Canadian Highlights

- Canada’s economy starts 2026 under a cloud as underlying domestic demand remains weak.

- Trade losses with the U.S. have been primarily offset by gains in resource, metals, and agricultural trade, while key manufactured goods still face tariff challenges.

- Building on positive momentum while addressing key underlying issues will be critical for success in 2026.

U.S. Highlights

- 2026 is shaping up to be another wild ride as international trade policy and the November midterm elections take top billing.

- The upcoming Supreme Court ruling on the scope of executive authority in setting tariff policy is expected in the coming weeks, while President Trump is expected to trigger the renegotiation of the USMCA ahead of its official review period in July.

- While the labour market is showing signs of easing, relatively robust inflation will likely limit the Fed to two cuts this year, while growth remains steady at around trend for 2026.

Canada – Time to Deliver

After a 2025 that featured a historic disruption to Canada’s economic relationship with its biggest trading partner, 2026 starts with the promise of a fresh start. The economy has shown some mettle, likely growing 1.7% in 2025 as data revisions revealed better-than-expected past performance and large swings in trade-flattered topline figures. However, there are real cracks under the surface (domestic demand contracted in two quarters this year) and focus is now firmly on how Ottawa’s strategy of new infrastructure, defense spending, and greasing the wheels on major projects to diversify trade markets begins to be delivered.

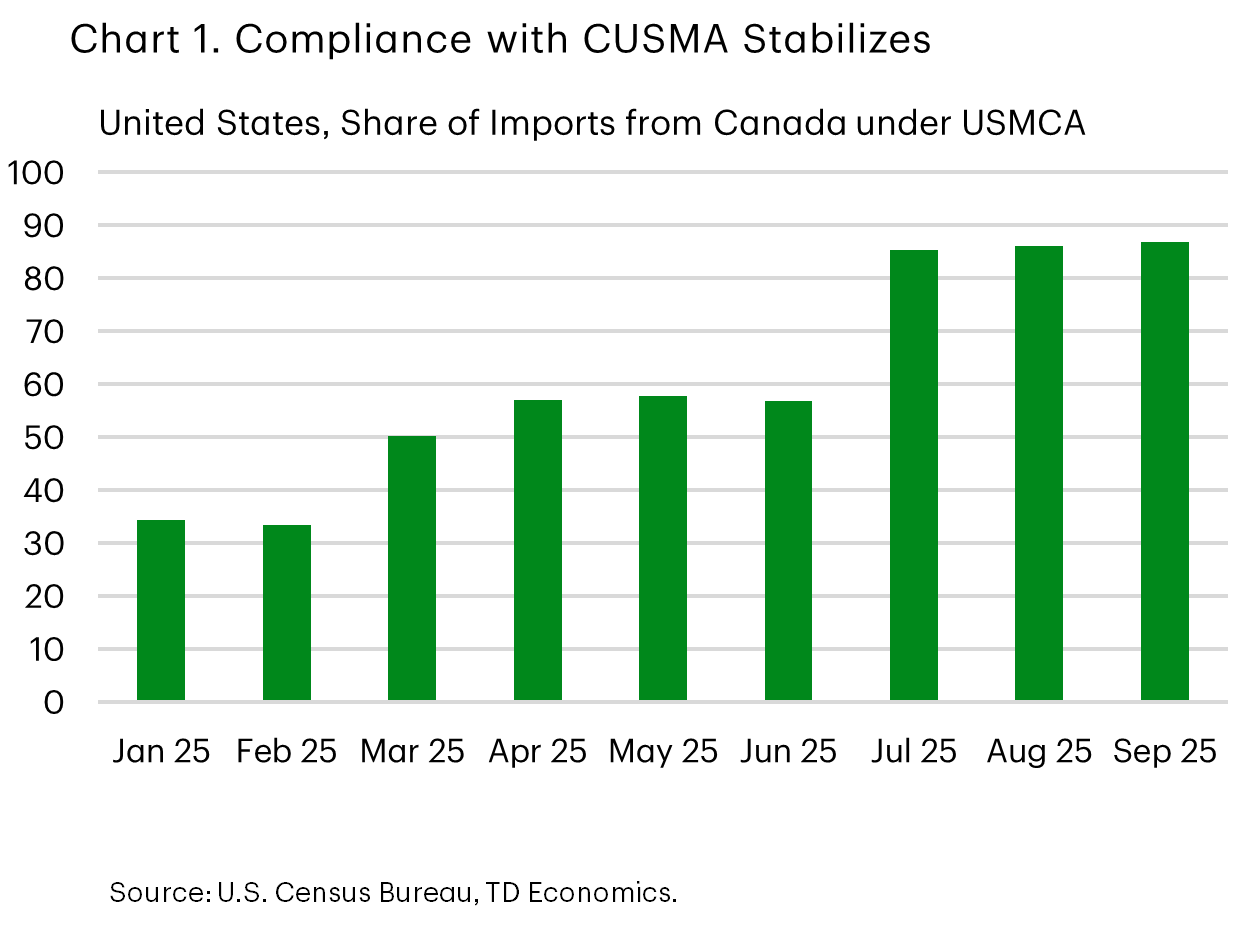

Next week, the trickle of data updates on Canada’s economy will resume. Delayed information on October’s trade balance will give another snapshot of how the process to diversify trading partners is going. Thus far, Canada has managed to more than offset the $13.0 billion decline in exports to the U.S. with $16.3 billion in flows to the rest of the world. Moreover, roughly 87% of Canadian exports to the U.S. in September (the last month for which we have data) were still duty-free as the increase in compliance under CUSMA has (thus far) shielded products from the 35% tariff rate (Chart 1). Unfortunately, there is more to this data than meets the eye.

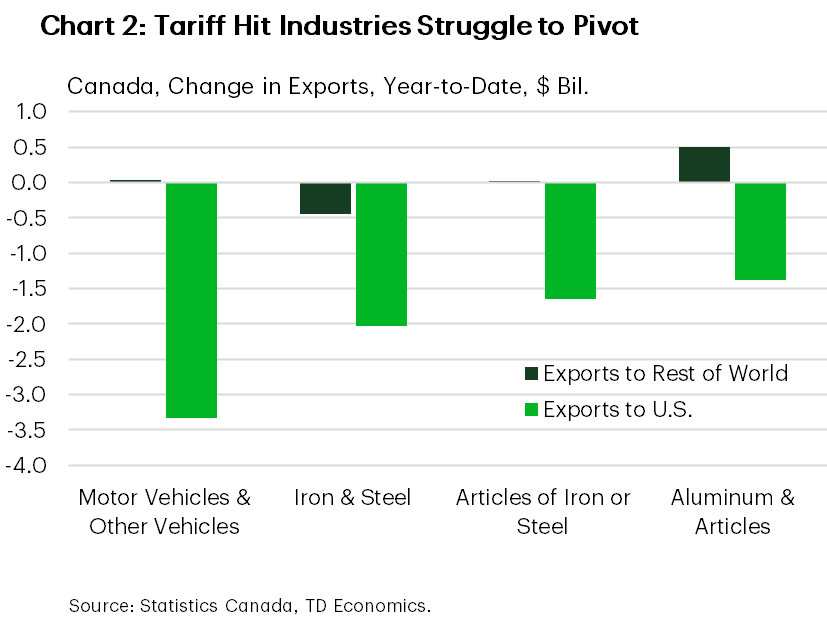

The protection conveyed by CUSMA doesn’t extend to specific goods tariffed under Section 232 of the Trade Expansion Act. These levies have materially affected the competitiveness of Canadian manufactured goods south of the border. Motor and Other Vehicles (-$3.3 billion year-to-date), steel & iron (-$2.0 billion), and aluminum (-$1.4 billion) exports to the U.S. have contracted significantly. Moreover, flows abroad for most of those products have not been sufficient to offset the lost revenues (Chart 2).

Secondly, the offsets to the trade losses are not coming from redirecting flows elsewhere, but by growth in other sectors. In fact, the economy has (generally) fallen back on the resource sector and raw materials sectors to grow exports. Leading the way are shipments of gold (+$5.3 billion), oil (+$3.8 billion), cereals (+0.9 billion) and fertilizer ($0.7 billion). A silver lining in non-resource sectors has been the aerospace industry. Aircraft exports are up over a billion dollars compared to the first nine months of 2024, and when jet engines are included in the tally, that contribution rises to roughly two billion dollars.

What the data reveal are the tricky particularities Canada faces when it comes to competing in the global marketplace. The regional elements of Canada’s economy mean that the parts of the country leading the charge on diversification are not necessarily those losing out from market access to our country’s largest trading partner. Moreover, CUSMA is set for a review this year, and its future is all but certain. Looking to 2026, the challenges facing the economy are daunting, so here’s hoping that the positive momentum (where we’ve seen it) can hold up while the key issues are addressed.

U.S. – 2026: More Political Chaos on Top of Underlying Resilience

Like it or not, 2025’s wild ride likely has more legs as 2026 is shaping up to be another rollercoaster year. Headline-grabbing political drama is likely to continue, coupled with an economy that will likely show resilience in the face of it.

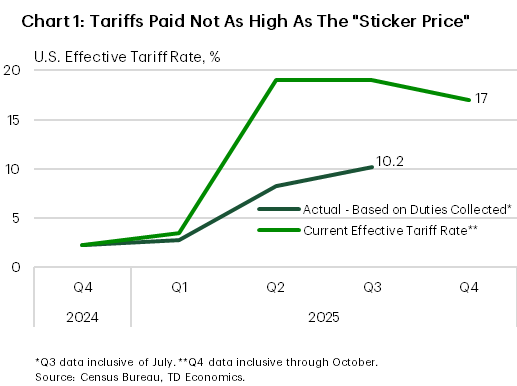

Trade policy will be front and center. One of the most closely watched legal developments is the Supreme Court’s pending decision regarding the scope of Presidential authority under the International Emergency Economic Powers Act (IEEPA), particularly as it relates to President Trump’s Liberation Day tariff package. With the decision expected in the coming weeks a ruling overturning the tariffs is unlikely to stem trade uncertainty given that the President could simply turn to other tariff measures. These include expanding Section 232 and 301 tariffs applied to imports deemed to be a national security threat or against countries that employed unfair trade practices against the U.S. Or, the President could employ unused tariff policies, including temporary Section 122 or 338 tariffs which are currently not in use. In either case, the decision will not un-ring the bell (Chart 1).

The renegotiation of the USMCA is another trade policy development to watch. While the official review doesn’t start until the 5th anniversary of the agreement in July, the U.S. has already released a list of trade concerns with Canada that will be part of negotiations. While the discussion could feature fits and starts as was the case in 2025, a renewed agreement would be a key factor in both lifting trade uncertainty in North America and opening the door for more countries to pursue deals that either fell by the wayside or did not exist at all last year.

The Midterm elections will be the main event to watch in 2026 – the house, 33 senate seats and 36 state gubernatorial races will be decided in November and a Democratic flip of either House or Congress could give Democrats renewed political power through committee and impede the President’s agenda in 2027. Current polling suggests the Senate will likely remain in Republican hands, while the House could lean in either direction depending on numerous close races.

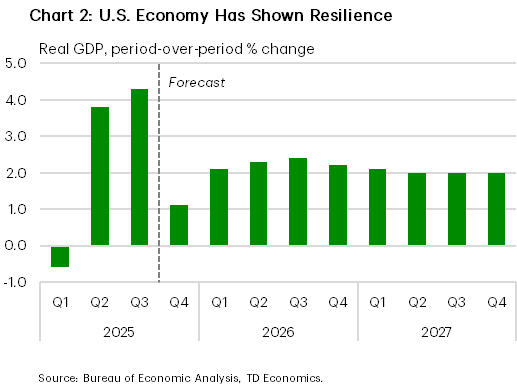

The evolution of economic growth will be a critical factor in deciding the outcome. To that end, the U.S. economy has shown more resilience than forecasters would have suggested a year ago, given the upending of international trade policy. GDP growth has averaged more than 4% in the 2nd and 3rd quarters, with a robust pace of consumer and business spending to boot. The fly in the ointment is that the labor market has notably weakened over time, with stagnant job growth pushing the unemployment rate to its highest level since 2021. But with domestic demand and inflation still holding up, we think this limits the Fed to just two additional cuts next year. The coming year will likely feature an evening out of these factors with still a healthy pace of growth around trend (Chart 2), driven by more trade certainty, the deregulatory impacts of the One Big Beautiful Bill Act, and ultimately, an underlying resilience that is hard to doubt.

{kind=link}