Month-end flows notably influenced the session, leading to another instance of US Dollar underperformance. Equity markets, while ending the month on a positive note, experienced significant volatility into the close, as major participants leveraged the typically higher liquidity around monthly settlement prices for portfolio rebalancing.

Global indices are now closing above their early 2025 highs, completing what has been a volatile yet ultimately successful month of June.

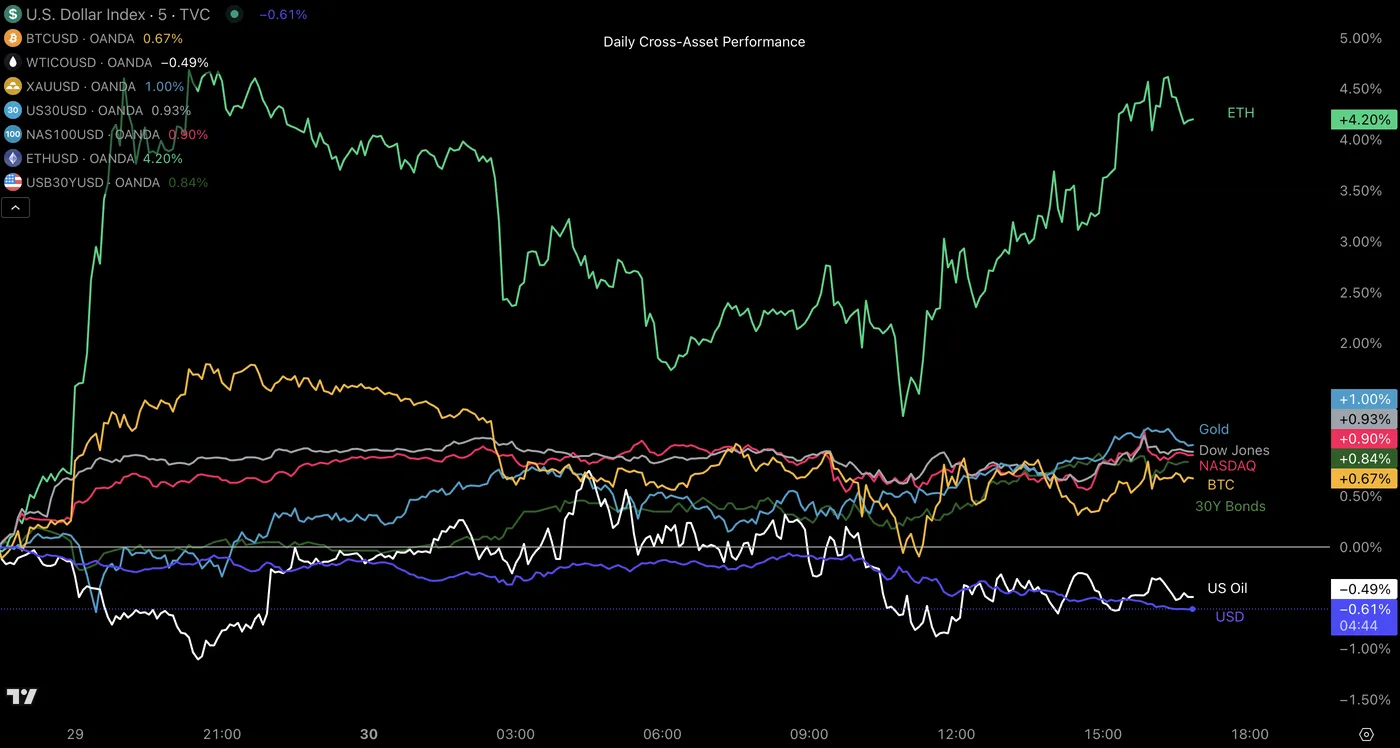

Commodities observed a mixed performance today. Oil and other energy products saw declines, while Gold staged a notable rally throughout the session, closing just above the key $3,300 mark.

The broader macroeconomic landscape remained relatively calm. However, renewed tensions have emerged in Iran, and we will provide further analysis should the situation escalate.

Daily Cross-Asset performance

Cross-Asset Daily Performance, June 30, 2025 – Source: TradingView

Ethereum is the standout performer on the session – Monitor the performance of the second biggest crypto in July as digital assets tend to perform well in the month starting tomorrow.

A picture of today’s performance for major currencies

Currency Performance, June 30 – Source: OANDA Labs

The story repeats again in today’s month-end flows – The US Dollar lagged again and Pacific currencies (NZD and AUD) are on top of majors.

Tomorrow’s asset performance will be essential to monitor in order to see what markets are cooking for the upcoming month.

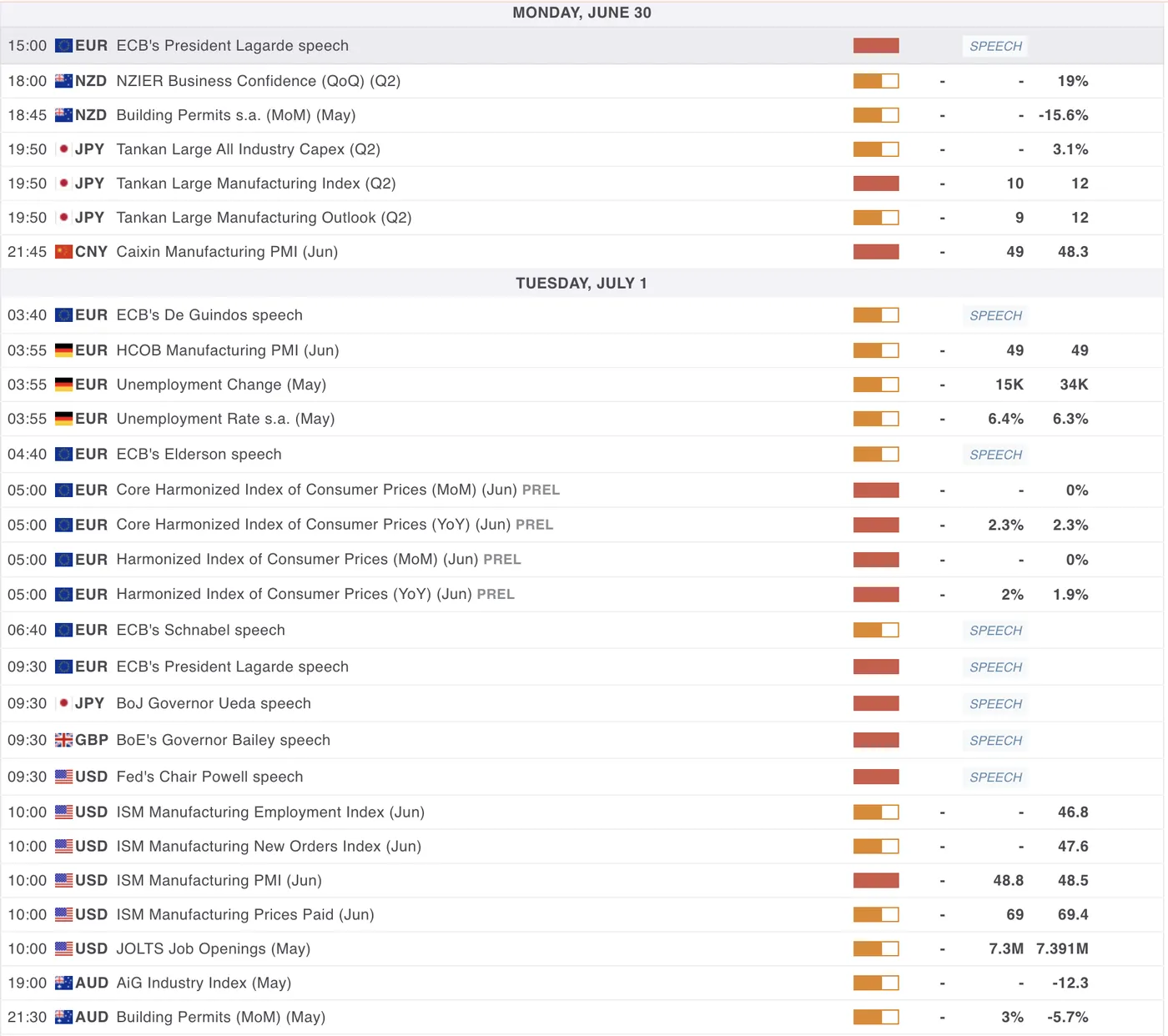

A look at Economic Data releasing in tonight and tomorrow’s session

For all Market moving events, check the MarketPulse Economic Calendar

The overnight/tomorrow session will see more economic data releases, mostly with the US PMIs giving more clarity on the current economic picture for the US.

The ISM Manufacturing PMI is releasing tomorrow at 10:00 A.M. ET, expected at 48.8. The less market moving Chicago PMI came at a fairly big downward surprise with 40.3 vs 43 expected, markets may be preparing for some surprise in tomorrow’s release.

Elsewhere, markets are awaiting for the Caixin PMI release from China tonight 21:45 (exp 49), which could be market moving particularly for APAC Currencies and Equity markets around the globe that have been performing quite dominantly in the past month.

For Euro traders, get ready for the Eurozone Inflation data release at 5:00 in the overnight session – We will have more clarity if the ECB has more work to do on their Monetary Policy or if the pause gets confirmed further.

Safe Trades!

{kind=link}