Canadian Highlights

- Canadian and U.S. policymakers have yet to hammer out a trade deal, but negotiations are still ongoing.

- Trade-related headwinds dampened Canadian trade in August, with tariff-exposed sectors continuing to feel the pinch.

- Canada’s labour market recovered some of the jobs lost in the previous two months, while ongoing labour force growth kept the unemployment rate steady.

U.S. Highlights

- The government shutdown continues through its second week, with no clear end in sight, while trade tensions between the U.S. and China have suddenly heated up.

- Absent official data, the market is turning to imperfect private-sector alternatives, which suggest the labor market continued to cool in September.

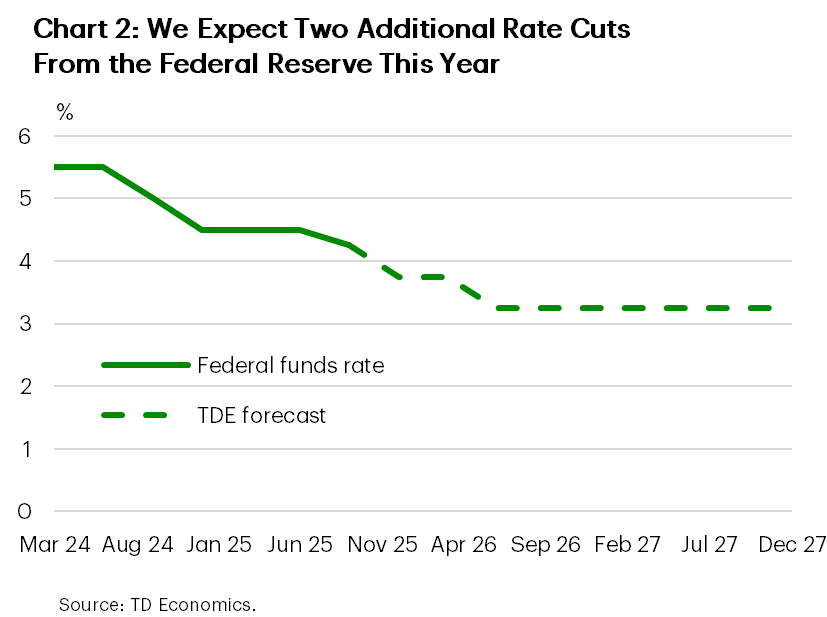

- We don’t see any developments this week that are likely to cause a big shift in the perception of the economy or the outlook, and so we are still penciling in two more quarter-point rate cuts from the Federal Reserve by year-end.

Canada – Labour Market Surprise

Toronto Blue Jays supporters have plenty reason to celebrate this week, having kept their championship dreams alive in a series win over the Yankees. Outside of the sports world, developments north of the border were a little more mixed. Let’s review the game tape and see what transpired this week.

Strike 1: Trade Talks Stall. Prime Minister Mark Carney and team went to bat for Canada during their visit to the White House; however, no trade agreement has been reached yet. Canadian trade representatives remain in Washington, continuing efforts to advance discussions, though the final outcome remains uncertain at this time. To be fair, a new comprehensive trade framework was not expected at this meeting—such progress is anticipated during next year’s USMCA review—but there is optimism that smaller deals regarding sector-specific tariffs can be reached soon. On a positive note, both sides have expressed confidence that a trade agreement will eventually be achieved, even if certain tariffs persist.

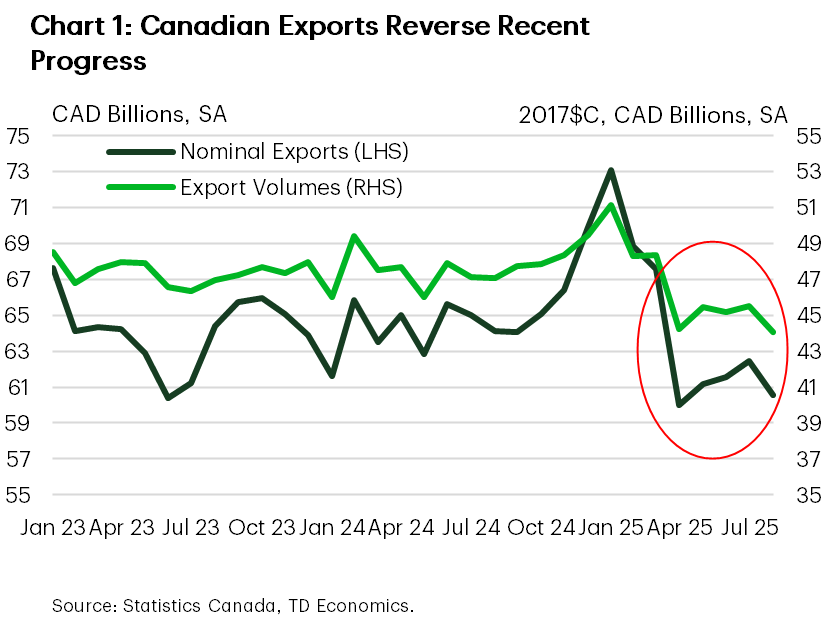

Strike 2: Export Recovery Experiences a Setback. Canadian exports declined by a hefty 3.0% month-on-month in August (Chart 1), with notable decreases observed in shipments to both U.S. and non-U.S. markets. Consequently, much of the progress made since the trade rebound began in April has been reversed. Recent trade flows have exhibited increased volatility, largely attributable to substantial movements of unwrought gold as buyers respond to the meteoric gold rally. Looking through the noise, one pattern is consistent: exports of goods to the U.S. subject to sectoral tariffs—specifically in steel, aluminum, automobiles, and lumber—are generally underperforming other export categories.

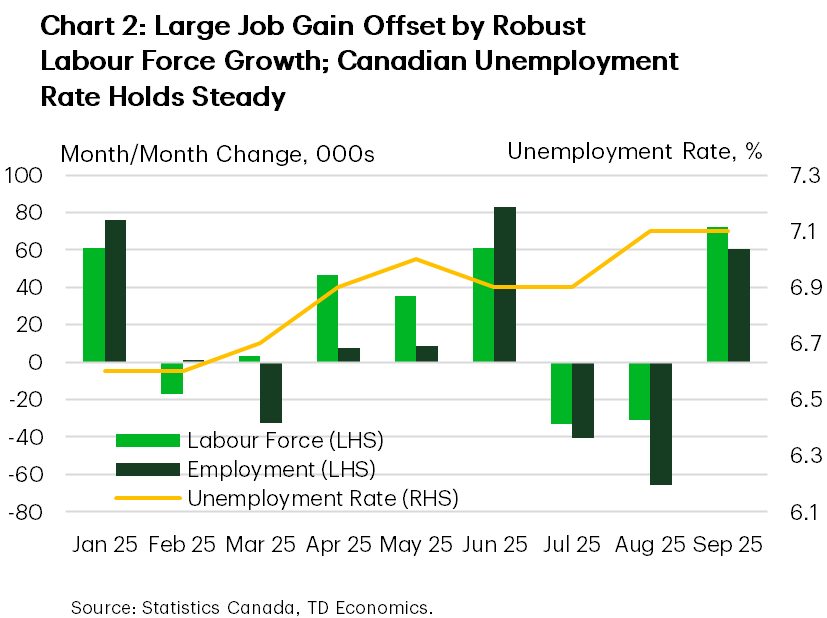

Base Hit: Canada’s Job Growth Exceeds Expectations. Labour market data for September indicated the Canadian economy added 60k jobs, significantly outperforming consensus forecasts for no job growth. This increase offsets more than half of the losses incurred in the previous two months, with employment gains distributed across multiple sectors. Notably, trade-exposed sectors—including manufacturing, agriculture, energy, and wholesale trade—recorded solid gains for the month. Zooming out, employment in Canadian industries most susceptible to U.S. trade remains below the performance of other segments of the economy. Despite the sturdy print, the unemployment rate remained steady at 7.1%, attributed to the largest influx of individuals into the labour force since November 2024.

The Bank of Canada will convene at the end of the month to make their next interest rate decision. This week’s jobs data may influence the BoC to hold rates steady. Markets also responded by lowering their expectations of a 25 bps cut from 60% earlier this week to around 40% as of writing. An update to Canadian inflation, in around two weeks, will play a significant role in the Bank’s decision. Though underlying inflation continues to hover within target range, strong evidence of waning inflation momentum will likely be required for the BoC to consider another rate cut.

U.S. – No Data, No Problem

Up until Friday, markets had been relatively calm amid the ongoing government shutdown, which has entered its 10th day. President Trump’s threat to increase tariffs on China this morning, in response to China’s export controls on rare-earth metals, has upended that. President Trump has gone so far as to declare he is not interested in meeting President Xi in person as previously scheduled for the end of the month, leading to a sharp sell-off in US equities and pushing Treasury yields lower. Markets stoically withstood the failure of seven separate proposals to re-open the government, but the possible breakdown of U.S.-China trade negotiations may be too much to bear. If that wasn’t enough, the end of the shutdown is not clearly in sight. The Senate is now adjourned until October 14, which all but guarantees that military members will miss a full pay cycle, an unprecedented development.

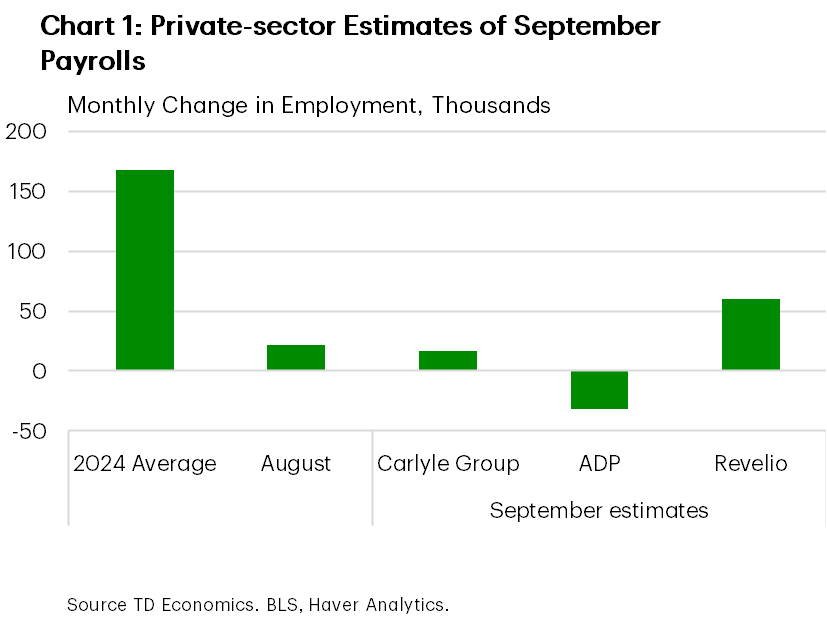

The outlook for the shutdown is not the only thing that is cloudy. The government shutdown means that official economic data are not being published, and policymakers, businesses, and households are unable to see new data on the state of the economy. Various private-sector groups have produced estimates of what happened to employment in September, shown in Chart 1. This was the key piece of data which was due to be published last Friday. While these alternative estimates generally suggest the labor market continued to cool through September, these measures are at best imperfect proxies for the official data. As for what data we do have this week, the preliminary reading of the University of Michigan’s consumer confidence ticked a touch higher in October. However, expectations on the future outlook continued to slide for a third consecutive month, likely driven by the softening labor market and still elevated uncertainty on trade policy.

Several members of the FOMC spoke this week, offering some insight into their thinking amidst the shutdown. New York Fed President Williams indicated that the lapse in government data would not deter him from further easing the policy rate at the Fed’s coming meetings. Meanwhile, other speakers continued to reiterate prior views. Kansas City Fed President Schmid voiced concern about inflation, while Miran, the only FOMC member to vote for a larger 50 basis point rate-cut at the last meeting, again indicated how he expected inflation to moderate. It is little surprise that market pricing at the next Fed meeting has remained relatively unchanged through the government shutdown. Expectations for further easing at a moderate pace are in line with the general view we observed in the FOMC minutes released this week, that interest rates are currently moderately restrictive and risks have shifted somewhat to the downside.

Normally, we would be looking ahead to next week’s release of CPI for more information on how prices are reacting to tariffs, but we are following the shutdown. We will also be closely watching trade negotiations between the U.S. and China to see what comes of today’s escalation.

{kind=link}