- As widely expected, the RBNZ held the OCR at 2.25%. The decision was unanimous, so no vote was required.

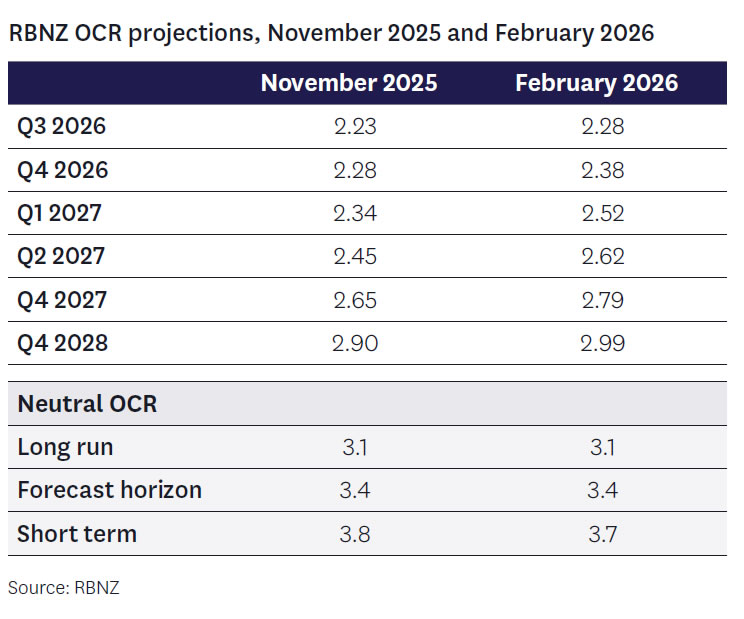

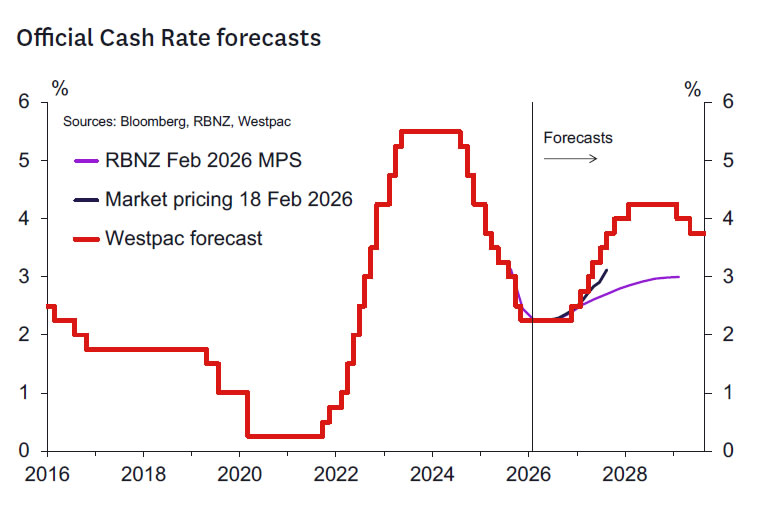

- The RBNZ’s revised OCR forecast signals the likelihood of policy tightening beginning late this year, rather than by mid-2027 as was forecast in November.

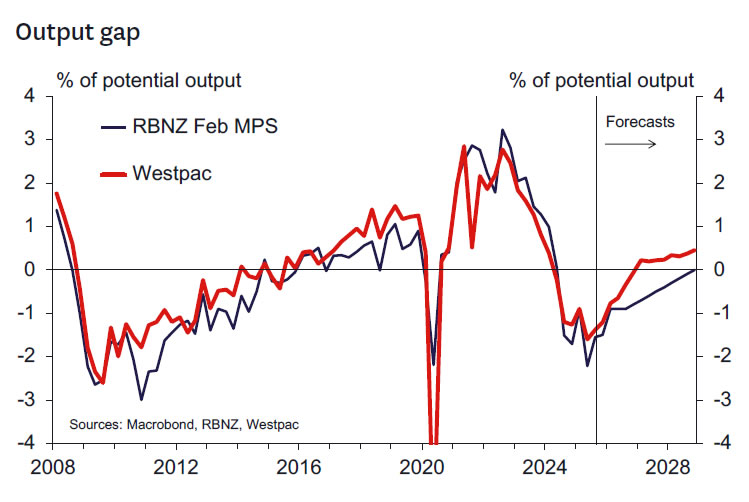

- The RBNZ’s activity outlook hasn’t been significantly lifted and is weaker in the second half of 2026 and into 2027.

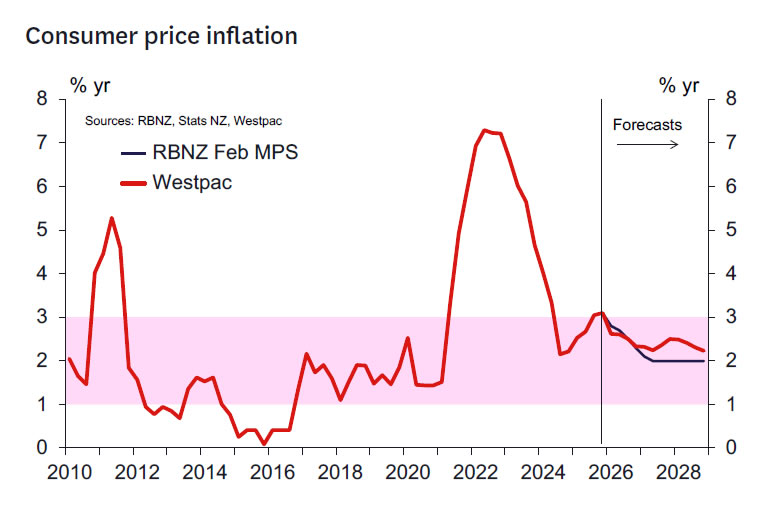

- The RBNZ expects inflation to move back inside the target band in the coming quarter and fall back to 2.0% by mid-2027. Risks are viewed as “balanced”.

- Westpac continues to expect the OCR will begin rising from the December 2026 meeting, with tightening to continue at most meetings in 2027.

- The generally dovish tone significantly moves the balance of risk away from an earlier start to the tightening cycle.

- Policy could tighten sooner than December if either activity or inflation readings exceed the RBNZ’s expectations, or later if the converse occurs.

Key take out: OCR on hold for a while yet.

As widely expected, the RBNZ held the OCR at 2.25%. The decision was reached by consensus and so no vote was required.

Also as expected, the RBNZ’s revised projections include a pulling forward of the timing of projected policy tightening.

The RBNZ’s forecast profile was a bit more dovish than we anticipated, and noticeably less hawkish than market pricing. Our view was that the RBNZ would bring forward the tightening to December but wouldn’t place much if any weight on an OCR increase before then. We expected that there would be a good chance of a follow-up hike in February 2027. As it happened, while the RBNZ removed the chance of an OCR cut in the first half of 2026 and signalled the possibility of an end of year hike, they didn’t see a follow up hike in the first quarter of 2027. A full hike seems evident by February 2027 vs the mid-2027 implied last time but it will take some time before the neutral 3-3.5% neutral zone is reached (2028/29 in these forecasts).

This modest shift forward in the tightening profile reflects a few key judgements:

- The output gap initially narrows a little bit more quickly than previously but then narrows more slowly such that the timeframe over which it closes completely remains unchanged (see detail below). The RBNZ didn’t assess the stronger Q3 GDP outcome as implying much in terms of reduced spare capacity and they have not upgraded their short-term growth forecasts. This is consistent with the RBNZ thinking their current GDP nowcasts are a fair reflection of how growth will evolve in the next couple of quarters. The RBNZ remains quite cautious around how quickly the economy will recover, emphasising the early stage of the recovery and the significant uncertainties to come. They also played up the rise in the unemployment rate recorded in the December 2025 quarter data.

- House prices are expected to be flat over 2026 and up 3% over 2027 and are seen to be a restraint on household demand.

- Inflation is forecast to remain above 2% over the year ahead, but the RBNZ remains comfortable that the fall in the headline rate expected will bring inflation close to 2%. These forecasts give the MPC time to assess the strength and durability of the economy.

- The RBNZ noted the tightening in financial conditions since November without drawing strong conclusions for the economic outlook. By implication, higher interest rates and the exchange rate likely are leaning against the economic recovery and inflation pressures, but it’s also the case that confidence around the economic outlook has improved a bit.

Commentary from the Governor and her colleagues at the press conference built on the overall dovish message from the forecasts. She noted the forecasts of inflation moving towards 2% in the year ahead, allowing room for the OCR to remain at 2.25% for much of 2026. The MPC sees the forecasts as consistent with a less than full chance of an OCR increase by year-end and there is consensus around that view. The RBNZ noted they were “confident of their position” and that this implied less tightening than market prices.

The Governor noted that there is an expectation that house prices will be flat over 2026 and won’t be as important in driving household consumption growth compared to an improving labour market. The Chief Economist noted that there could be some downside risks to the outlook for consumption growth associated with the house price forecasts.

Westpac’s OCR call.

We continue to expect that there will be no further policy easing this cycle and that the RBNZ will begin to raise the OCR from the December 2026 meeting. The timing of the return of the OCR to higher, more neutral levels will depend on the pace of the eventual recovery and the evolution of inflation.

The MPC seems to feel comfortable that they have time to assess, and the bar to justify OCR “lift-off” remains high. Hence risks of a 2027 start are perhaps a bit higher than we thought before but what’s clear is that risks of a pre-election hike seem low as of now. Much will depend on how economic activity and the labour market evolves over 2026.

Notable quotes.

Some notable quotes from the Statement of Record and MPS were as follows:

Current state of the economy

“ Economic activity began recovering over the second half of last year in response to strong export prices and supportive monetary policy settings.”

Growth outlook

“ There are signs that the recovery is broadening across the economy, although the September quarter GDP likely overstates the true level of momentum in the economy.”

Output gap / excess capacity

“ The Committee noted that there is still significant spare capacity in the economy. The output gap is estimated to be -1.5 percent of potential GDP in the December 2025 quarter.”

“ Spare capacity in the labour market is substantial but stabilising.”

Inflation outlook

“ The Committee is confident, however, that with significant excess capacity in the economy, inflation will fall to around the mid-point of the target range over the next 12 months.”

Inflation expectations

“ Inflation expectations for professional forecasters and business leaders increased slightly across all tenors, but long-term expectations remain close to the target mid-point.”

“ Inflation expectations of households have continued to decline from elevated levels.”

Current policy stance

“ Members agreed that the monetary policy stance would need to remain accommodative for some time to support a sustained recovery in economic activity.” Current financial conditions

“ Domestic financial conditions have tightened since November.”

Risks to the inflation outlook

“Risks to the outlook for inflation are balanced.” Global growth

“ The Committee noted that the global economy was more resilient than expected in 2025.”

“ The Committee continues to expect trade barriers to present a headwind to growth, with trading partner growth expected to weaken slightly over 2026.”

Outlook for monetary policy

“ If the economy evolves as expected, monetary policy is likely to remain accommodative for some time.”

“ Conditional on the central economic outlook, we project that the OCR will remain around its current level in the near term, before gradually increasing from late 2026.”

“ One member supported maintaining the OCR at current levels for now but noted that if economic activity recovers as expected, monetary stimulus could begin to be withdrawn somewhat earlier without compromising the economic recovery.”

Other notable quotes

“ The economic recovery has been uneven across sectors and regions.”

“ The Committee agreed that the economic recovery remains nascent, and a premature normalisation of monetary conditions could dampen the recovery and lead inflation to undershoot the target.”

RBNZ forecast detail.

The RBNZ’s forecasts for economic conditions are softer than our own.

The RBNZ has noted the lift in some economic indicators, supported by earlier monetary policy easing and firmness in commodity export earnings. However, they also noted that the recovery is still in its early stages, and spare capacity will take some time to dissipate.

What stands out is that, beyond the very near-term, the RBNZ expects that the recovery will remain fairly gradual, including continued softness in household spending growth. In part, that reflects the RBNZ’s expectations that unemployment will fall more gradually than we anticipate. We certainly appreciate the risk of the recovery remaining gradual in the near term. However, the pace of recovery in the RBNZ’s forecasts seems surprising given that their forecasts assume that monetary policy remains accommodative. It’s also surprising that despite that assumed accommodative policy stance, the RBNZ doesn’t expect the output gap to close until the end of 2028. In contrast, we expect firming economic activity will see unemployment fall faster and the output gap closing by late-2026/ early 2027.

It’s a similar story for inflation. While our forecasts and the RBNZ’s are very similar over the current year, the RBNZ’s longer-term inflation forecast looks low. Much of that is because they expect the strength in administered prices like government charges, which has boosted domestic inflation over the past few years, will dissipate. They also expect more modest price-setting behaviour by firms.

We think the risks on both of those fronts are firmly to the upside. While some specific administered prices might be more modest than in previous years, the strength seen in these costs has not been related to just a few categories. For several years we’ve experienced a rolling maul of large cost increases in a range areas that have pushed domestic inflation higher. And we expect that will continue to be the case over the coming years, limiting the downside for overall inflation. As a result, we continue to expect the medium-term inflation outlook will surprise the RBNZ to the upside, with longer term inflation remaining above 2%.

Key things to watch ahead of the RBNZ’s 8 April Review.

The next RBNZ policy review will take place on 8 April. The domestic data flow between now and then is relatively light. The most important economic releases are:

- The Q4 GDP report (19 March): The outcome of this report will be compared to the RBNZ’s estimate, with any deviation having implications for the RBNZ’s estimate of the output gap and perhaps also its view on near-term growth momentum. The RBNZ’s forecast of 0.5% growth is close to our own view (0.6%q/q).

- The February Selected Price Indexes (17 March): With the Q1 CPI report not released until 21 April, the RBNZ will have limited pricing data with which to assess whether inflation is tracking lower in line with its forecast.

- The January and February filled jobs reports (2 March and 30 March): With the next Household Labour Force Survey not due until 6 May, the Monthly Employment Indicator will provide insight as to whether job growth is likely to be sufficient to put the unemployment rate on a downward path.

In addition to the above, key monthly activity indicators such as the BusinessNZ manufacturing and services indexes and the ANZ Business Outlook survey will also be of interest (the next QSBO survey is not released until 21 April). Developments in retail spending and housingrelated indicators will also be monitored to see whether the economic recovery is broadening. The RBNZ will also monitor movements in key export commodity prices and financial conditions.

{kind=link}