There is little on the economic calendar for the final week of the year, leaving Fed minutes from the December meeting as the lone focal point for markets during the New Year holiday stretch. The minutes are expected to shed light on the internal debate that produced a rare three-way split. Chicago Fed President Austan Goolsbee and Kansas City Fed President Jeffrey Schmid both voted to hold rates steady. At the opposite extreme, ultra-dove Governor Stephen Miran dissented in favor of a larger 50bp cut. The remaining policymakers backed the consensus move, delivering a 25bp reduction that lowered the target range to 3.50–3.75%.

The accompanying statement tweak was just as important as the vote itself. By implying a higher hurdle for additional cuts, the Fed effectively endorsed market pricing for a January hold, even as longer-term expectations remain unsettled. That uncertainty is evident in futures markets, where odds of a March cut hover around 50%.+

Meanwhile, the dot plot exposed just how divided the committee remains. Excluding Miran, policymakers were almost evenly split, with four projecting one cut in 2025 and seven seeing no cuts at all—including scenarios involving renewed tightening. At the same time, seven officials penciled in two or more cuts in 2026. This wide dispersion suggests it will take a meaningful shift in data to pull expectations decisively away from the median one-cut outlook.

With that backdrop, it is premature to draw firm conclusions, at least not before the December non-farm payrolls report on January 9, which is likely to be the next genuine catalyst for repricing Fed expectations.

Attention is also firmly on geopolitics. US President Donald Trump said talks with Ukrainian President Volodymyr Zelenskyy were “getting very close” to a peace agreement, though he acknowledged major unresolved issues, including the fate of the Donbas region. Security guarantees also remain another sticking point. Zelenskyy said agreement had been reached in principle, while Trump was more cautious, suggesting Europe would need to shoulder much of the responsibility with US backing. Zelenskyy later said he had requested security guarantees lasting up to 50 years and that any peace deal should be put to a referendum during a 60-day ceasefire.

In the currency markets, Yen is leading gains for the day so far, followed by Dollar and Euro. While Kiwi, Aussie, and Loonie lag, and Sterling and Swiss Franc trade near the middle of the pack.

In Europe, at the time of writing, FTSE is down -0.01%. DAX is down -0.10%. CAC is up 0.09%. UK 10-year yield is down -0.09 at 4.495. Germany 10-year yield is down -0.021 at 2.845. Earlier in Asia, Nikkei fell -0.44%. Hong Kong HSI fell -0.71%. Chian Shanghai SSE rose 0.04%. Singapore Strait Times fell -0.05%. Japan 10-year JGB yield rose 0.017 to 2.058.

BoJ opinions suggests series of hikes as neutral rate remains distant

The latest Summary of Opinions from the BoJ’s December 18–19 meeting reinforced a clear tightening bias, with many policymakers arguing that the December rate hike should not mark the end of the cycle.

One opinion noted there was “still considerable distance” to neutral levels, explicitly calling for rate hikes at “intervals of a few months”. Another linked Yen weakness and rising long-term yields partly to the policy rate being too low relative to inflation, suggesting delayed normalization risks exacerbating financial distortions.

Inflation concerns featured prominently throughout the discussion. Several members described recent price pressures as “sticky”. One opinion highlighted spring wage negotiations as a key test, arguing that a third consecutive year of target-consistent wage growth would confirm underlying inflation has reached 2%.

Still, not all voices favored an aggressive path. Some policymakers urged caution, citing uncertainty around the neutral rate and shifting global rate environments. They argued flexibility should take precedence over targeting a specific policy level.

At the meeting, the BoJ raised its policy rate to a 30-year high of 0.75%.

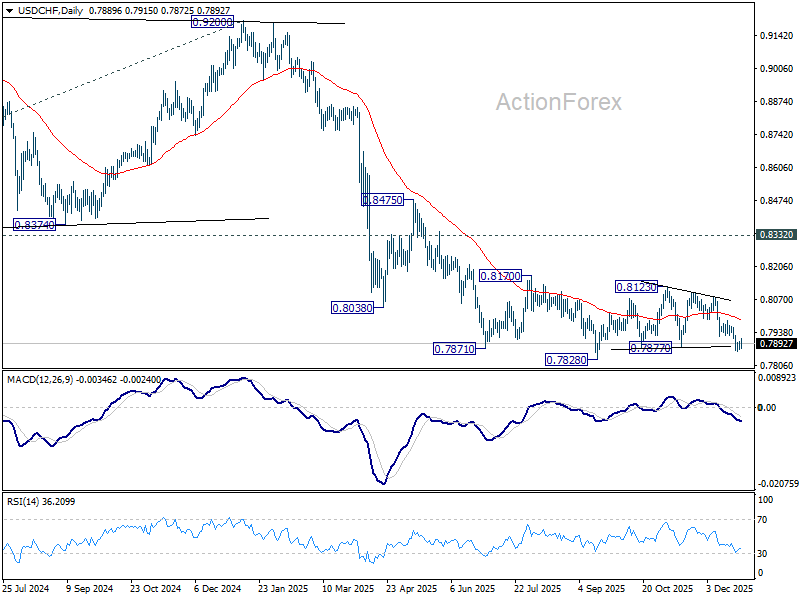

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7868; (P) 0.7886; (R1) 0.7914; More….

Intraday bias in USD/CHF remains neutral and more consolidations would be seen above 0.78670 temporary low. While stronger recovery cannot be ruled out, further fall is expected as long as 0.7986 resistance holds. Break of 0.7860 will target 0.7828 low. Decisive break there will confirm larger down trend resumption.

In the bigger picture, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low). Long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382.

{kind=link}