Overview

The winter of discontent has descended on the New Zealand economy since May. In some respects, business and consumer sentiment has soured, raising questions on exactly when the long-awaited pickup in the economy will become broader based and more sustainable. Parts of the economy are doing well and there is exuberance in the primary sector who are receiving the best returns seen for several years. The Government’s new “Investment Boost” policy might well bring forward some investment in some quarters.

Outside of New Zealand, the trade war has continued to progress – but the degree of heat in the battle has been much lower than feared a few months ago as countries have largely chosen to deal as opposed to fight. Global growth forecasts have picked up as some of the worstcase scenarios have been discounted. Nevertheless, there is still water to go under the bridge as the details of some deals done are unclear, and negotiations continue between the US and some trading partners.

Inflation remains too high, but the economy still has significant excess capacity. Hence there are divergent pressures on the Monetary Policy Committee as they chart the way forward.

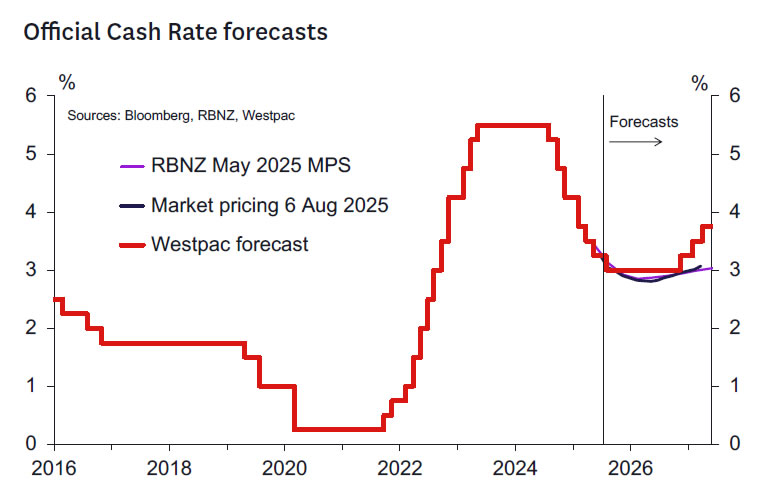

Against this backdrop, we expect the RBNZ will deliver another 25bp rate cut at this month’s policy review. It’s unlikely that the RBNZ will call time on the easing cycle just yet as the economy is yet to decisively and sustainably turn.

With all that in mind, in this note we explore some of the hawkish and dovish arguments that might shape discussion regarding the outlook for policy over the coming months.

The Hawk’s Eye View.

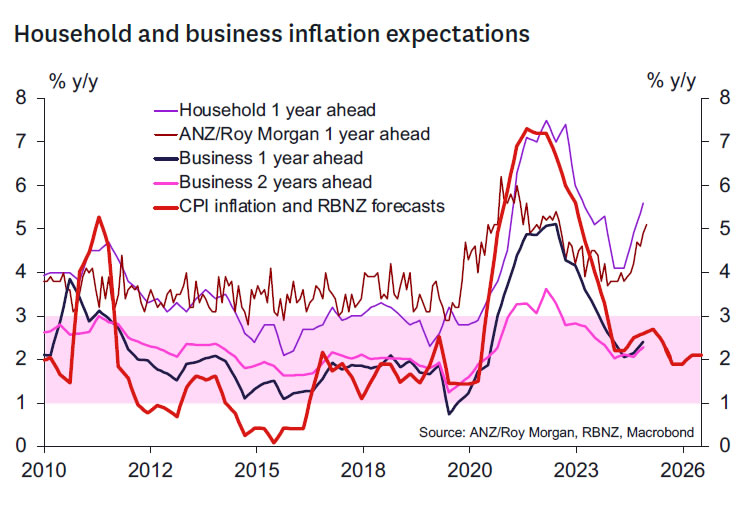

Inflation has increased to 2.7% and looks set to reach 3% in the next couple of quarters. Easing further in this context would be unwise.

- A short-term increase in inflation might not be of concern if there is significant excess capacity in the economy. But inflation might not fall back either significantly or quickly, given that the rise in inflation in recent quarters was not envisaged when the easing cycle began a year ago.

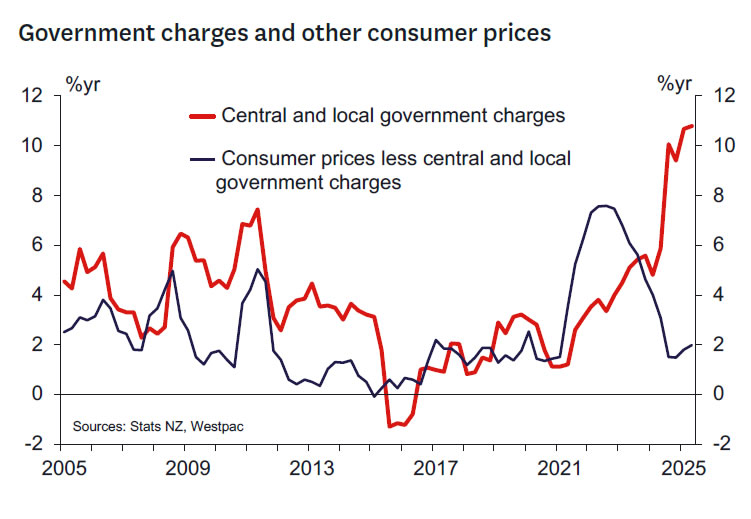

- It’s possible that large increases in a range of administered costs, like rates and electricity charges, will continue as there are ongoing cost pressures in those sectors. If correct, then non-tradables inflation and total inflation will only fall slowly.

- Future cost shocks could boost inflation from an elevated level.

- Inflation expectations are already rising and could impede any sustained fall in inflation to 2%.

The lagged impact of past easing is yet to fully work its way through.

- It is too soon to judge the impact of the OCR easing since August last year. While the OCR has declined by 225bps already, only half of the expected easing in mortgage rates has passed through to the rates paid by households.

- As households continue to refinance, the effective mortgage rate will continue to decline, further stimulating spending.

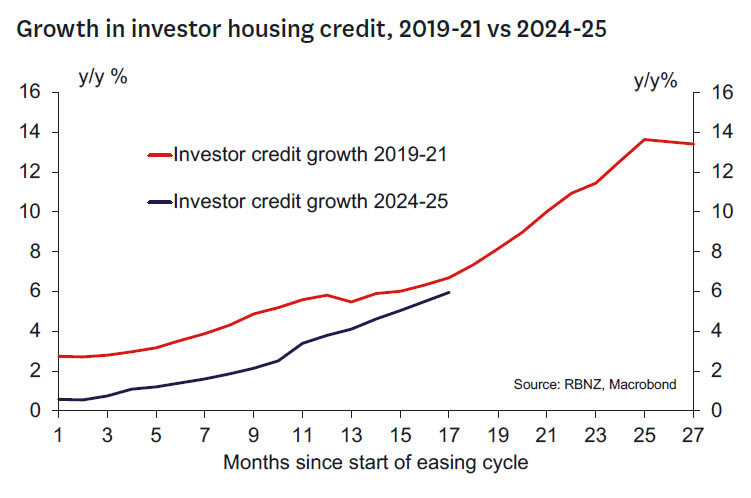

- Housing market investors are already responding to easy financial conditions and are scaling up investment. So far investor demand is not driving prices higher as the housing supply response has been significant. But supply has recovered to 2015 levels now and may be progressively eroded as demand continues, boosting prices as time goes on. We don’t want a repeat of the 2020-21 experience.

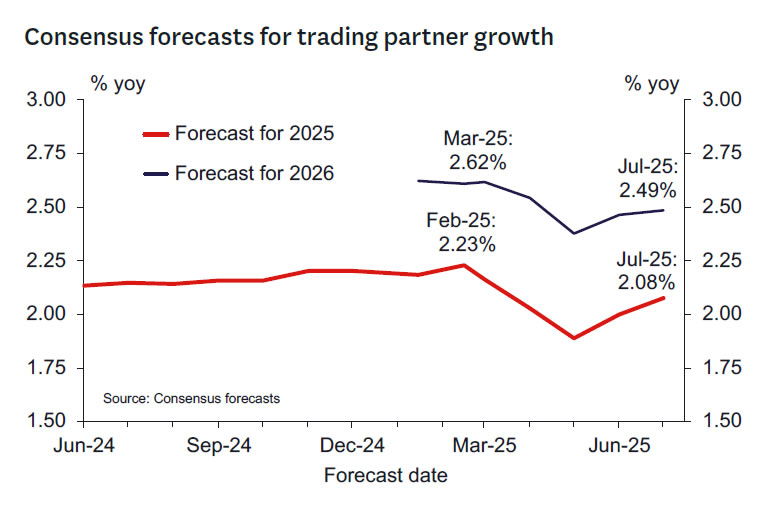

The downside risks for global growth are receding and are less uncertain. Much of the case for additional easing in the April and May meetings rested on a weaker global economy.

- While increases in US tariffs will dampen global growth to a degree, they’re not likely to be the significant drag that was initially feared.

- Forecasts for global growth have been scaled back up as uncertainty has reduced. Consensus and IMF forecasts for global growth are only modestly lower than pre-April levels.

- The Chinese economic outlook seems firmer as policy stimulus is expected to support the economy.

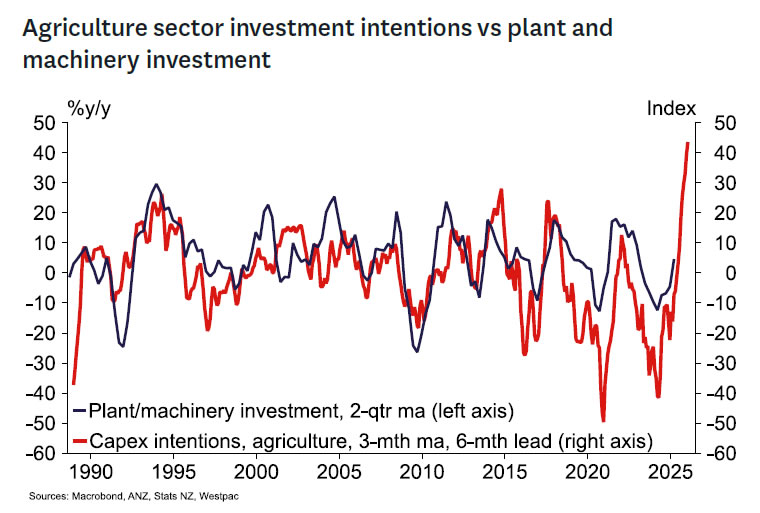

- Prices for our key agricultural exports remain firm. That’s already boosting incomes and spending in rural regions.

The Government’s Investment Boost policy will partially offset downside risks to the growth outlook.

- The Budget included a very generous incentive for firms looking to invest in plant and equipment.

- It’s likely that the agriculture sector will take this golden opportunity with both hands given income levels are so strong.

- Credit growth in the agriculture sector has scaled up significantly as farmers have confidence to do sorely needed investment.

- The tractors are piling up on the dock as dealers scramble to meet orders.

The Dove’s Tale.

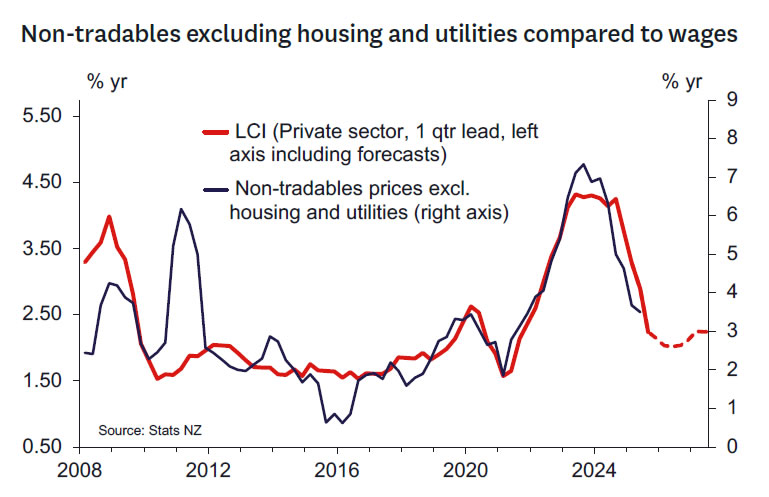

- While non-core items like food have pushed inflation higher, medium-term inflation pressures are contained and indeed continue to weaken.

- Non-tradables inflation outside of the government sector is trending lower and already at or below average levels.

- Businesses in interest rate sensitive sectors like construction are reporting pressure on margins.

- Provided that inflation is expected to remain comfortably within the 1-3% target over the medium term, the RBNZ should use the flexibility provided by the Remit rather than try to fully offset “excess” inflation in the local government sector by forcing further disinflation in the private sector.

Monetary policy needs to be clearly stimulatory to drive the period of above-trend growth needed to absorb spare capacity.

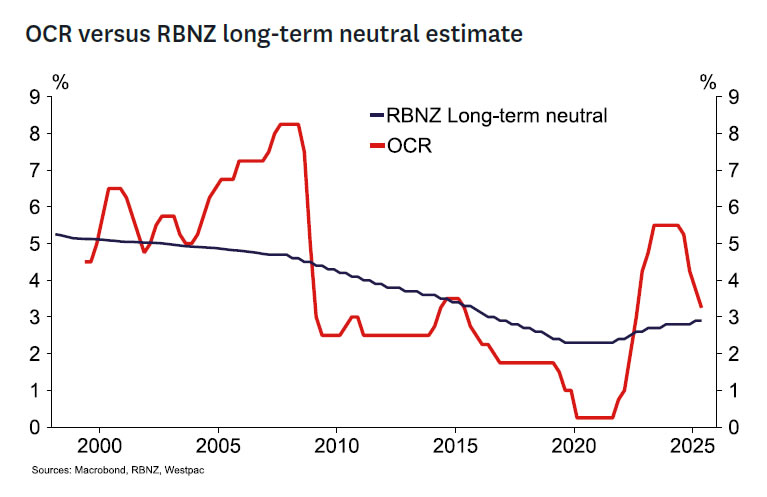

- The RBNZ’s best unbiased estimate is that the longrun neutral OCR is around 3.0% – still below the current OCR.

- Returning the OCR to broadly neutral levels is allowing the economy to grow again. However, until the OCR is moved to a clearly stimulatory level, growth is unlikely to reach the pace required to absorb existing spare capacity in the economy. Historically, outside of crises, the OCR has usually troughed around 50-100bp lower than neutral

- This is especially so with fiscal policy tightening to address the current structural fiscal deficit.

Demand for labour remains especially weak suggesting that the unemployment rate could continue to rise for a while yet.

- Employment fell 0.1% q/q in the June quarter, compared with the 0.2% growth forecast by the RBNZ in May, and the unemployment rate rose to 5.2%.

- Job advertising is yet to turn higher. Firms may be extracting greater productivity gains from their existing labour force, delaying the upturn in hiring.

- If current trends continue, the unemployment rate will continue to rise, thus exceeding the peak forecast in the May MPS (and potentially earlier forecasts that the unemployment rate would peak as high as 5.4%).

- A prolonged period of above-trend unemployment means that wage growth could fall further putting additional downward pressure on non- tradables inflation.

While uncertainty has declined, US trade policy continues to pose downside risks to NZ growth and inflation.

- Confirmation that New Zealand will face a 15% tariff on exports to the US has reduced uncertainty but is clearly unwelcome news for exporters.

- While uncertainty about the size of tariffs faced by key trading partners has reduced, it’s still high, which may restrain households and businesses from consuming and investing and delay the recovery.

- As the economy already has significant spare capacity, there’s room to ease further to insure against the risk of unexpectedly weak economic outcomes.

{kind=link}