Canadian Highlights

- Canada’s unemployment rate jumped higher to 6.8% in December as rapid labour force growth outweighed tepid employment gains.

- Canada’s goods trade balance is back in deficit territory. But trade in gold continues to whipsaw both import and export readings, making discerning trends more challenging.

- Prime Minister Carney will visit China next week to discuss investment and trade; a timely meeting on the heels of the U.S./Venezuela situation.

U.S. Highlights

- The payrolls report for December came in weaker than expected, capping off the “low hire, low fire” 2025 jobs market.

- Global oil markets adjusted to the possible return of Venezuelan crude to global markets following U.S. actions in the country.

- Investors will have to stay tuned for the Supreme Court’s ruling on the IEEPA tariffs.

Canada – Jobs, Trade, and Global Shifts

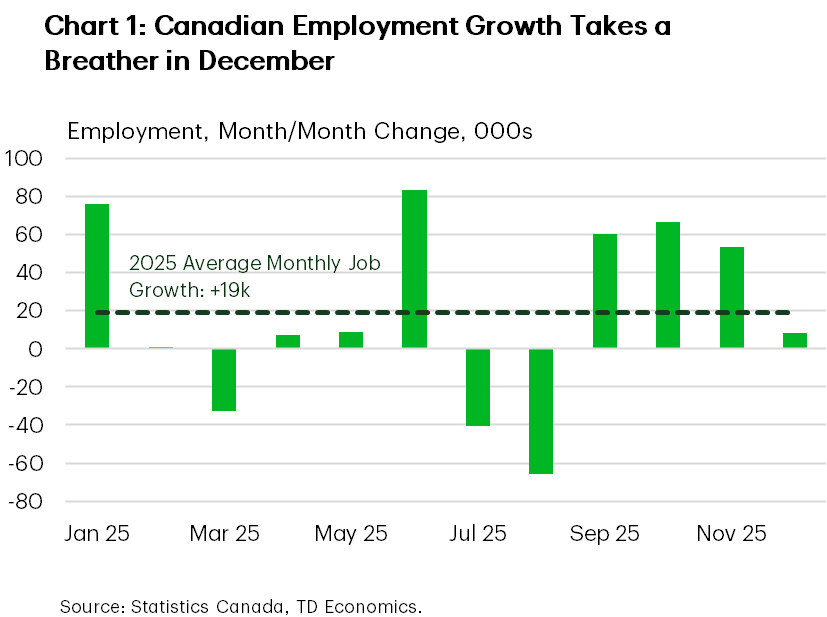

Data flow this week showed the Canadian economy entered the tail end of the year on a slightly positive note. An update to Canada’s job market was the headliner, with job creation totaling a modest 8k for the month of December. While this edged out market expectations, it represents a deceleration from the blistering 60k average gain over the prior three months (Chart 1). The unemployment rate also moved three ticks higher to 6.8%, completely unwinding the sharp drop in November, as the labour force grew at its fastest pace in over a year.

For all the headwinds and headaches, the labour market has put in a not-too-bad showing this year. In fact, the current unemployment rate is only 0.1 percentage points (ppts) above year-ago levels, a much better outcome than forecast in early 2025. Looking ahead, we’re expecting the jobless rate to peak this quarter before drifting lower thereafter as new labour force growth stalls. This report won’t change the Bank of Canada’s (BoC) policy stance, with several important data points due out before their January 28th meeting.

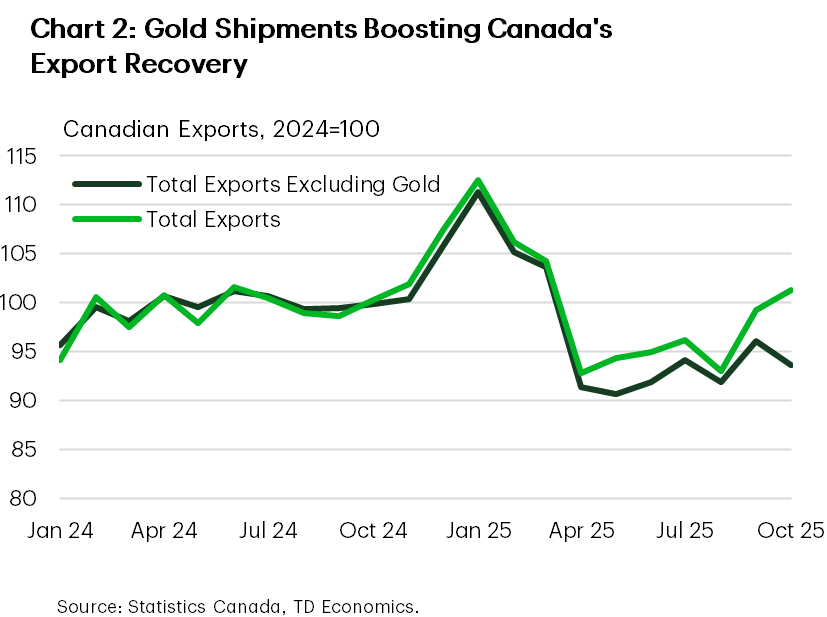

The improvement theme was also seen in the October trade data even though the nation’s trade balance flipped back to into the red. Chart 2 shows that total exports (including gold) have increased by 9% since bottoming in April 2025 and are approximately in line with average export levels for 2024, though those numbers have been lifted by high gold prices. Strip gold out of the equation and exports are up a more modest 2.5% since April 2025 and remain 6% below the 2024 average. Gold now accounts for almost 14% of Canada’s nominal exports, over three times above than its historical average.

There is also some improvement in export diversification. One third of Canadian exports are now being shipped to non-U.S. markets, a level never achieved outside of trade distortions seen during the early days of the pandemic. But again, gold is a big part of the picture. A multi-month surge in unwrought gold exports to the UK has made a sizeable contribution to the rise. Also of note, China has quickly become the main overseas buyer of Canadian crude, which has also helped Canada orient toward East-West trade.

Cultivating this relationship will be important, especially in the wake of the recent U.S./Venezuela situation. We wrote here about the potential near-term risks to Canada’s oil industry, and while minimal, it still strengthens the case for Canada to expedite a new oil pipeline that builds out capacity for Asian shipments. Chinese demand for Canadian crude is set to increase as the U.S. pressures Venezuela to cut ties with China. Canadian oil also has shorter shipping times and flexible tanker options, buoying the case for China to buy more Canadian crude. We are likely to see this discussed next week when Prime Minister Mark Carney visits China to engage in talks around boosting trade and investment.

U.S. – Hiring Slows, Affordability Worries Grow

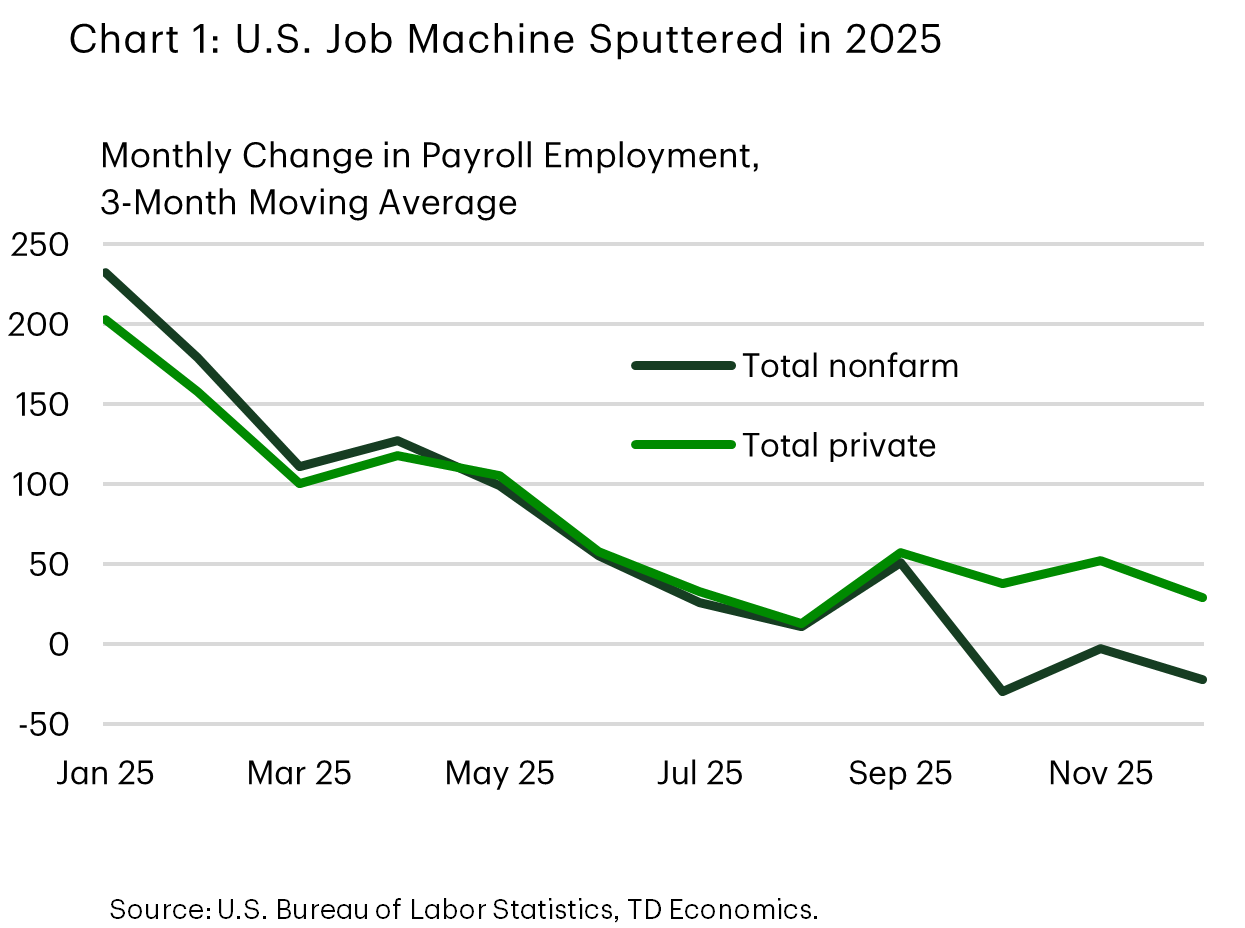

The world was on tenterhooks this morning as all waited to see if the Supreme Court would rule on the administration’s use of the International Emergency Economic Powers Act (IEEPA) to implement some of its tariffs in 2025. The much-anticipated IEEPA ruling did not come, so the big news of the day is the weaker than expected December jobs report. Private sector hiring slowed, prior months were revised lower, and the number of jobseekers declined, allowing the unemployment rate to fall even as jobs growth slowed. The data reinforce the view that 2025 was a “low hire, low fire” year, characterized by a pronounced deceleration in job growth and a modest rise in the unemployment rate (Chart 1).

Survey data this week were mixed. The ISM Manufacturing Index contracted for a tenth consecutive month, with respondents citing “tariff related pricing pressures” and notable reductions in 2026 capital expenditure plans. By contrast, the ISM Services surprised to the upside, highlighting continued resilience in consumer demand for travel, healthcare, and professional services. The divergence between manufacturing and services has persisted throughout the year, as manufacturing remains more exposed to tariff related uncertainty. Both surveys indicated easing price pressures and softening labour demand, consistent with today’s payrolls release.

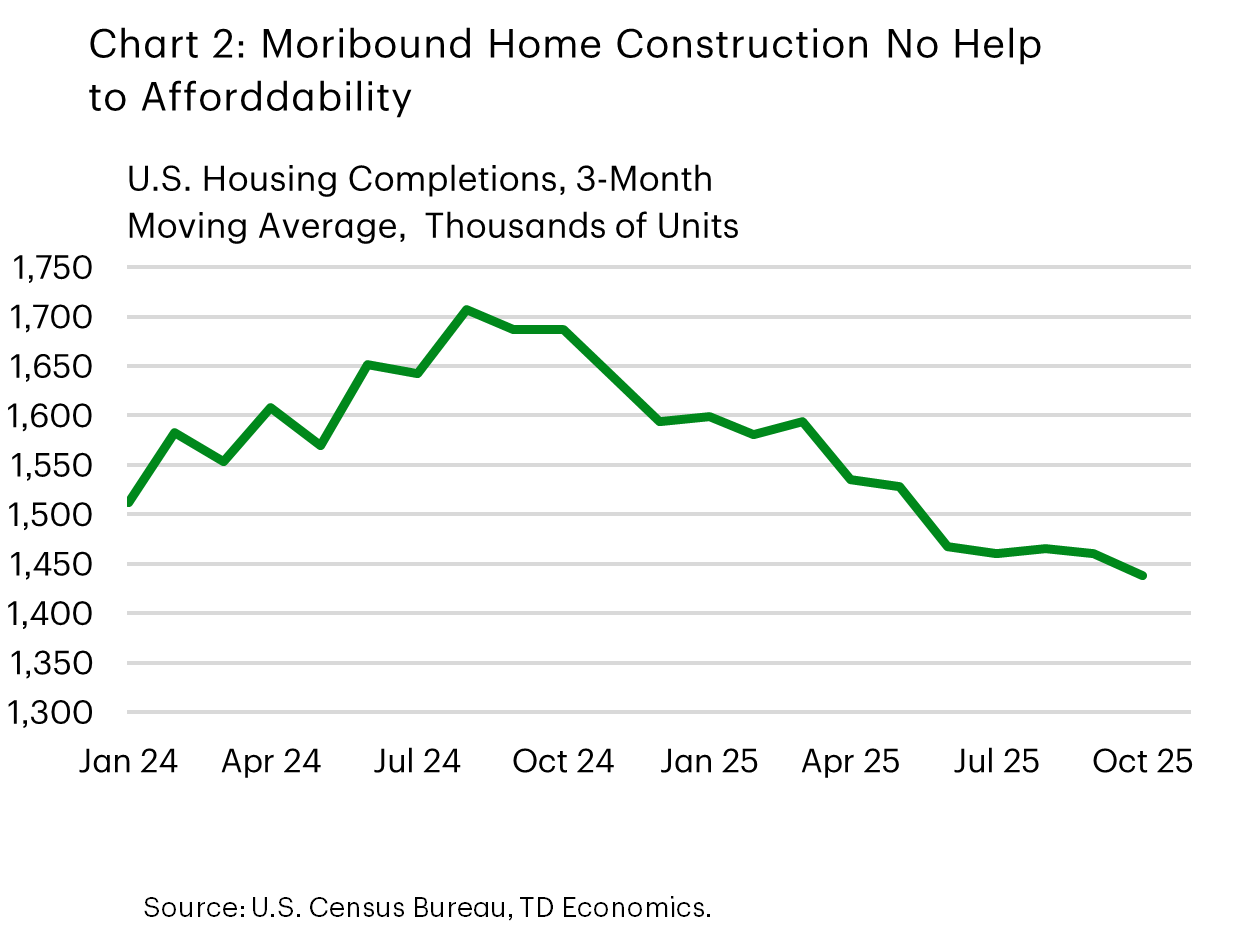

Developments in Venezuela added complexity to the oil market backdrop. Markets are assessing the administration’s commitment to the “Donroe Doctrine” and its implications for global oil supply. Despite Washington’s efforts to restore Venezuelan output, significant logistical and political hurdles remain. WTI moved down toward US$57 following the announcement that up to 50 million barrels of seized Venezuelan crude will be released to help address household affordability concerns. Adding to the affordability theme, housing data showed that homebuilding remains subdued, which doesn’t help the cost of housing (Chart 2). The administration has a clear desire to act on this front, promising a ban on institutional investor purchases and demanding government purchase mortgage-backed securities to help lower mortgage rates, though we await details on actual policy actions.

Prior to Friday’s jobs numbers, Federal Reserve officials suggested risks around employment and inflation were broadly balanced. Minneapolis President Kashkari indicated the labour market may be approaching equilibrium, while Richmond President Barkin characterized the economy as “finely tuned,” implying the FOMC would need to give equal weight to prices and employment. This reinforces our view and the view of the market that the FOMC is not in a hurry to cut rates further now, though we do expect to see interest rates come down later this year. We look ahead next week to the release of CPI inflation data, and after being let down by the Supreme Court this week, we are not going to be alone in being eager for news about when they may release decisions next.

. The unemployment rate also moved three ticks higher to 6.8%, completely unwinding the sharp drop in November, as the labour force grew at its fastest pace in over a year.){kind=link}