Risk-on sentiment returned to global equity markets today as tensions surrounding Greenland appeared to de-escalate further. Stocks across regions pushed higher, reflecting relief that the immediate geopolitical shock has been contained, at least for now. The shift followed fresh comments from US President Donald Trump, who elaborated on the previously announced Greenland framework while attending the World Economic Forum. Trump said the US had secured “total and permanent access” to Greenland through a deal with NATO, stressing there would be no time limit on that access.

“It’s total access. There’s no end, there’s no time limit,” Trump told Fox Business, adding that negotiations were now focused on details rather than principle. The comments reinforced the perception that Washington has stepped back from confrontation of more tariff threats in favor of a security-based arrangement.

NATO Secretary General Mark Rutte confirmed that the alliance is now working through the operational aspects. Speaking to Reuters in Davos, Rutte said NATO commanders would handle the additional Arctic security requirements and expressed hope that implementation could be achieved event in early 2026.

Despite the improved tone, uncertainty remains. Denmark reiterated that its sovereignty over Greenland is not up for discussion, underlining that the framework does not amount to a transfer of ownership. Key details of the agreement remain unclear, keeping diplomatic nerves exposed beneath the surface calm.

More broadly, the episode has left scars in Europe. EU leaders are believed to be reassessing relations with the US, after the Greenland dispute shook confidence in the reliability of the transatlantic partnership. Concerns persist that U.S. policy could shift again abruptly.

That lingering distrust is visible in markets. While equities are rallying, Swiss Franc resilience suggests risk aversion has not fully disappeared. This is also reflect in Gold, which retreats from record highs without deeper pullback. Investors appear relieved, but not convinced that the issue is conclusively resolved.

In FX performance terms for the week so far, Dollar remains the second worst performer, ahead of only Yen, with Sterling also lagging. Kiwi leads, followed by Aussie, supported by strong Australian jobs data. Euro and Loonie trade mid-pack.

In Europe, at the time of writing, FTSE is up 0.52%. DAX is up 1.12%. CAC is up 1.18%. UK 10-year yield is up 0.033 at 4.496. Germany 10-year yield is down -0.003 at 2.881. Earlier in Asia, Nikkei rose 1.73%. Hong Kong HSI rose 0.17%. China Shanghai SSE rose 0.14%. Singapore Strait Time rose 0.38%. Japan 10-year JGB yield fell -0.047 to 2.241.

US initial jobless claims tick up to 200k vs exp 209k

US initial jobless claims fell -1k to 200k in the week ending January 17, below expectation of 209k. Four-week moving average of initial claims fell -4k to 201.5k, lowest since January 13, 2024.

Continuing claims fell -26k to 1849k in the week ending January 10. Four-week moving average of continuing claims fell -16k to 1871k.

ECB accounts signal patience, reject directional bias

The December meeting accounts showed the ECB broadly aligned with prevailing market rate expectations of not rate move in the near term. Nevertheless, the accounts emphasized that patience should not be misread as inertia.

While the Governing Council felt policy was “in a good place,” members stressed that this did not imply a static stance. The ECB retains flexibility to respond as conditions evolve, indicating that patience does not equate to reluctance to act or a one-sided reaction function.

Uncertainty featured prominently in the discussion. Novel risks—including the AI-driven investment boom, potential U.S. tariffs, and concerns over Chinese dumping—cloud the outlook. While some members saw risks skewed toward inflation undershooting the target, a smaller group warned of overshoot risks.

Against that backdrop, “it was important not to give the impression that the next move would be in one direction or the other, or to suggest any tightening or easing bias,” the minutes noted.

Australia jobs surge 65.2k in December, unemployment drops to 4.1%

Australia’s labor market delivered a major upside surprise in December, reinforcing the picture of persistent tightness. Employment surged 65.2k, more than double expectations of 26.5k, driven primarily by a strong rise in full-time jobs (+54.8k), with part-time employment also increasing (+10.4k).

The strength fed directly into the unemployment rate, which fell from 4.3% to 4.1%, far below expectations of 4.4% and matching the joint-lowest level since December 2024. The participation rate held steady at 66.8%, while monthly hours worked rose 0.4% mom, signaling that labor demand remains robust rather than superficial.

According to Sean Crick, head of labour statistics at Australian Bureau of Statistics, the drop in unemployment was partly driven by more younger people entering the workforce. Even so, the scale of job creation highlights an economy that continues to absorb new entrants with ease.

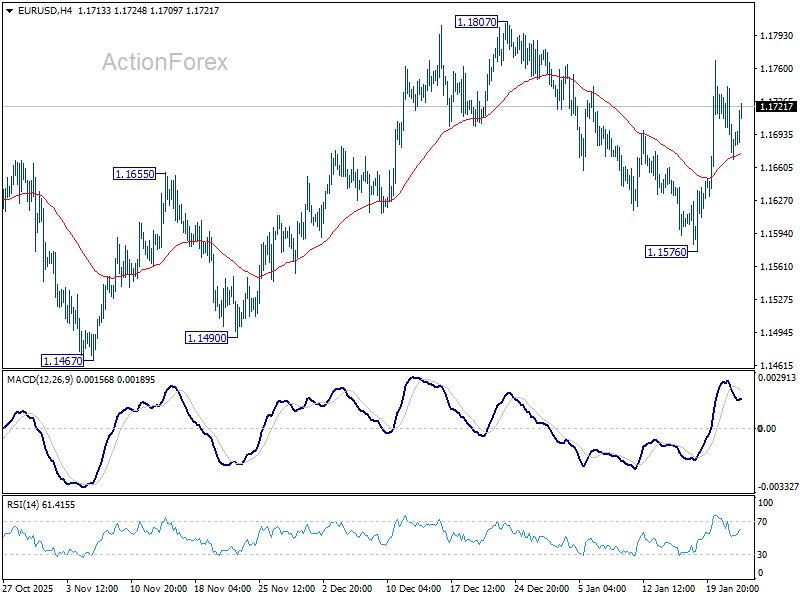

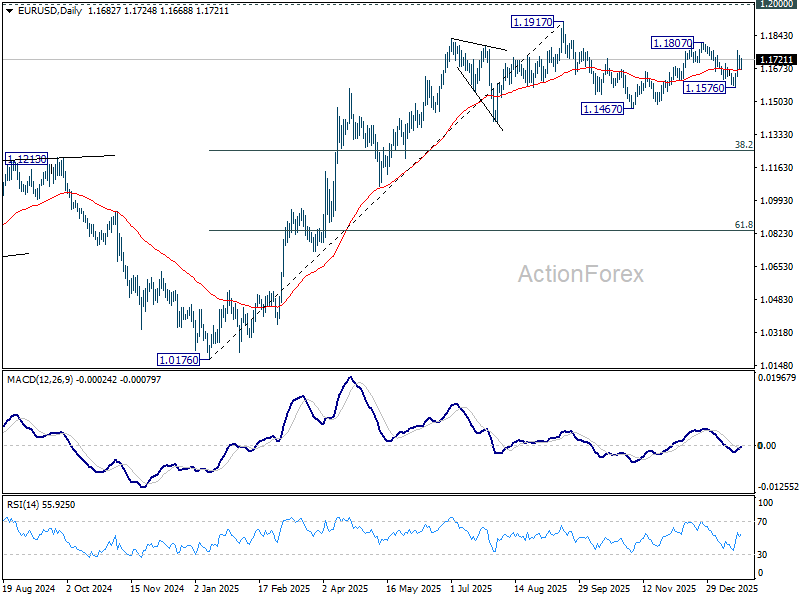

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1660; (P) 1.1701; (R1) 1.1727; More….

Intraday bias in EUR/USD remains neutral and risk stays on the upside with 55 4H EMA (now at 1.1672) intact. Break of 1.1807 will resume whole rally from 1.1467, and target a retest on 1.1917 key resistance level. However, sustained trading below 55 4H EMA will bring deeper fall back to 1.1576 support instead.

In the bigger picture, as long as 55 W EMA (now at 1.1413) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will carry larger bullish implication. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

{kind=link}