Dollar strengthened broadly in European session despite limited fresh news flow, but it remains overshadowed by Australian Dollar. Aussie continued to draw support from today’s stronger-than-expected CPI release, which reinforced the view that the RBA will tread cautiously on rate cuts.

There is little sense of a unified theme across FX markets. Eurozone data have been inconsistent. Yesterday’s PMI surveys suggested Germany may be stabilizing, but today’s weaker Ifo survey reminded markets that the path to recovery remains fragile. Yen is under particular pressure today, probably with traders positioning for an extended rally in global equities and higher U.S. yields.

In relative terms, Aussie is the strongest currency so far this week, followed by Swiss Franc and Euro. At the other end, Loonie has been the weakest, with Yen and Kiwi also lagging. Dollar and Sterling remain mid-pack. But positioning is fluid as markets continue to digest diverging inflation and growth signals.

In Europe, at the time of writing, FTSE is up 0.01%. DAX is up 0.16%. CAC is down -0.60%. UK 10-year yield is up 0.004 at 4.687. Germany 10-year yield is up 0.002 at 2.756. Earlier in Asia, Nikkei rose 0.30%. Hong Kong HSI rose 1.37%. China Shanghai SSE rose 0.83%. Singapore Strait Times fell -0.29%. Japan 10-year JGB yield fell -0.02 to 1.640.

Germany Ifo falls to 87.8, recovery prospects dim

Germany’s Ifo Business Climate Index fell to 87.8 in September from 88.9, with Current Situation Index slipping from 86.4 to 85.7 and Expectations falling from 91.4 to 89.7. The institute said prospects for recovery have “suffered a setback”.

By sector, weakness was broad-based. Manufacturing sentiment dropped further, with companies reporting weaker orders and fading optimism among capital goods producers. Services took the hardest hit, plunging to -3.0, the lowest since February, as expectations grew more pessimistic. Trade sentiment also deteriorated, while construction offered a rare bright spot with modest improvement.

Japan’s PMI composite falls to 51.1, services resilient as factories struggle

Japan’s private sector lost momentum in September, with the flash PMI Composite slipping from 52.0 to 51.1, the weakest in four months. Manufacturing was the clear drag, with the headline index down from 49.7 to 48.4 and output falling from 49.8 to 47.3. Services held broadly steady at 53.0, down from 53.1.

S&P Global’s Annabel Fiddes said services remain the “key growth engine,” offsetting a “deepening downturn” in manufacturing. Demand trends diverged sharply, with services seeing another solid rise in sales, but factories reporting the fastest drop in new orders since April.

Cost pressures also remain high. Input price inflation has eased from earlier in the year but is still consistent with a sharp rate overall, prompting firms to raise selling prices to protect margins. Companies were more cautious on hiring, with employment growth slowing to the weakest pace in two years.

Australia CPI surprises at 3.0% in August, RBA caution ahead

Australia’s monthly CPI accelerated from 2.8% yoy to 3.0% yoy in August, above expectations of 2.8% yoy and the highest reading since July 2024. The rise was driven by housing (+4.5%), food and non-alcoholic beverages (+3.0%), and alcohol and tobacco (+6.0%).

Core inflation showed stickier trends. CPI excluding volatile items and holiday travel rose from 3.2% yoy to 3.4% yoy. Trimmed mean edged down slightly to 2.6% from 2.7%, but remain well above June’s 2.1% yoy.

RBA is widely expected to hold interest rate unchanged next week. But the stronger core reading will keep November’s meeting live, with rate cut expectations now tempered by concerns that inflation may not be easing as quickly as hoped.

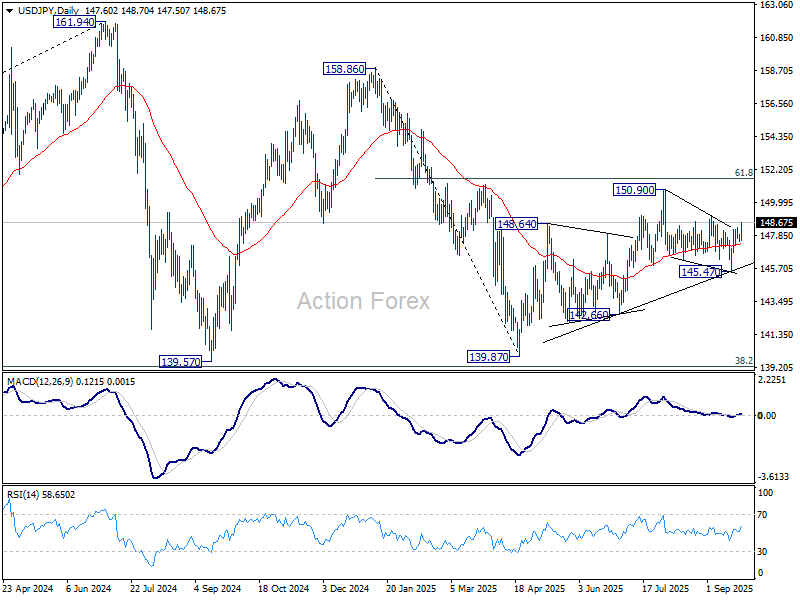

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.44; (P) 147.68; (R1) 147.91; More…

USD/JPY’s rebound from 145.47 resumes today and the strong support from 55 4H EMA affirms near term bullishness. Intraday bias is now mildly on the upside for 149.12 resistance. Firm break there should confirm that correction from 150.90 has completed at 145.47. Rise from 139.87 should be ready to resume through 150.90. On the downside, though, below 147.45 minor support will turn intraday bias neutral again.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

{kind=link}