Yen weakened broadly today despite the BoJ delivering a widely expected 25bps rate hike. The move pushed 10-year JGB yields above the psychologically important 2% level for the first time since 1999, but higher yields failed to translate into currency support.

Part of the reaction reflects a classic sell-on-news dynamic. With the long-anticipated BoJ decision out of the way, markets reverted to the prevailing trend rather than extending positioning on the headline outcome. More importantly, the BoJ offered little clarity on where policy rates are ultimately heading. While the tightening bias was retained, there was no guidance on the destination, leaving investors without a clear anchor for longer-term Yen valuation.

Governor Kazuo Ueda openly acknowledged that estimates of Japan’s neutral rate span a wide range, with no consensus on where it lies. That uncertainty argues for caution, particularly as any further rate increase would push policy closer to neutral, if not into it. As a result, markets are increasingly skeptical that the BoJ will move again any time soon. Without a credible path toward materially higher rates

Elsewhere, Dollar is recovering from its post-CPI selloff. While November inflation data showed a sharp cooling, skepticism has grown around the quality of the report due to gaps caused by the government shutdown. Some economists have labeled the release a “Swiss cheese” CPI report, highlighting missing components as the lots of holes. Most notably, shelter costs—roughly a third of the CPI basket—were absent, significantly distorting the inflation signal. Missing data were effectively treated as showing no price growth, raising concerns about statistical reliability.

That has tempered enthusiasm for aggressive Fed repricing, even as inflation appears to be easing. For now, the Fed is still expected to hold rates in January, with March cut odds hovering around 55%. With three more months of jobs and inflation data still to come, it remains premature to draw firm conclusions.

In FX markets this week so far, Swiss Franc leads, followed by Dollar and Sterling, while Kiwi lags despite strong domestic data today, followed by Aussie and Yen. Euro and Loonie sit in the middle.

In Asia, Nikkei rose 1.03%. Hong Kong HSI rose 0.69%. China Shanghai SSE rose 0.36%. Singapore Strait Times is up 0.10%. Japan 10-year JGB yield rose 0.056 to 2.022. Overnight, DOW rose 0.14%. S&P 500 rose 0.79%. NASDAQ rose 1.38%. 10-year yield fell -0.035 to 4.116.

BoJ raises rates to 0.75%, keeps tightening bias intact

The BoJ raised its policy rate by 25bps to 0.75%, as widely expected, marking another step in its gradual normalization process. Despite the hike, the BoJ emphasized that financial conditions remain highly accommodative, with real interest rates still “significantly negative.”

In its statement, the BoJ reaffirmed a tightening bias. If the outlook laid out in the October 2025 Outlook Report is realized, the Bank said it will “continue to raise the policy interest rate”. Policymakers also expressed increased confidence that the likelihood of realizing the outlook “has been rising”.

At the post-meeting press conference, Governor Kazuo Ueda stressed future adjustments will depend on incoming data on economic, price, and financial conditions, with policy decisions reassessed at every meeting rather than following a preset path.

On the neutral rate, Ueda acknowledged substantial uncertainty. He described the estimate as sitting within a wide range and said they would assess how the economy and prices respond to each rate move. “We will seek to produce new estimates on Japan’s neutral rate, if needed, though I don’t think that will help us narrow the range that much,” he added.

NZ trade deficit narrows to ND -163m on 9.2% yoy exports surge

New Zealand’s trade balance surprised to the upside in November, with the deficit narrowing sharply to NZD -163m, far smaller than expectations for a shortfall of around NZD -1.2B. The improvement was driven by a solid pickup in exports, which rose 9.2% yoy, or NZD 588m, to NZD 7.0B.

Export performance was mixed by destination. Shipments to Australia surged by 31% yoy, while exports to the EU also rose strongly by 51% yoy. By contrast, exports to China slipped modestly by -0.7%yoy, while shipments to the US fell sharply by -17% yoy, and Japan by -1.9% yoy.

Imports rose at a more moderate pace of 4.4% yoy to NZD 7.2B. Gains were led by stronger inflows from the US (36% yoy), EU (17% yoy) and South Korea (20% yoy). Imports from China rose a modest 1.7% yoy. Imports from Australia declined (-7.7% yoy).

NZ ANZ business confidence hits 30-year high as cyclical recovery gathers pace

New Zealand business confidence surged in December, with the ANZ headline index jumping from 67.1 to 73.6. Firms’ own activity outlook rose sharply from 53.1 to 60.9. Both readings are the strongest in 30 years, pointing to a broad-based improvement in sentiment as the economic cycle turns.

Inflation indicators ticked up modestly but remain contained. The share of firms expecting to raise prices in the next three months rose one point to 52%, while those anticipating cost increases climbed two points to 76%. Inflation expectations, however, were unchanged at 2.69%, suggesting confidence is improving without triggering a renewed inflation scare.

ANZ said “things are clearly looking up,” noting that the earlier slowdown was deliberately engineered by tight monetary policy. With that restraint easing, interest rates and the exchange rate both well below their peaks, and the RBNZ signaling no intention to hike rates any time soon, cyclical forces appear firmly supportive of recovery.

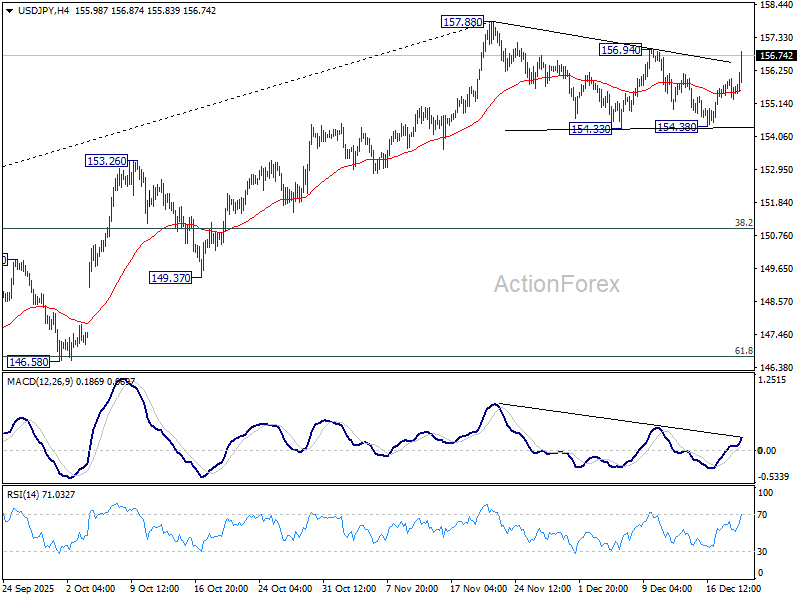

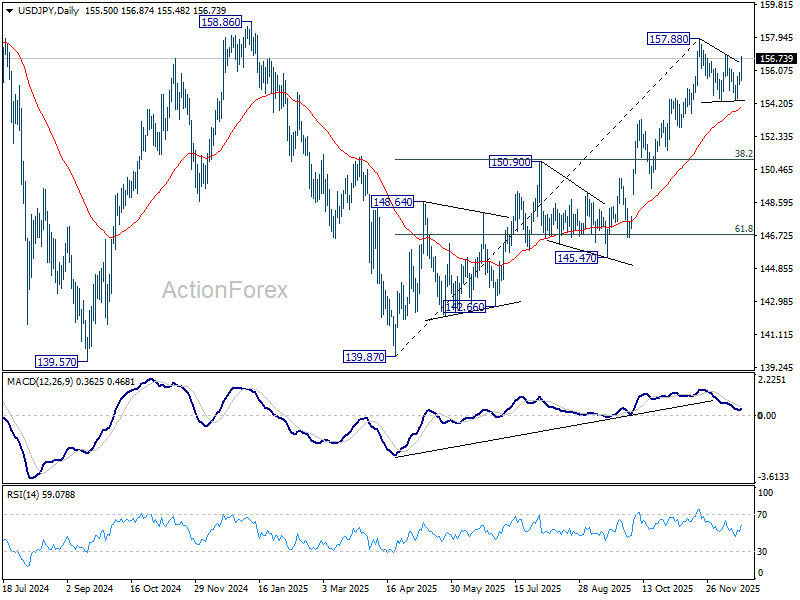

USD/JPY Daily Outlook

Daily Pivots: (S1) 155.23; (P) 155.61; (R1) 155.93; More…

Immediate focus in USD/JPY is now on 156.94 resistance with today’s strong rise. Firm break there will argue that larger rally from 139.87 is resuming through 157.88 to 158.85 key structural resistance. Decisive break there will be a strong medium term bullish signal. Risk will now stay on the upside as long as 154.38 support holds, in case of retreat.

In the bigger picture, corrective pattern from 161.94 (2024 high) could have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. Decisive break of 158.85 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 150.90 resistance turned support will dampen this bullish view and extend the corrective range pattern with another falling leg.

{kind=link}