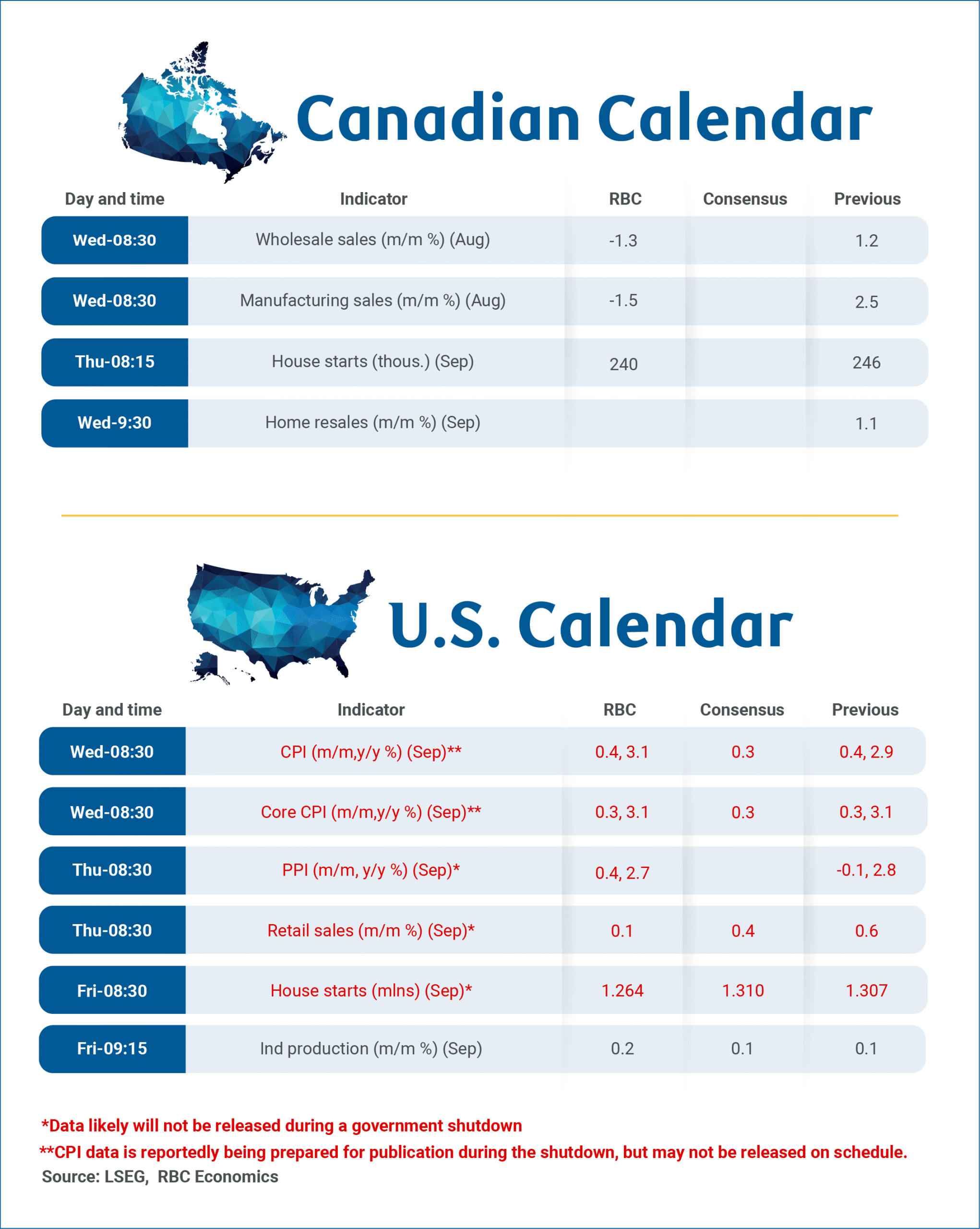

Early Canadian gross domestic product and net trade data have broadly showed signs the economy is stabilizing after contracting in Q2. However, heavily trade-exposed sectors remain under significant pressure, driving expectations for softer industry data on Wednesday.

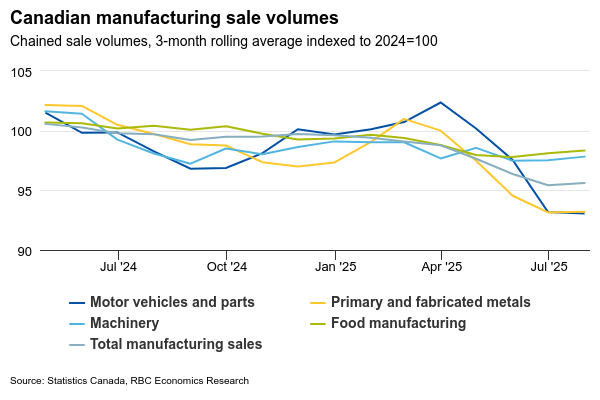

Statistics Canada’s preliminary estimate showed manufacturing sales contracted 1.5% in August, partially reversing the stronger 2.5% gain in July. Part of this swing reportedly reflected a pullback in the transportation sector following a jump in motor vehicle sales in July. Vehicle production and sales from July to August are notoriously volatile due to typical factory retooling shutdowns.

Food sales were also reportedly weaker, and the 0.5% rise in manufacturing production prices reported for August suggests sales volume likely more than reversed the 1.6% increase in July. That would leave volume down about 4.5% in August from a year ago with more substantial declines in sectors targeted by U.S. tariffs such as primary metal manufacturing.

The positive news is broader consumer demand in Canada has been resilient, supporting activities in sectors more domestically focused. StatsCan’s preliminary estimate showed a 1% increase in retail sales in August after a 0.8% decline in the previous month.

Housing activity has also continued to recover at a modest pace. Early data from local real estate boards point to a mixed national picture in September for home resales.

Overall, we maintain our expectation that softening in trade-exposed sectors will persist, but won’t spread widely to other parts of the Canadian economy. We look for weak GDP growth over the second half of this year, starting with a 0.5% annualized increase in Q3.

In the U.S., the government shutdown means key data releases, including September’s retail sales, are unlikely to be released in the coming week.

On balance, U.S. consumer spending has broadly surprised to the upside this year. Alternative data from the National Retail Federation pointed to a contraction in core retail spending (excluding auto and gas) in September, but to a level that remains well above a year ago.

September’s U.S. inflation data may still be released but with a delay, as it feeds into the calculation of cost-of-living adjustments for Social Security beneficiaries, which is considered mandatory under law. We expect headline CPI to have edged higher to 3.1% in September from 2.9%, but core ex-food and energy inflation to have held at 3.1% after another 0.3% month-over-month increase from August.

{kind=link}