Asia Market Wrap – Japan, China Data, Stocks Steady

Hong Kong stocks fell 1.2% after data showed China’s economy slowed in July, with weak factory activity and retail sales. This suggests Donald Trump’s trade war is affecting the world’s second-largest economy. Meanwhile, Japanese stocks rose 1% as the country’s economy grew faster than expected last quarter.

MSCI’s broad Asia-Pacific index (outside Japan) dropped 0.2%. Japan’s Nikkei 225 bounced back 1.6%, nearing a record high after a big drop on Thursday, which ended its six-day winning streak. Australian stocks rose 0.7%, while Hong Kong stocks fell 1.1%.

China’s CSI 300 index went up 0.8% after weaker-than-expected July economic data, like retail sales and industrial production, raised hopes for new government stimulus. Markets in India and South Korea are closed for holidays.

Earlier, hopes for US monetary easing had boosted market confidence, with traders expecting a quarter-point rate cut. However, US wholesale inflation rose in July at its fastest pace in three years, causing traders to lower the chances of a September rate cut to 90%, down from being fully certain before.

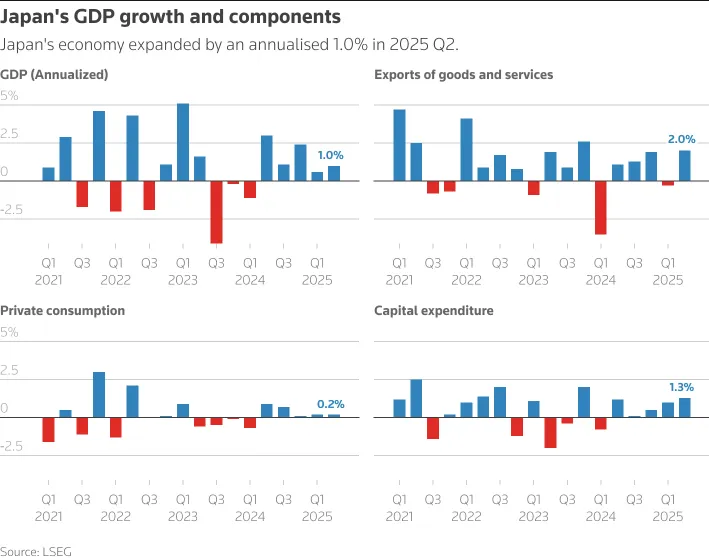

Japan GDP Posts Upside Surprise

Japan’s economy grew faster than expected in the second quarter, with GDP rising 1.0% annually, marking five straight quarters of growth. This was supported by strong exports and capital spending, despite US tariffs. The growth beat market expectations of 0.4% and followed a revised 0.6% rise in the previous quarter.

Source: LSEG

However, analysts warn that US tariffs and global uncertainties could hurt Japan’s economy in the coming months, especially for automakers trying to keep prices low for US customers.

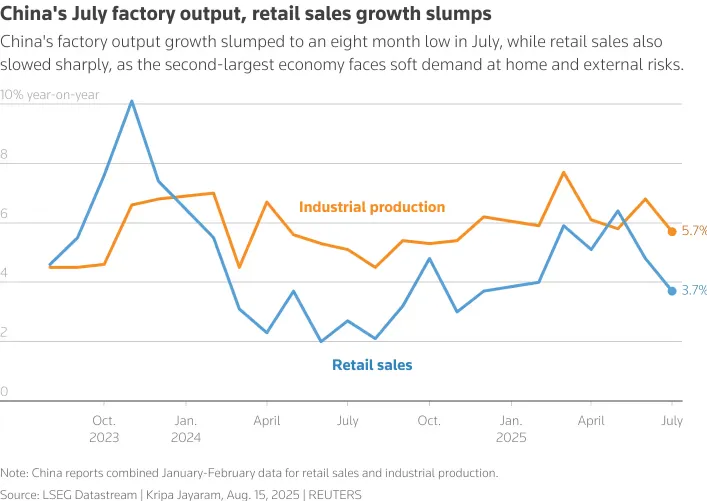

China Data Disappoints as Factory Output and Retail Sales Slump

China’s factory output growth hit an eight-month low in July, and retail sales slowed sharply, increasing pressure on policymakers to boost the $19 trillion economy with more stimulus.

Challenges include US trade policies, extreme weather, tough domestic competition, and a weak property sector. Industrial output grew 5.7% in July, down from 6.8% in June and below the 5.9% forecast. Retail sales rose 3.7%, the slowest since December 2024, missing the expected 4.6% increase.

Source: LSEG

European Open – European Indexes Higher Ahead Trump-Putin Meeting

Heading into the European Open, Pan-region futures rose 0.5%, German DAX futures increased 0.5%, and FTSE futures also gained 0.5%.

Investors are keeping a close eye on US President Donald Trump’s meeting with Russia’s Vladimir Putin on Friday, aimed at ending the war in Ukraine.

There’s concern about how long any agreement might last, and European leaders worry the US and Russia could make big decisions that leave them out or pressure Ukraine into a bad deal.

If the Trump-Putin Alaska summit gets positive feedback, European stocks are likely to see a boost. The details matter, and Europe is unlikely to fully welcome Russia, even if peace is restored. This means defense stocks might slow down their steady rise but won’t face major setbacks.

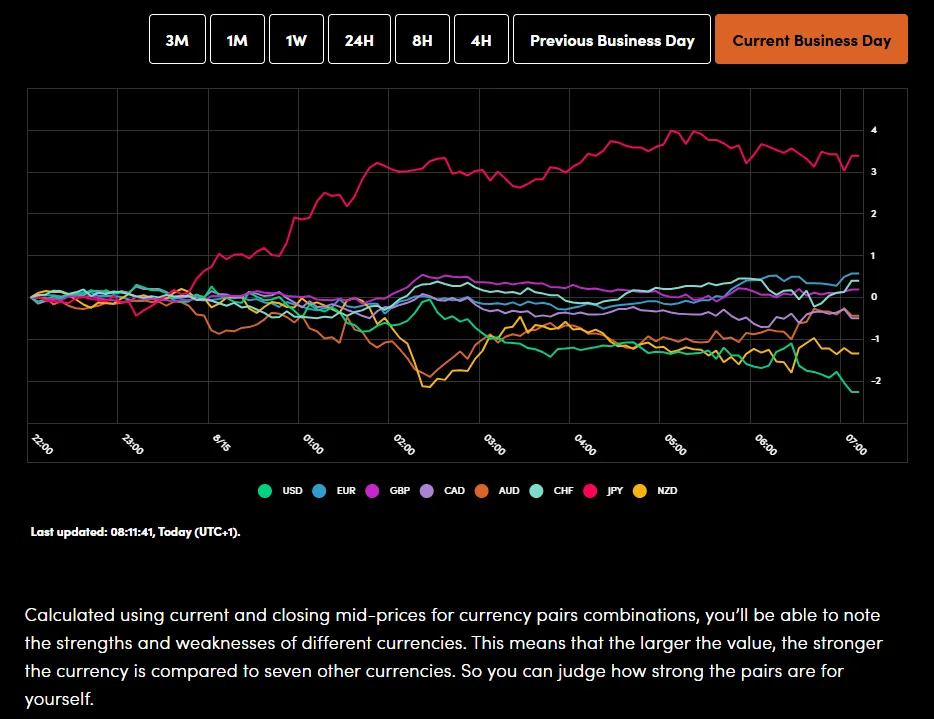

On the FX front, The euro and British pound stayed mostly unchanged after dropping 0.5% and 0.3% in the previous session, ahead of US retail sales data.

The Japanese yen strengthened thanks to surprisingly strong economic growth, with exports holding up well against new US tariffs.

The Australian dollar remained steady, while the Chinese yuan fell from a two-week high due to weaker-than-expected economic data.

Currency Power Balance

Source: OANDA Labs

For more on Gold, please read Gold’s (XAU/USD) Recovers to $3350/oz After Mixed CPI Reaction. What Next?

Economic Data Releases and Final Thoughts

Looking at the economic calendar, a busy day lies ahead.

Geopolitics will be in the news as the Trump-Putin meeting gets underway while we also have the Jackson Hole Symposium where all eyes will be on Fed Chair Jerome Powell.

From a data perspective, the US session brings retail sales numbers will give a glimpse to consumer demand but the bigger one could be the Michigan Consumer Sentiment data.

It will be interesting to see where survey respondents see inflation expectations over the 12 months in particular.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Chart of the Day – DAX Index

From a technical standpoint, the DAX index has continued to advance following yesterdays breakout.

DAX Index Two-Hour Chart, August 15. 2025

Source: TradingView.com (click to enlarge)

{kind=link}