- The Labour government will likely face a big fiscal hole in the upcoming budget. We expect they will close the gap and deliver some welcomed fiscal tightening for markets, even if it will be unpopular amongst voters.

- We remain negative on GBP as tailwinds from more sustainable fiscal policies will be counterweighed by negative growth impact and a USD negative environment.

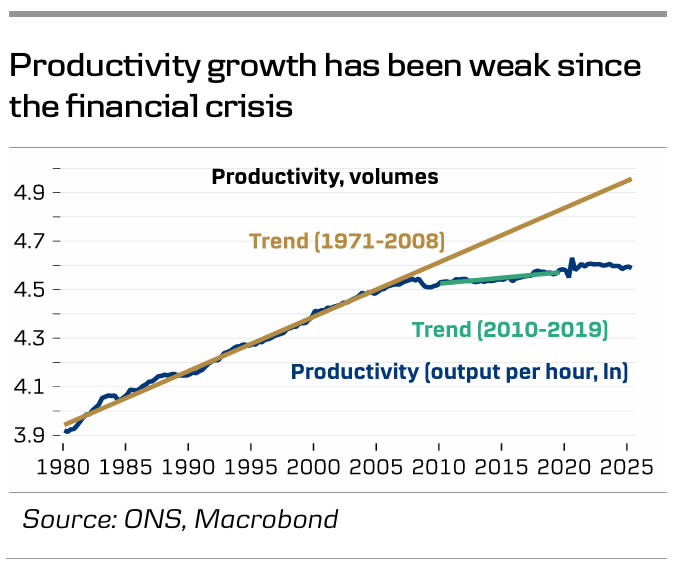

On 26 November, the annual Autumn Statement will be presented in the UK accompanied by independent forecasts from the Office of Budget Responsibility (OBR), the UK fiscal watchdog. Chancellor Rachel Reeves faces a significant fiscal shortfall, amongst others due to an expected 0.3 percentage point cut in trend productivity growth by the OBR. This adjustment, which is bigger than analysts had predicted of 0.1-0.2 percentage points, deepens the fiscal hole by approximately another GBP12bn, based on estimates from the Institute of Fiscal Studies, bringing the total shortfall to GBP30-40bn (including a modest GBP10bn. headroom). However, factors such as higher inflation and wage forecasts, along with the recent sharp decline in Gilt yields, could help offset some of the impact if accounted for by the OBR.

The large fiscal shortfall makes it increasingly challenging for the Labour government to uphold its promise to freeze income tax rates, National Insurance contributions and VAT, the three main sources of revenue. Reeves has indicated potential tax rises and spending cuts blaming Brexit and the previous Conservative government for the fiscal and economic troubles. We believe Labour will aim to address the fiscal gap now with the next general election still distant to avoid the risk of more tax hikes later. As a result, we think the budget is set to alleviate some pressure in the Gilt market.

Key for Gilt markets and GBP FX will be whether the government might adjust fiscal rules to avoid tough decisions. One option could be advancing next year’s rule change, allowing a 0.5% of GDP deficit, which would ease budget pressures but risk alarming Gilt investors. The government’s ability to fully address the challenge and secure sufficient headroom will be critical. Keeping Labour’s promise appears difficult and could lead to reliance on uncertain revenues from new taxes or less credible spending cuts, both negative for Gilts. Breaking promises by raising more predictable revenues such as the income tax would be positive. A 1 percentage point increase to the basic rate would raise GBP8bn. according to the UK tax authorities. Alternatively, a VAT hike, which Reeves hasn’t ruled out, could boost revenue but will trigger higher inflation, at least in the short term and in turn put upward pressure on short end UK yields.

We stay negative on GBP FX. While a significant tightening of fiscal policy would alleviate some pressure in terms of the negative impact from unsustainable public finances, we highlight the negative growth impact. If we get a significant tightening, this will act as a further headwind for the UK economy and likely trigger more substantial easing from the BoE. Combined with a global investment environment characterised by a positive correlation to a USD negative environment, in our view, favours a weaker GBP. We expect EUR/GBP to trend higher the coming year, targeting the cross at 0.89 in 12 months.

, the UK fiscal watchdog. Chancellor Rachel Reeves faces a significant fiscal shortfall, amongst others due to an expected 0.3 percentage point cut in trend productivity growth by the OBR. This adjustment, which is bigger than analysts had predicted of 0.1-0.2 percentage points, deepens the fiscal hole by approximately another GBP12bn, based on estimates from the Institute of Fiscal Studies, bringing the total shortfall to GBP30-40bn (including a modest GBP10bn. headroom). However, factors such as higher inflation and wage forecasts, along with the recent sharp decline in Gilt yields, could help offset some of the impact if accounted for by the OBR.){kind=link}