The first full week of 2026 delivered a barrage of geopolitical shocks that would normally be expected to rattle global markets. Instead, investors largely looked through the noise, producing a market outcome that appears counterintuitive at first glance.

The most dramatic development came from Latin America, where the US carried out a direct military intervention that resulted in the capture of Venezuela’s President. Washington subsequently moved to take control of Venezuela’s vast oil reserves, for selling previously sanctioned crude, marking a decisive escalation in US involvement in the region.

Shortly after, geopolitical tensions widened further as the White House doubled down on rhetoric around Greenland, describing its acquisition as a “national security priority” to counter Russian and Chinese influence in the Arctic. While the likelihood of outright annexation remains remote, the language alone was enough to keep geopolitical risk firmly in focus.

At the same time, Iran entered one of its most significant periods of domestic unrest in years, with nationwide protests met by a violent crackdown. The deterioration in internal stability added further to an already crowded geopolitical picture, particularly given Tehran’s strained relationship with Washington.

Despite this heavy backdrop, global risk appetite proved remarkably resilient. Major equity indices including S&P 500, FTSE and DAX all pushed to fresh record highs, sending a clear signal that markets were unwilling to price in systemic risk from geopolitical headlines alone.

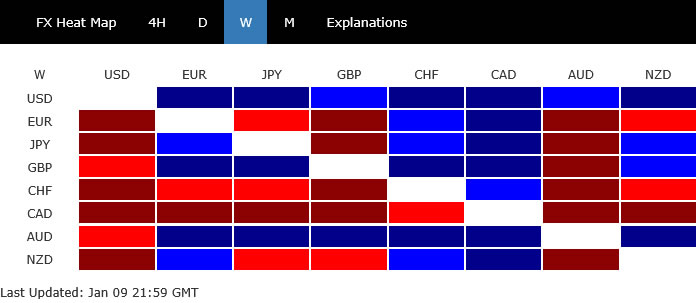

Instead, the adjustment occurred primarily in currencies. Dollar emerged as the strongest performer of the week, supported both by its hegemonic role during periods of global tension and by a shift in Fed expectations following a full slate of US data releases.

Aussie followed as the second-best performer, buoyed by firm risk appetite and reinforced by RBA rhetoric that ruled out near-term rate cuts. Sterling also benefited from the broader risk-on tone.

At the other end of the spectrum, Loonie stood out as the weakest major currency, followed by Swiss Franc and Euro. Kiwi and Yen finished the week mixed in the middle, highlighting that geopolitics did matter — but only selectively.

Dollar Leads But Lacks Intermarket Confirmation

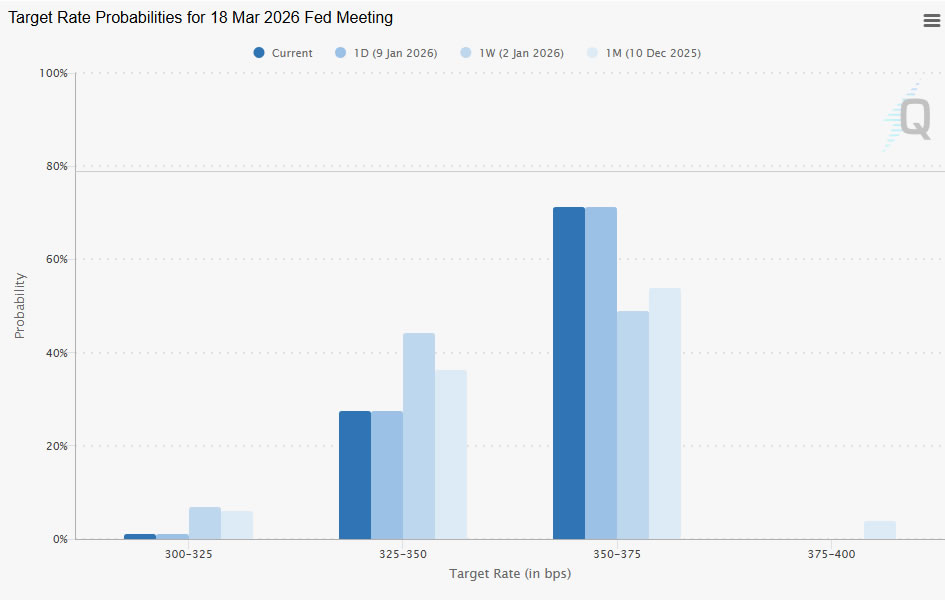

Dollar finished last week as the strongest major currency, extending gains after some hesitation. Following a string of mixed but generally resilient US economic releases, markets have moved swiftly to price out the chance of near-term easing. Fed funds futures now imply over a 70% probability that rates will be held at 3.50–3.75% at the March FOMC meeting, a sharp reversal from less than 50% just a week earlier.

A key anchor for that repricing was the labor market. While December payroll growth was modest at 50k, the unemployment rate fell from a revised 4.5% in November to 4.4%, reinforcing the view that labor conditions remain tight despite slowing hiring momentum. That combination leaves the Fed with little incentive to rush into another “insurance cut.” With wage growth still firm and unemployment low, policymakers can afford to wait for clearer signs of deterioration before shifting stance.

Technically, Dollar Index’s rebound extended with firm break of 55 D EMA (now at 98.75). That move suggests the pullback from 100.39 has completed at 97.74 as a correction. Further rally is now in favor back to 100.39 resistance, and possibly above.

Even so, the broader structure remains corrective. The advance from 96.21 is still viewed as a counter-trend move within the longer-term decline from 110.17. As such, upside potential is expected to be capped near 38.2% retracement of 110.17 to 96.21 at 101.54, absent substantial shift in underlying developments.

For Dollar to transition from a corrective rebound to sustained medium-term strength, intermarket confirmation is required. Specifically, markets would need to see a meaningful correction in equities and a decisive upside break in Treasury yields — ideally occurring in tandem. But that confirmation has yet to materialize.

DOW extended its uptrend to fresh record highs last week, suggesting that risk appetite remained intact. As long as 47,853 support holds, near-term bias remains bullish, with attention on 50,000 psychological level, which coincide with medium term rising channel ceiling. Decisive break above that 50,000 zone would likely accelerate gains towards 100% projection of 41,981.14 to 48,431.57 from 45,728.93 at 52,179.36. Such development would cap momentum of any Dollar rally.

Treasury yields is also a critical missing link in determining whether Dollar’s rebound can evolve into something more durable. For now, US 10-year yield is locked in a narrowing range, repeatedly finding support at the 55 D EMA (now at 4.136), while failing to generate enough momentum to clear the 4.200 cluster resistance (38.2% retracement of 4.629 to 3.947 at 4.207) decisively.

On the one hand, decisive break above 4.200, would confirm that the fall from 4.629 has completed already. That would open the way to 61.8% at 4.63. However, sustained break of the 55 D EMA will argue that recent rebound from 3.947 has completed, and bring deeper fall back to 4.000 round number. If realized, that could also mark the completion of Dollar Index’s corrective bound, and drag it lower back towards 96.21 support.

Venezuela Shock Exposes CAD’s Strategic Vulnerability

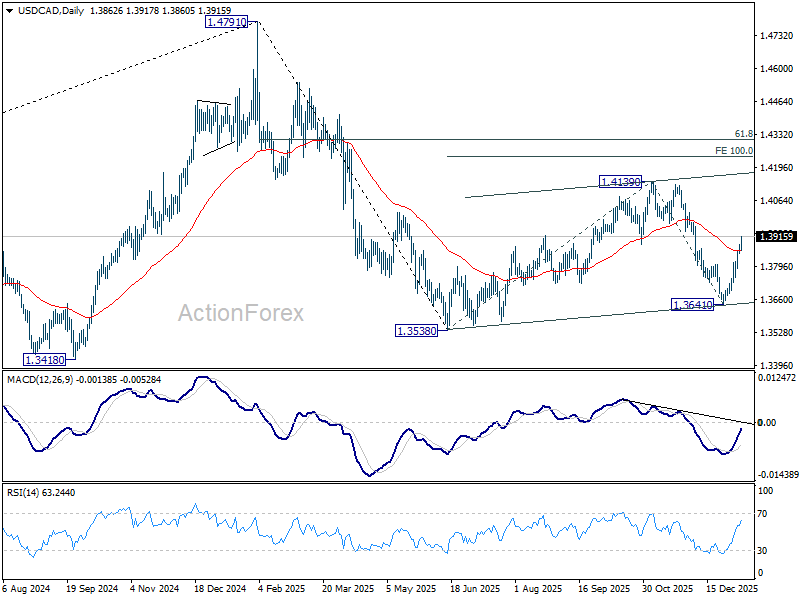

Among the major currencies, Canadian Dollar emerged as the clear underperformer of the week. Its weakness stood out not only against US Dollar, but also relative to other commodity-linked peers, highlighting that this was not a generic risk move but a distinctly Canada-specific repricing.

At the heart of the selloff was the US military intervention in Venezuela and the subsequent decision by Washington to take control of the country’s oil output. President Donald Trump announced that Venezuela’s interim authorities would transfer an estimated 30–50 million barrels of sanctioned crude to the US, with shipments expected to arrive directly at US unloading facilities.

In the near term, the mechanics and timing of these deliveries remain unclear. But markets wasted little time in pricing the implications. Any influx of Venezuelan crude into the US market would compete directly with Canadian oil exports.

Beyond the immediate supply impact, the longer-term strategic consequences weighed even more heavily on Loonie. Increased Venezuelan oil flows weaken Canada’s leverage ahead of this year’s review of the CUSMA trade agreement, which has so far shielded much of Canada’s exports from US tariffs.

Even though most Canadian crude enters the US through the Midwest rather than the Gulf Coast, markets are forward-looking. The prospect of Washington having alternative oil supply options reduces Ottawa’s negotiating power at a sensitive political juncture.

Technically, price action in USD/CAD mirrors that fundamental shift. Last week’s strong rally suggests decline from 1.4139 has completed as a correction at 1.3641. The advance from there is now seen as the third leg of a broader corrective pattern originating from 1.3538. That opens the scope for a retest of 1.4139, and possibly further to 100% projection of 1.3538 to 1.4139 from 1.3641 at 1.4242.

Whether this move evolves into a full bullish reversal could ultimately hinge on the outcome of the CUSMA review and how aggressively Washington reshapes continental energy flows.

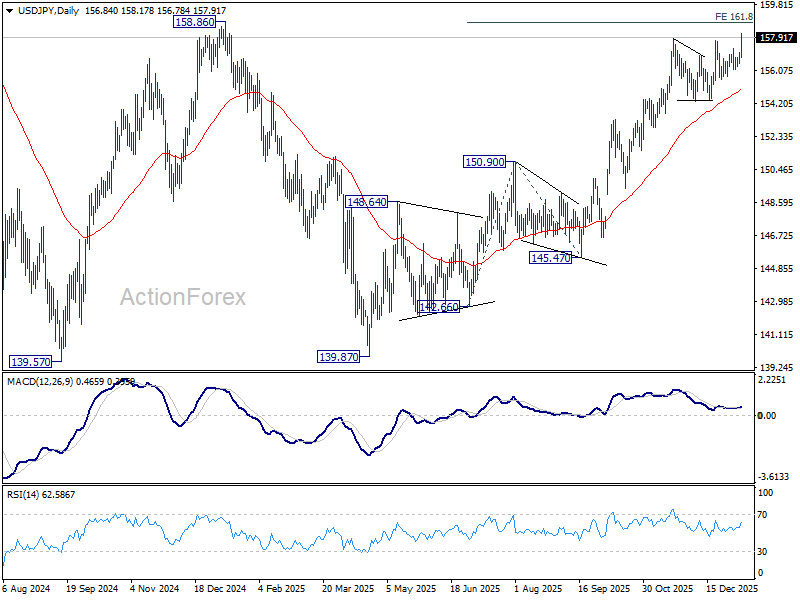

Snap Election Speculation Lifts Nikkei, Undermines Yen

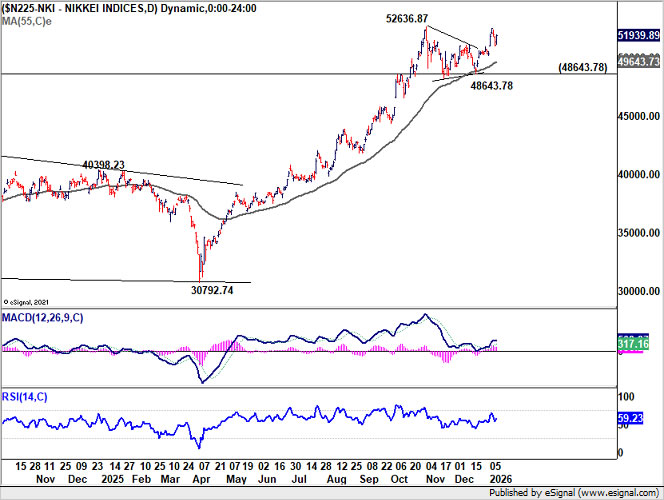

Yen failed to play its traditional safe-haven role last week. Instead, USD/JPY staged a clear upside breakout during, supported partly by firmer US data and Fed repricing. But more importantly, the selloff in Yen was fueled by a sharp shift in sentiment toward Japanese assets. The catalyst came from local political reporting rather than macro data.

According to the Yomiuri Shimbun’s late report on Friday, Prime Minister Sanae Takaichi is weighing a snap election as early as February. The strategy would allow her to leverage high approval ratings to secure a more stable governing majority.

For markets, the election narrative is significant because it strengthens expectations of fiscal expansion. A renewed mandate would give Takaichi greater freedom to pursue growth-supportive spending policies, reinforcing Japan’s equity story.

That prospect drove Nikkei futures sharply higher to new records after the local market close. The rally, in turn, accelerated outflows from Yen, which once again behaved as a funding currency rather than a haven.

Technically, immediate attention now turns to whether Nikkei 225 can gap cleanly above 52,636.87 on Monday and sustain momentum. If it does, the next focus will be 138.2% projection of 25,661.89 to 42,426.77 from 30,792.74 at 53,961.80. Firm break there will pave the way to 161.8% projection at 57,918.32.

If Nikkei does push toward 58k region, USD/JPY is likely to follow toward the 161.94 high. The key risk then becomes policy response: whether Japanese authorities intensify verbal warnings, or ultimately move toward direct intervention should the pair break above 158.86 structural resistance zone.

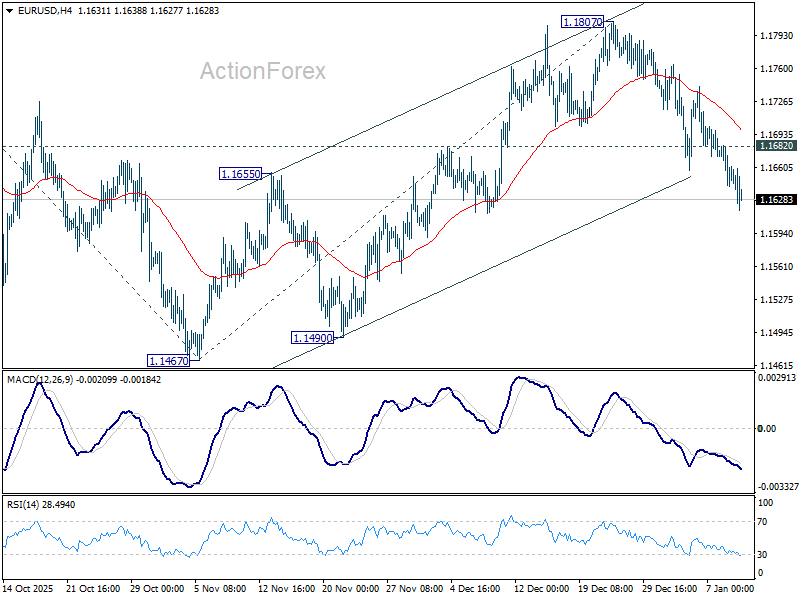

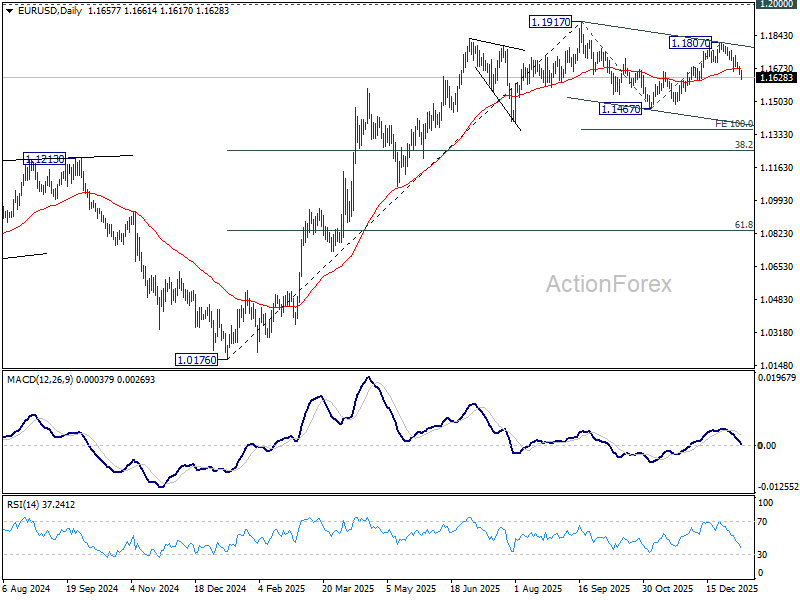

EUR/USD Weekly Outlook

EUR/USD’s extended fall last week suggests that rise from 1.1467 has completed at 1.1807 already. Fall from there is seen as the third leg of the corrective pattern from 1.1917. Initial bias stays on the downside this week for retesting 1.1467. Break there will pave the way to 100% projection of 1.1917 to 1.1467 from 1.1807 at 1.1357. ON the upside, above 1.1682 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 1.1807 resistance holds, in case of recovery.

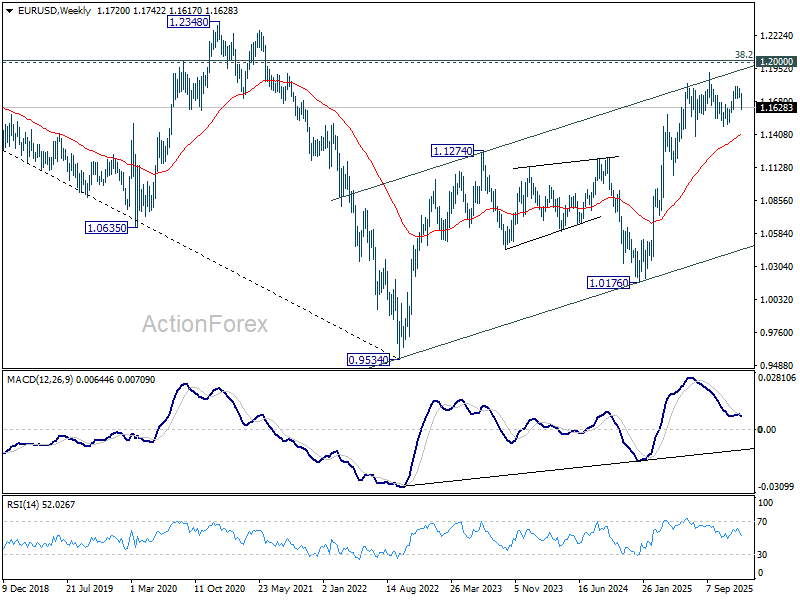

In the bigger picture, as long as 55 W EMA (now at 1.1406) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will carry larger bullish implication. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

In the long term picture, 38.2% retracement of 1.6039 to 0.9534 at 1.2019, which is close to 1.2000 psychological level is the key for the outlook. Rejection by this level will keep the multi decade down trend from 1.6039 (2008 high) intact, and keep outlook neutral at best. However, decisive break of 1.2000/19, will suggest long term bullish trend reversal, and target 61.8% retracement at 1.3554.

{kind=link}