Forex markets remained relatively steady following the January US CPI release, with the slightly softer-than-expected headline reading failing to trigger major repositioning. The moderation in inflation was largely driven by lower energy prices, while underlying pressures showed only gradual improvement. The data did little to materially alter Fed expectations.

A March hold is effectively locked in, with markets pricing around an 88% probability of no change. Attention instead remains on June, where odds of a rate cut stand near 70%, reflecting expectations that gradual disinflation will eventually allow the Fed to ease.

With policy expectations stable, focus now shifts back to broader risk sentiment. US equity futures were flat at the time of writing, leaving open the question of whether yesterday’s AI-driven selloff will extend into the final session of the week.

On the trade front, according to the Financial Times, US President Donald Trump is considering scaling back some tariffs on steel and aluminum products. Officials reportedly believe certain levies have raised consumer costs on items such as cans and tins. The administration is said to be reviewing affected products and may exempt select items while halting further expansion of tariff lists.

Treasury Secretary Scott Bessent told CNBC that any adjustments would likely involve clarification on “incidental objects,” though ultimate authority rests with the president. Markets will watch closely for confirmation, as even limited tariff easing could modestly support sentiment.

For the week so far, Dollar is the weakest performer, followed by Sterling and Kiwi. Yen leads gains, with Swiss Franc and Aussie also firm. Euro and Loonie sit mid-pack. Positioning remains fluid, and a renewed shift in risk appetite could still reshape currency rankings before weekend.

In Europe, at the time of writing, FTSE is flat. DAX is up 0.22%. CAC is down -0.32%. UK 10-year yield is down -0.017 at 4.438. Germany 10-year yield is down -0.014 at 2.769. Earlier in Asia, Nikkei fell -1.21%. Hong Kong HSI fell -1.72%. China Shanghai SSE fell -1.26%. Singapore Strait Times fell -1.57%. Japan 10-year JGB yield fell -0.022 to 2.213.

US CPI Cools to 2.4% as energy drag offsets shelter gains

US headline CPI eased from 2.7% yoy to 2.4% in January, slightly below expectations of 2.5% and marking the lowest reading since May.

Core CPI also moderated, slipping from 2.6% to 2.5%, matching forecasts and reaching its lowest level since early 2021. Over the past 12 months, the energy index fell -0.1%, while food prices rose 2.9%.

On a monthly basis, CPI rose 0.2%, while core CPI increased 0.3%. Shelter remained the largest contributor to the monthly gain, rising 0.2%, alongside a 0.2% increase in food prices. These advances were partially offset by a -1.5% decline in energy prices, which helped cap overall inflation momentum.

The data reinforce the view that inflation pressures are gradually easing, though core components — particularly shelter — continue to keep underlying price growth above the Fed’s 2% target.

BoE’s Pill warns disinflation incomplete despite projected CPI drop

BoE Chief Economist Huw Pill said UK underlying inflation remains around 2.5%. He emphasized that policy must continue to bear down on price pressures to ensure disinflation is sustained.

While headline inflation is projected to fall toward 2% in April or May, Pill noted that much of the expected decline reflects temporary effects from measures announced in Chancellor Rachel Reeves’ November budget. Stripping out that half-percentage-point impact, underlying price pressures remain firmer than the 2% target.

“In order to complete that (disinflation) process, monetary policy has a part of play and that means we do need to retain some restrictiveness in the stance of monetary policy until that process of disinflation is complete,” Pill said.

Pill said monetary policy still carries a degree of restrictiveness, even if its exact magnitude has become “more ambiguous now”. “Perhaps there’s more ambiguity about the extent of restriction than there is ambiguity about the incompleteness of the disinflation process to target,” he added.

Swiss CPI flat as imported prices drag

Switzerland’s consumer prices slipped -0.1% mom in January, undershooting expectations for a flat reading. The decline was largely driven by a -0.6% drop in imported product prices, while domestic prices edged up 0.1% on the month. Core CPI, which excludes fresh and seasonal products, energy and fuel, rose 0.1%, suggesting limited underlying pressure.

On an annual basis, headline inflation held steady at 0.1% yoy, in line with expectations. Core inflation was unchanged at 0.5%, with domestic product prices also steady at 0.5% from a year earlier. The data point to a subdued price environment, with limited momentum building in domestic costs.

Imported prices remained a key drag, falling -1.5% year-on-year compared with a -1.6% decline previously. The stronger Swiss Franc and softer external price dynamics continue to suppress imported inflation, keeping overall price growth well below levels seen elsewhere in Europe.

BoJ’s Tamura says inflation becoming “sticky,” sees scope to tighten

BoJ board member Naoki Tamura said in a speech that the wage–price cycle the Bank has been aiming to establish remains intact, with inflation increasingly driven by domestic factors rather than imported cost shocks. He argued that inflation is “becoming endogenous and sticky,” as higher labor costs replace raw material prices as the primary driver.

Tamura noted, as early as this spring the Bank could judge its price stability target achieved — provided wage growth in 2026 is confirmed to be consistent with the 2% goal for a third consecutive year. Such confirmation would mark a significant milestone in Japan’s long struggle to exit deflation.

He cautioned, however, that price developments warrant close attention as Yen resumes depreciation. Also, as firms continue to lift wages, there is strong potential for higher labor costs to be passed through across production, distribution and retail stages.

Tamura also there remains “considerable distance” to the neutral interest rate level, implying that even further rate hikes would leave financial conditions accommodative. The challenge, he said, is to avoid both a premature tightening that risks deflation and an environment of persistent inflation that exceeds what can be considered moderate — a balancing act that keeps normalization gradual.

NZ BNZ manufacturing eases to 55.2, but signals continued expansion

New Zealand’s BusinessNZ Performance of Manufacturing Index eased from 56.1 to 55.2 in January, indicating a slight moderation in momentum but remaining firmly in expansion territory. Production slipped from 57.5 to 56.6, employment edged down from 53.7 to 52.9, and new orders cooled from 59.9 to 56.4, pointing to slower yet still solid activity.

Despite the pullback, BNZ described the latest reading as reflecting a “healthy level of expansion.” Senior Economist Doug Steel said the January PMI adds to evidence that the economy has “finally turned the corner,” aligning with forecasts and a broader set of indicators suggesting decent growth.

However, underlying sentiment showed some softening. The proportion of positive comments from respondents fell to 47.7% in January, down from 57.1% in December and 54.4% in November. While the sector remains in growth mode, the decline in optimism hints at a more cautious tone among manufacturers as 2026 begins.

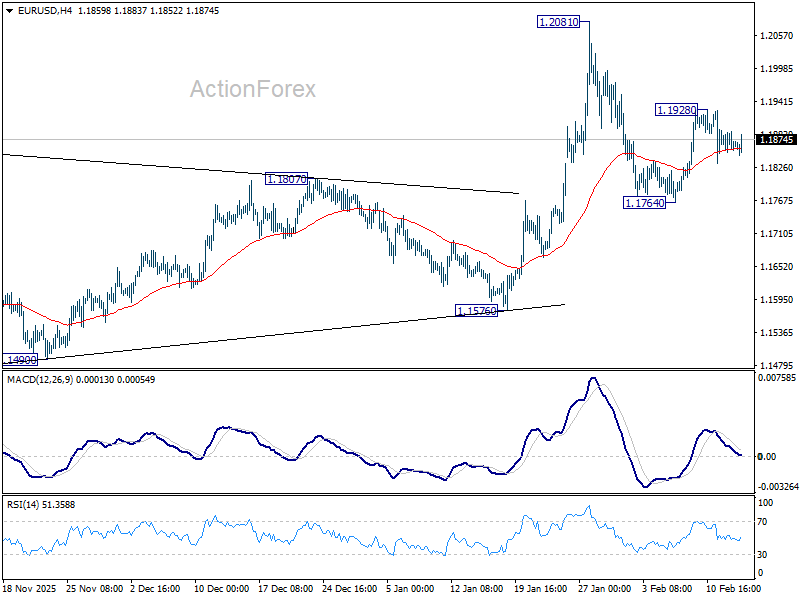

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1853; (P) 1.1871; (R1) 1.1891; More….

EUR/USD recovers mildly from 55 4H EMA but stays in established tight range. Intraday bias remains neutral. On the upside, above 1.1928 will target a retest on 1.2081 high. Decisive break there and sustained trading above 1.2 psychological level will carry larger bullish implications. On the downside, however, sustained trading below 55 D EMA (now at 1.1756) will raise the chance of reversal on rejection by 1.2, and target 1.1576 support for confirmation.

In the bigger picture, as long as 55 W EMA (now at 1.1470) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will add to the case of long term bullish trend reversal. Next medium term target will be 138.2% projection of 0.9534 to 1.1274 from 1.0176 at 1.2581. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

{kind=link}