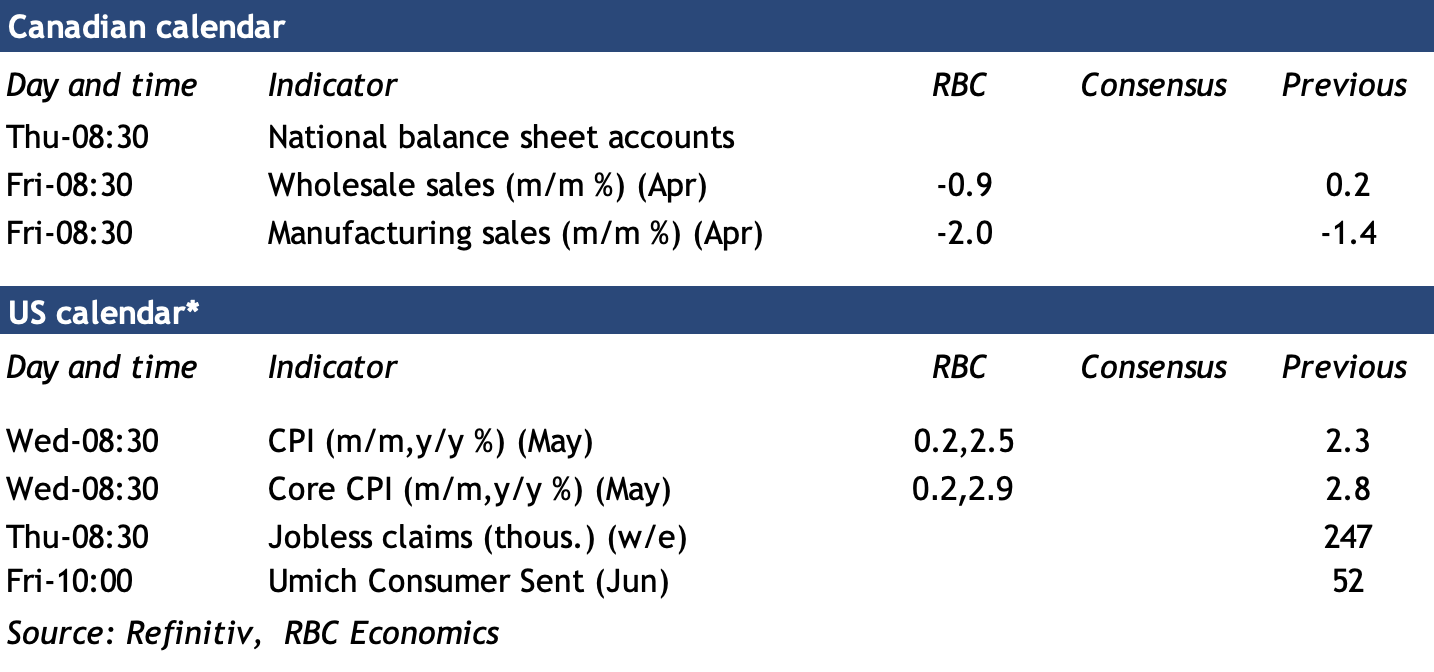

Summary

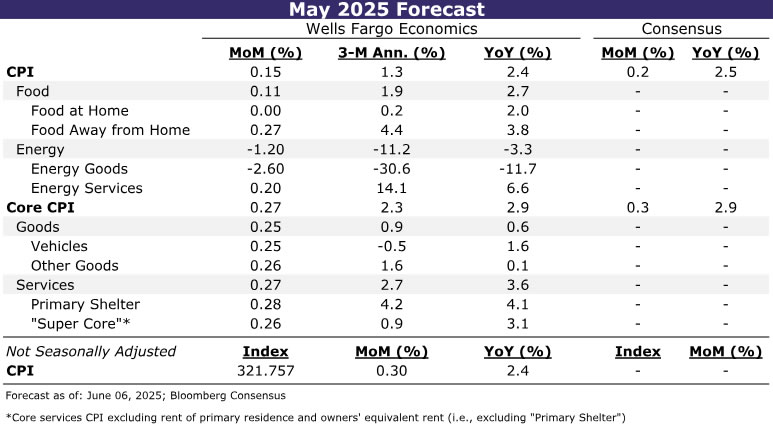

May’s CPI report will be an important test of the speed and magnitude to which higher tariff rates are being passed along to the consumer. We expect to see only a moderate advance in headline CPI (0.15%) in May as gasoline prices fell on a seasonally adjusted basis and food inflation appeared tame. But excluding food and energy, inflation looks to have firmed on the back of higher goods prices. We estimate the core CPI rose 0.27% in May.

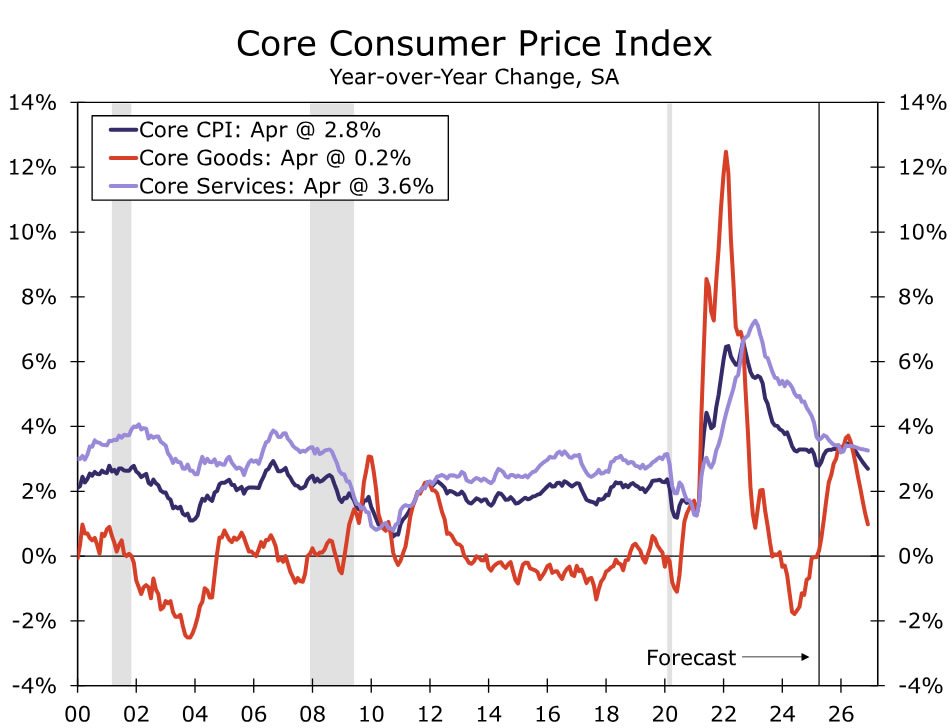

Front-loading of inventories and efforts to avoid alienating customers—especially as it remains to be seen where tariff rates eventually land—are mitigating the early effects of higher import duties on consumer prices. That said, we expect to see the inflationary effects ramp up more in the coming months as the higher tariff environment persists. We estimate core CPI will advance at an average monthly pace of 0.30% in the second half of the year, which would push the year-over-year rate back up to 3.3% in Q4 from April’s year-over-year rate of 2.8%.

The Rebound Begins

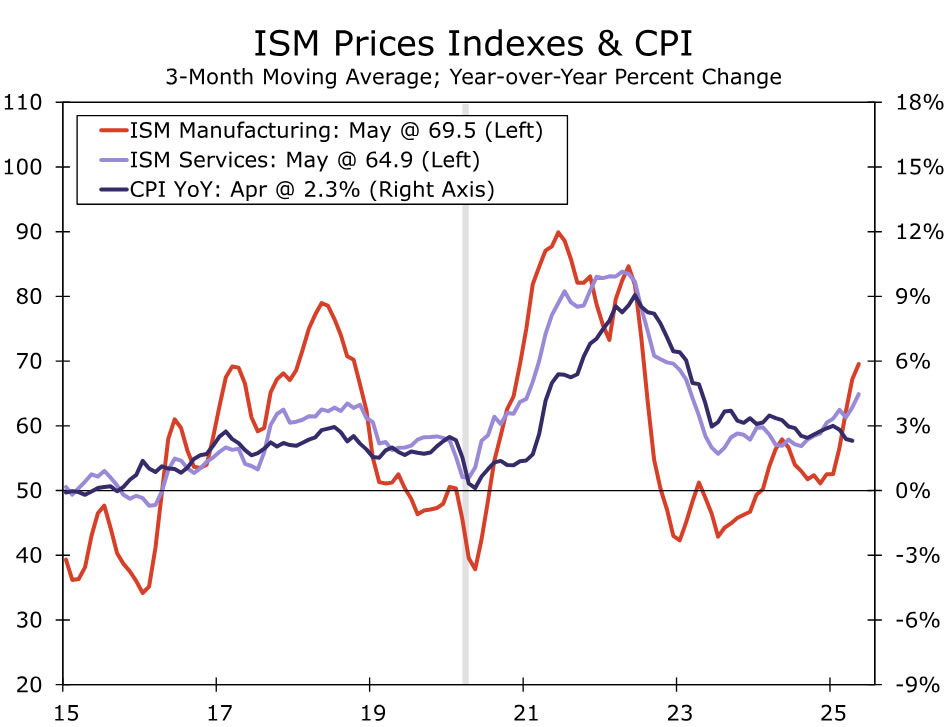

The May CPI report will test whether April’s potential signs of tariffs were early glimmers of inflation effects to come or more typical monthly noise. We estimate consumer prices rose 0.2% (0.15% unrounded), in line with the current Bloomberg consensus. If realized, the increase would push up the year-over-year rate up a tenth to 2.4% and follow soft data in showing that the downward trend in inflation is beginning to reverse (Figure 1). Core categories are expected to drive the advance. Excluding food and energy, we estimate prices increased 0.3% (0.27% unrounded) in May and 2.9% over the past year.

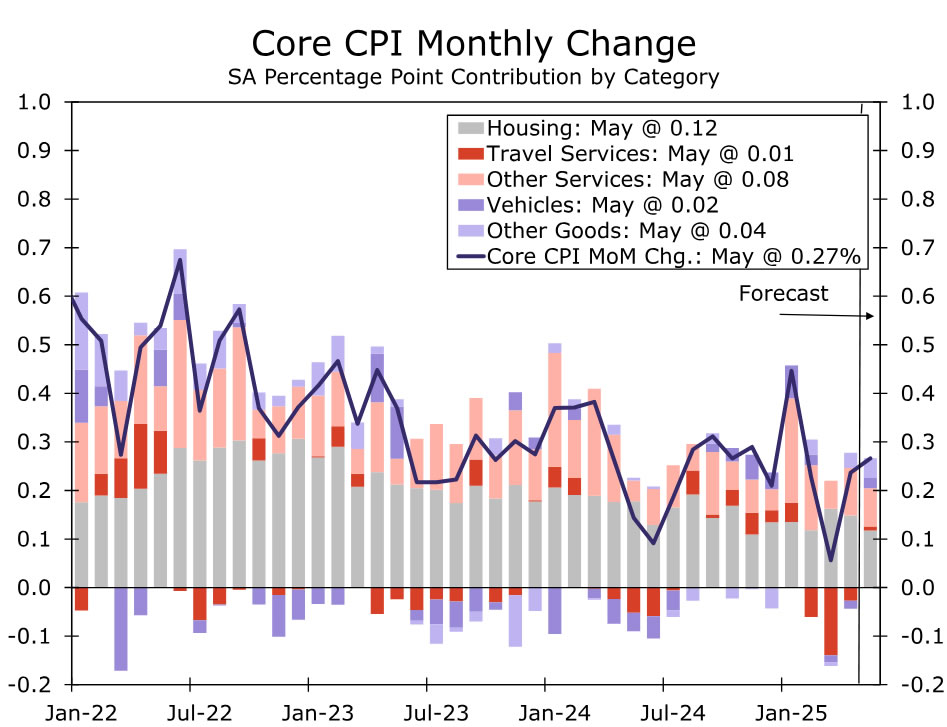

Last month’s CPI report showed a modest (0.1%) rise in core goods prices, as a drop in vehicle prices was more than offset by a rise in other core goods categories. Core goods ex-new and used autos matched its largest monthly rise in more than a year in April, with notable strength among household, recreational and IT goods. Whether these categories deliver a repeat performance will help to determine if higher import duties are indeed being passed on to consumers, or if April’s strength was merely a function of volatility in the data. The risk of the latter seems higher than usual, as the BLS noted it temporarily reduced data collections in April due to staffing shortages. But the jump in tariff rates over the past few months—collections are up 80% year-to-date through June 4—generates significant potential for April’s strength to continue. We expect to see core goods prices rise about 0.25%, with similarly sized gains in vehicles and remaining core goods.

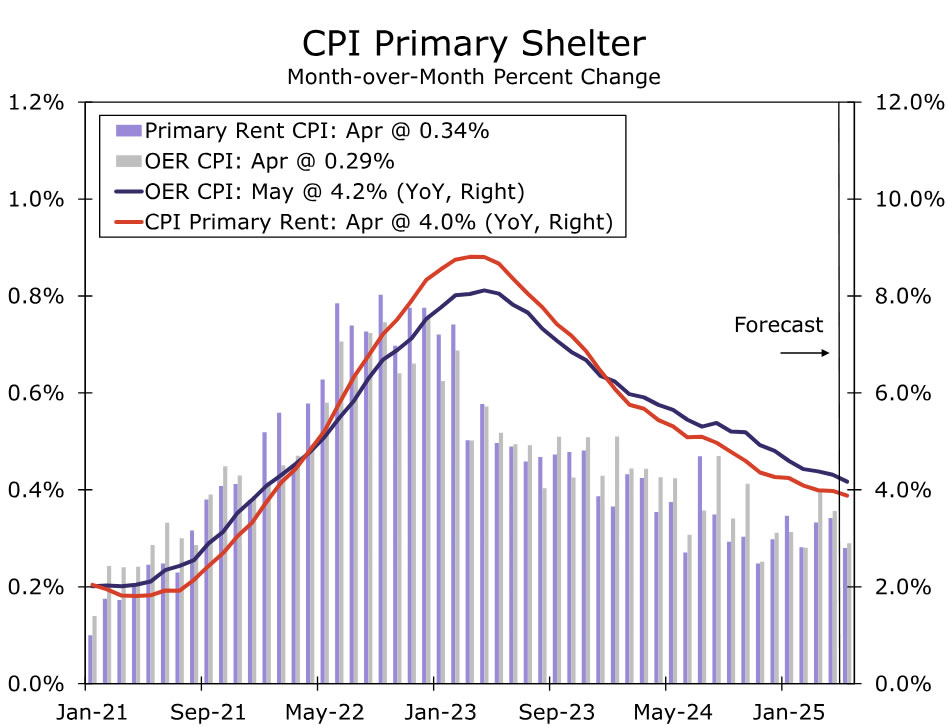

While the changing trade policy environment has put goods inflation back in the spotlight, service-sector disinflation slowly continues. We estimate core services inflation was little changed in May, with a 0.3% monthly increase keeping the year-ago rate at 3.6%. Beneath the steady monthly gain, the drivers are likely to shift. Primary shelter inflation is anticipated to moderate after a couple of months of above-trend gains (Figure 3). But travel-related services prices should rise slightly in May after falling sharply the past three months. Although recent weakness in travel categories highlights more cautious spending by consumers, we expect to see a modest lift in prices amid the early timing of Memorial Day.

Consumers look to have gotten a bit more breathing room when it came to gas prices last month, however. We estimate energy prices declined a little more than 1% last month. Along with a roughly 0.1% rise in food prices, this leads us to expect headline inflation will rise less than the core index in May.

While May’s Consumer Price Index is not expected to deliver a stand-out increase, we look for inflation to pick up through the second half of the year. Higher tariff rates lie behind the expected uptrend. In our view, the administration remains committed to meaningfully higher import duties despite the current pause on “reciprocal” tariffs and legal challenges of the current section of the Trade Act used to employ them. Pre-tariff inventory building and hope that the current scale of tariffs may be reduced have helped to restrain cost increases thus far. Consumer-facing companies in particular seem hesitant to immediately pass on the full costs of tariffs due to concerns about the underlying strength of low- and middle-income households. As a result, we expect some of the tariff costs to be absorbed via margins, which remain noticeably higher than before the 2018 trade war. That said, as the higher tariff regime persists, shielding consumers from the costs is likely to become more challenging. We anticipate the three-month annualized rate of core goods inflation to peak around 4%-5% in early fall, a little lower and later than our previous forecast published May 8 ahead of the 90-day pause on “reciprocal” tariffs on China.

Yet, spillovers into the service sector are still expected to be limited. The jobs market is no longer experiencing historic labor shortages, and the weakening backdrop for workers points to employment cost growth slowing further this year. The monthly pace of shelter inflation is close to settling to around a 0.28%-0.30% monthly pace over the remainder of the year, which should help to drive the current year-over-year rate of 4.2% down to 3.6% next spring. Meantime, service providers face the same concerns as companies directly impacted by tariffs about consumers’ ability and willingness to spend. As a result, we look for services inflation to recede a bit more throughout the year and to mitigate the increase to goods inflation fueled by tariffs.

in May as gasoline prices fell on a seasonally adjusted basis and food inflation appeared tame. But excluding food and energy, inflation looks to have firmed on the back of higher goods prices. We estimate the core CPI rose 0.27% in May.){kind=link}