American consumers felt slightly better about the economy in early December, according to a survey released on Friday.

The Consumer Sentiment Index from the University of Michigan went up to 53.3 this month, an improvement from 51.0 in November, and slightly better than what economists expected.

However, the overall mood remains gloomy. The main problem is that consumers are still very worried about high prices (inflation) and are not very optimistic about the job market.

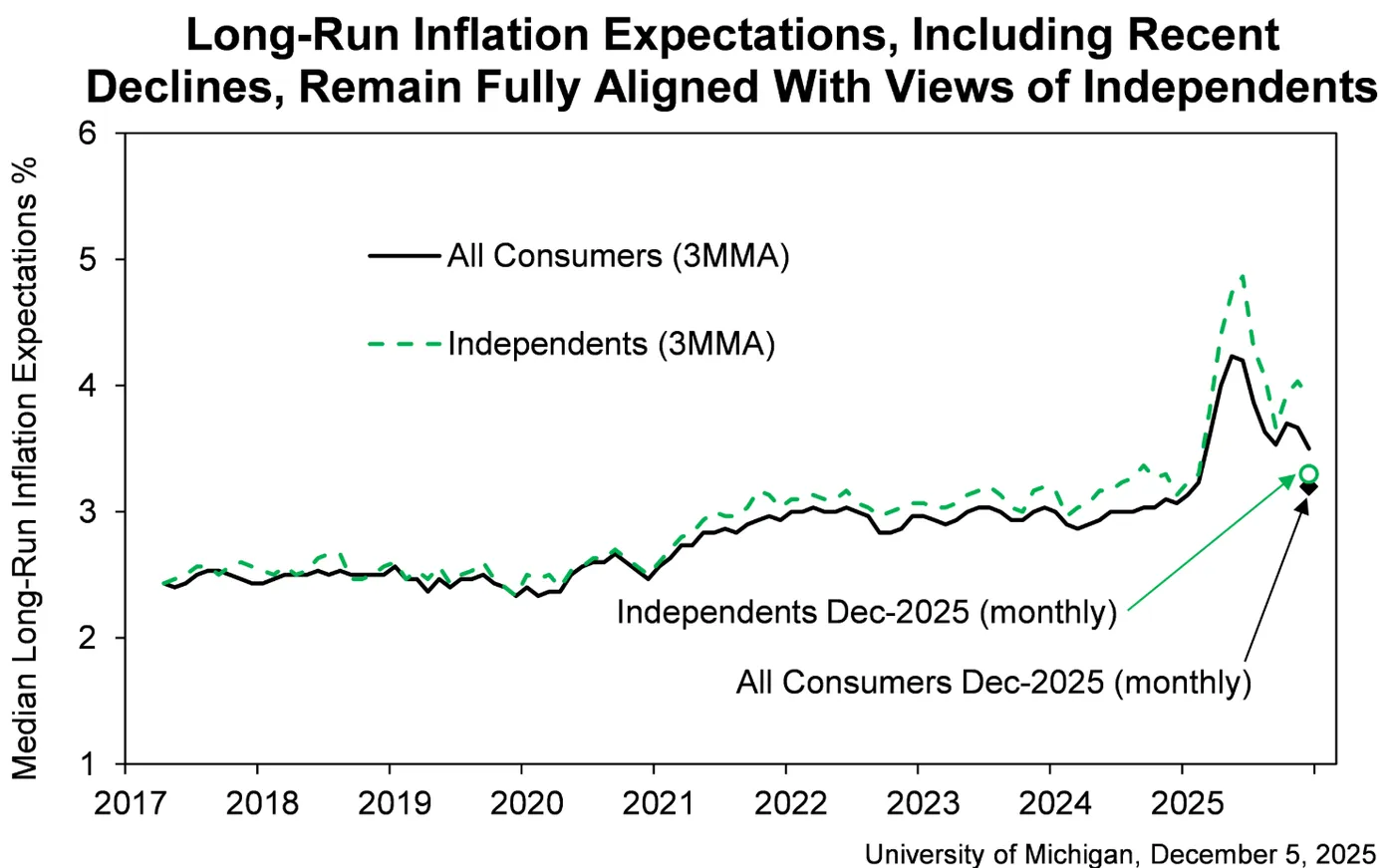

On a positive note, consumers expect price increases to slow down slightly: they now anticipate inflation will be 4.1% over the next year, down from 4.5%, and 3.2% over the next five years, down from 3.4%.

Source: UofM

PCE Data Release for September 2025

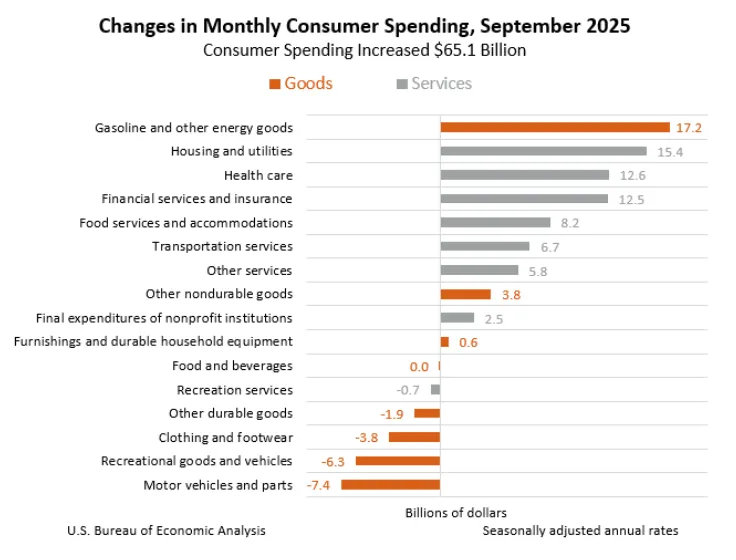

In September 2025, Americans spent 0.3% more than they did in August, which was a total increase of about $65.1 billion. This increase was exactly what financial experts had predicted.

The main reason for this spending growth was a large jump in spending on services (up by $63.0 billion), especially on housing, utilities, healthcare, and financial services. Spending on physical goods saw only a small increase (up by $2.1 billion).

This small gain was due to a sharp rise in the cost of gas and other energy; otherwise, spending would have fallen, as people spent less money on things like cars, recreational items, and clothes.

Source: US Bureau of Economic Analysis

Market Impact & US Dollar Index (DXY) Reaction

The data was not really a huge surprise and heading into the release i did not expect it to have a major impact on the Interest rate outlook moving forward for the Federal Reserve.

Those assumptions have been proved correct with rate cut expectations remaining relatively unchanged for next week’s Federal Reserve meeting. Markets are still pricing in around an 87% probability of a 25bps rate cut next week.

Heading into next week’s Fed meeting, I still believe that the economic projections may hold more weight than the actual decision by the Fed. This is unless the Fed defy market expectations and hold rates steady. Any rate cut may receive a lukewarm response.

However the 2026 economic projections and particularly those around how many rate cuts the Fed sees in 2026 could stoke significant volatility.

At the previous meeting the Fed’s economic projections only showed one 25 bps rate in 2026. Any dovish or hawkish tilt in this regard could send market volatility soaring.

Following today’s data, the US dollar index slipped further as pressure continues to mount on the greenback.

Immediate support rests at 98.72 before the 100-day MA at 98.58 and the 98.00 handles come into focus.

On the upside, resistance may be found at the 200-day MA resting at 99.51 before the psychological 100.00 becomes an area of focus once more.

US Dollar Index Daily Chart, December 5, 2025

Source: TradingView

Trade Safe.

{kind=link}